100 Pesos – Mexico

Mexico

Context

Material

References

KM: #Click to copy to clipboard972

Numista: #55260

Value

Exchange value: 100 MXN = $5.82

Inflation-adjusted value: 170.38 MXN

Obverse

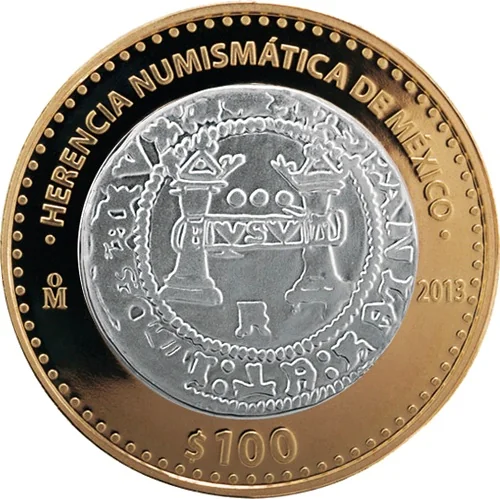

Reverse

Edge

Segmented reeding.

Categories

| Animal> Bird> Eagle |

| Currency> Coin depiction |

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Mexican Mint | (Mo) |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2013 | Mo | 8,000 | Prooflike |

Historical background

In 2013, Mexico's currency, the peso (MXN), operated within a context of relative stability and cautious optimism, but remained sensitive to both domestic policy shifts and global financial currents. The year was politically significant as it marked the beginning of Enrique Peña Nieto's presidency, following his inauguration in December 2012. His administration quickly launched an ambitious reform agenda, particularly in energy and telecommunications, which initially buoyed investor sentiment and supported the peso. The currency traded in a range of approximately 12 to 13 pesos per US dollar for much of the year, reflecting a period of calm compared to the volatility seen during the 2008-2009 global financial crisis.

The primary external influence on the peso in 2013 was the monetary policy speculation emanating from the United States Federal Reserve. Following the "taper tantrum" in mid-2013, when the Fed first hinted at reducing its quantitative easing program, emerging market currencies, including the Mexican peso, experienced bouts of pressure and depreciation. Investors, anticipating higher yields in the US, began pulling capital from emerging markets. However, Mexico was somewhat insulated from the worst of this volatility due to its strong macroeconomic fundamentals, including low public debt, a stable inflation rate, and a flexible credit line with the International Monetary Fund.

Domestically, the Bank of Mexico (Banxico) maintained a supportive stance, keeping its benchmark interest rate at a historic low of 4.0% for the entire year to foster economic growth. This policy, combined with the positive momentum from structural reforms, helped the economy and currency weather external shocks. Consequently, while the peso faced headwinds from global risk aversion, it ended 2013 without a dramatic crisis, positioned as one of the more resilient emerging market currencies, setting the stage for the challenges and adjustments that would come in subsequent years.

The primary external influence on the peso in 2013 was the monetary policy speculation emanating from the United States Federal Reserve. Following the "taper tantrum" in mid-2013, when the Fed first hinted at reducing its quantitative easing program, emerging market currencies, including the Mexican peso, experienced bouts of pressure and depreciation. Investors, anticipating higher yields in the US, began pulling capital from emerging markets. However, Mexico was somewhat insulated from the worst of this volatility due to its strong macroeconomic fundamentals, including low public debt, a stable inflation rate, and a flexible credit line with the International Monetary Fund.

Domestically, the Bank of Mexico (Banxico) maintained a supportive stance, keeping its benchmark interest rate at a historic low of 4.0% for the entire year to foster economic growth. This policy, combined with the positive momentum from structural reforms, helped the economy and currency weather external shocks. Consequently, while the peso faced headwinds from global risk aversion, it ended 2013 without a dramatic crisis, positioned as one of the more resilient emerging market currencies, setting the stage for the challenges and adjustments that would come in subsequent years.

💎 Very Rare