5000 rials (Fatima Ma'souma Dignity Decade) – Iran

Add to wishlist

Circulating commemorative coins

Commemoration: Fatima Ma'souma Birth Anniversary and Dignity Decade

Iran

Context

Material

Diameter: 29.3 mm

Weight: 10.1 g

Thickness: 2.1 mm

Shape: Round

Composition: Nickel brass

Magnetic: No

Technique: Milled

Alignment: Coin alignment

flip

References

KM: #

Numista: #52621

Value

Exchange value: 5000 IRR

Obverse

Description:

Iran, 5000 Rials, dated 1979.

Inscription:

جمهوری اسلامى ايران

۵۰۰۰

ريال

۱۳۹۲

۵۰۰۰

ريال

۱۳۹۲

Translation:

Islamic Republic of Iran

5000

Rials

1392

5000

Rials

1392

Language: Persian

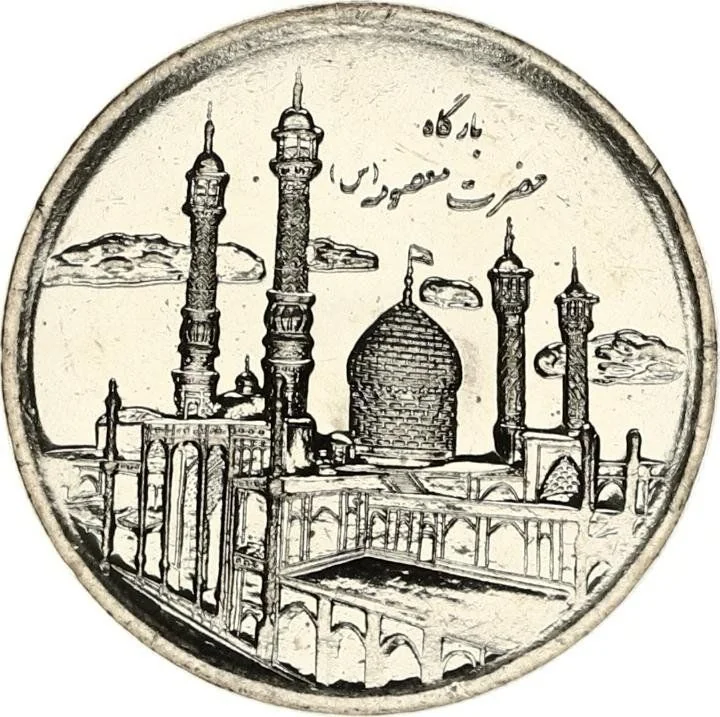

Reverse

Description:

Shrine of Hazrat Ma'souma (PBUH)

Inscription:

(بارگاه حضرت معصومه (س

Translation:

The Shrine of Hazrat Masoumeh (S.A.)

Language: Persian

Edge

Reeded

Categories

| Building> Religious building |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2013 | — | 20,000,000 | ||

| 2014 | — | — |

Historical background

In 2013, Iran's currency situation was defined by severe strain and volatility, primarily as a consequence of intensifying international sanctions. The core pressure came from sanctions targeting Iran's central bank and oil exports, enacted by the United States and the European Union in late 2011 and 2012. These measures drastically cut Iran's foreign currency earnings by hindering its ability to sell oil and access the global financial system, creating a critical shortage of hard currency like US dollars and euros needed for imports.

This shortage triggered a dramatic collapse in the value of the Iranian rial. The currency had lost over 50% of its value in 2012, and the instability continued into 2013. The government attempted to manage the crisis through a multi-tiered exchange rate system: an official rate for essential imports (around 12,260 rials to the dollar) and a vastly depreciated open market rate, which fluctuated wildly, at times exceeding 36,000 rials to the dollar. This gaping disparity fueled a rampant black market for foreign exchange, widespread corruption, and soaring inflation for ordinary citizens.

The economic distress was a central issue in the June 2013 presidential election, contributing to the victory of the moderate Hassan Rouhani, who campaigned on promises to stabilize the economy and resolve the nuclear standoff to secure sanctions relief. Therefore, by the end of 2013, the currency crisis was not just an economic issue but a pivotal political driver, setting the stage for the negotiations that would lead to the 2015 Joint Comprehensive Plan of Action (JCPOA).

This shortage triggered a dramatic collapse in the value of the Iranian rial. The currency had lost over 50% of its value in 2012, and the instability continued into 2013. The government attempted to manage the crisis through a multi-tiered exchange rate system: an official rate for essential imports (around 12,260 rials to the dollar) and a vastly depreciated open market rate, which fluctuated wildly, at times exceeding 36,000 rials to the dollar. This gaping disparity fueled a rampant black market for foreign exchange, widespread corruption, and soaring inflation for ordinary citizens.

The economic distress was a central issue in the June 2013 presidential election, contributing to the victory of the moderate Hassan Rouhani, who campaigned on promises to stabilize the economy and resolve the nuclear standoff to secure sanctions relief. Therefore, by the end of 2013, the currency crisis was not just an economic issue but a pivotal political driver, setting the stage for the negotiations that would lead to the 2015 Joint Comprehensive Plan of Action (JCPOA).

🌱 Common