1 Dollar – Trinidad and Tobago

Circulating commemorative coins

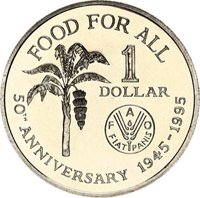

Commemoration: F.A.O. - Food for All

Trinidad and Tobago

Context

Year: 1979

Issuer: Trinidad and Tobago

Period:

(since 1976)

Currency:

(since 1964)

Total mintage: 1,000,000

Material

Diameter: 32 mm

Weight: 12.7 g

Thickness: 1.78 mm

Shape: Round

Composition: Copper-nickel

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #Click to copy to clipboard38

Numista: #5208

Value

Exchange value: 1 TTD

Obverse

Description:

Heraldic emblem

Inscription:

REPUBLIC OF TRINIDAD AND TOBAGO

TOGETHER WE ASPIRE TOGETHER WE ACHIEVE

1979

TOGETHER WE ASPIRE TOGETHER WE ACHIEVE

1979

Script: Latin

Reverse

Edge

Reeded

Categories

| Symbols> Coat of Arms |

| Organization> FAO |

Mints

| Name | Mark |

|---|---|

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1979 | — | 1,000,000 |

Historical background

In 1979, Trinidad and Tobago's currency situation was fundamentally shaped by the nation's oil boom, which had begun earlier in the decade following the 1973 oil crisis. The country was a significant petroleum exporter, and soaring global oil prices flooded the economy with foreign exchange (primarily US dollars). This led to a period of substantial government revenue, a strong balance of payments, and a seemingly stable Trinidad and Tobago dollar (TTD), which was pegged to the US dollar at a fixed rate of TT$2.40 = US$1.00. This peg, managed by the Central Bank established in 1964, provided predictability for trade and investment during this affluent period.

However, this stability was superficial and masked underlying vulnerabilities. The massive influx of petrodollars created intense inflationary pressures, as domestic production could not keep pace with the surge in government and consumer spending. This phenomenon, known as "Dutch Disease," began to undermine other sectors like agriculture and manufacturing, making the economy overly dependent on a single volatile commodity. Furthermore, the fixed exchange rate, while a symbol of strength, was becoming increasingly expensive to maintain as it required large reserves of foreign currency to defend, and it made non-oil exports less competitive on the global market.

Consequently, 1979 represented the peak before a sharp decline. The economy was overheating, and the rigid currency peg would soon be tested. The global oil market would begin to soften in the early 1980s, leading to a dramatic collapse in government revenue. The strains that were building in 1979—inflation, sectoral imbalance, and an overvalued fixed exchange rate—would culminate in a severe economic crisis by the mid-1980s, ultimately forcing the government to devalue the Trinidad and Tobago dollar and seek assistance from the International Monetary Fund. Thus, 1979 was the final chapter of the boom, with the currency regime poised for an inevitable and painful adjustment.

However, this stability was superficial and masked underlying vulnerabilities. The massive influx of petrodollars created intense inflationary pressures, as domestic production could not keep pace with the surge in government and consumer spending. This phenomenon, known as "Dutch Disease," began to undermine other sectors like agriculture and manufacturing, making the economy overly dependent on a single volatile commodity. Furthermore, the fixed exchange rate, while a symbol of strength, was becoming increasingly expensive to maintain as it required large reserves of foreign currency to defend, and it made non-oil exports less competitive on the global market.

Consequently, 1979 represented the peak before a sharp decline. The economy was overheating, and the rigid currency peg would soon be tested. The global oil market would begin to soften in the early 1980s, leading to a dramatic collapse in government revenue. The strains that were building in 1979—inflation, sectoral imbalance, and an overvalued fixed exchange rate—would culminate in a severe economic crisis by the mid-1980s, ultimately forcing the government to devalue the Trinidad and Tobago dollar and seek assistance from the International Monetary Fund. Thus, 1979 was the final chapter of the boom, with the currency regime poised for an inevitable and painful adjustment.

🌱 Common