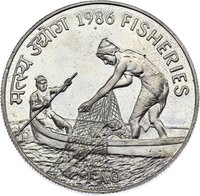

20 rupees – India

Add to wishlist

Non-circulating coins

Commemoration: Fisheries

India

Material

Diameter: 39 mm

Weight: 25 g

Shape: Round

Composition: Copper-nickel

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #53045

Value

Exchange value: 20 INR

Inflation-adjusted value: 313.21 INR

Obverse

Reverse

Edge

Reeded

Categories

| Animal> Fish |

| Organization> FAO |

Mints

| Name | Mark |

|---|---|

| Mumbai / Bombay | ♦ & B |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1986 | ♦ | — | ||

| 1986 | B | — | Proof |

Historical background

In 1986, India's currency situation was characterized by a tightly controlled and complex exchange rate regime under the License Raj. The Indian Rupee (INR) was not fully convertible and its value was pegged to a basket of currencies of India's major trading partners, though with a heavy de facto weight on the British Pound Sterling and the U.S. Dollar. The government, through the Reserve Bank of India (RBI), maintained a system of multiple exchange rates—a primary official rate for essential imports like oil and fertilizers, and a secondary rate for other transactions. This created a bureaucratic maze and fostered a black market for foreign exchange, as the official rate was often overvalued, making exports less competitive.

Economically, the year was part of a period of persistent external sector vulnerability. India's trade deficit was widening, foreign exchange reserves were chronically low (averaging around $5-6 billion, covering just a few weeks of imports), and the country relied heavily on external borrowing and aid, particularly from the International Monetary Fund (IMF). The 1980s saw increased borrowing to finance growth, leading to a growing debt burden. While the mid-80s saw some growth, the structural weaknesses—protectionist policies, inefficient industries, and the overvalued rupee—were storing up problems that would culminate in the 1991 balance of payments crisis.

Publicly, the currency was stable in nominal terms against the dollar, but this stability was artificial and maintained through severe restrictions. For the average citizen, access to foreign exchange for travel or study abroad was extremely limited and required arduous approvals. The system stifled economic efficiency, but the political will for radical liberalization was not yet present in 1986. The year thus represents a late phase of the pre-reform era, where the contradictions of a managed but overextended economy were becoming increasingly apparent, setting the stage for the dramatic reforms that would follow five years later.

Economically, the year was part of a period of persistent external sector vulnerability. India's trade deficit was widening, foreign exchange reserves were chronically low (averaging around $5-6 billion, covering just a few weeks of imports), and the country relied heavily on external borrowing and aid, particularly from the International Monetary Fund (IMF). The 1980s saw increased borrowing to finance growth, leading to a growing debt burden. While the mid-80s saw some growth, the structural weaknesses—protectionist policies, inefficient industries, and the overvalued rupee—were storing up problems that would culminate in the 1991 balance of payments crisis.

Publicly, the currency was stable in nominal terms against the dollar, but this stability was artificial and maintained through severe restrictions. For the average citizen, access to foreign exchange for travel or study abroad was extremely limited and required arduous approvals. The system stifled economic efficiency, but the political will for radical liberalization was not yet present in 1986. The year thus represents a late phase of the pre-reform era, where the contradictions of a managed but overextended economy were becoming increasingly apparent, setting the stage for the dramatic reforms that would follow five years later.

⭐ Rare