20 Dollars – Canada

Canada

Context

Material

Diameter: 38 mm

Weight: 31.1 g

Silver weight: 28.77 g

Thickness: 3.5 mm

Shape: Round

Composition: 92.5% Silver

Standard: Silver ounce

Magnetic: No

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #Click to copy to clipboard272

Numista: #51906

Value

Exchange value: 20 CAD = $14.63

Bullion value: $82.33

Inflation-adjusted value: 37.77 CAD

Obverse

Description:

Queen Elizabeth II at 64, wearing the royal diadem and jewels, facing right.

Inscription:

ELIZABETH II D·G·REGINA

· 1995 ·

· 1995 ·

Translation:

Elizabeth II, by the Grace of God, Queen. 1995.

Script: Latin

Engraver: Dora de Pédery-Hunt

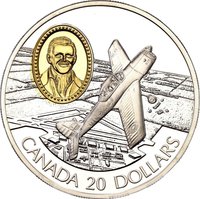

Reverse

Description:

DHC-1 Chipmunk, gold-plated cameo of Russell Bannock.

Inscription:

CANADA 20 DOLLARS

Script: Latin

Engravers: William Woodruff, Ago Aarand

Designer: Robert William Bradford

Edge

Interrupted reeding

Categories

| Transportation> Aircraft |

Mints

| Name | Mark |

|---|---|

| Royal Canadian Mint of Ottawa | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1995 | — | 17,722 | Proof |

Historical background

In 1995, Canada's currency situation was defined by a dramatic and sustained depreciation of the Canadian dollar, which reached a historic low. The dollar, often colloquially called the "loonie" following the introduction of the one-dollar coin in 1987, fell to an all-time closing low of 68.64 cents US in August of that year. This decline was part of a multi-year downtrend driven by several structural factors, including high levels of public debt, persistent federal and provincial budget deficits, and relatively high inflation and interest rates compared to the United States. Market confidence was further shaken by political uncertainty, notably the looming threat of Quebec sovereignty ahead of the October 1995 referendum.

The weak currency presented a complex economic picture. On one hand, it provided a significant boost to Canada's export-oriented sectors, such as manufacturing, forestry, and automotive industries, by making their goods cheaper on the international market. This export advantage was a crucial buffer for the economy. On the other hand, the low dollar contributed to higher costs for imported goods, putting upward pressure on consumer prices and squeezing purchasing power. It also symbolized a broader crisis of confidence in Canadian economic management, as international investors demanded a risk premium to hold Canadian assets.

The federal government's primary response was a decisive shift towards fiscal austerity. Finance Minister Paul Martin's 1995 budget, described as one of the most austere in Canadian history, implemented deep spending cuts to eliminate the federal deficit. This marked a pivotal turn away from the deficits of the previous decades and was aimed directly at restoring fiscal credibility and investor confidence to support the currency. While the loonie remained under pressure through the mid-1990s, these tough measures laid the groundwork for the subsequent period of fiscal surpluses, declining debt-to-GDP ratios, and the currency's eventual recovery later in the decade.

The weak currency presented a complex economic picture. On one hand, it provided a significant boost to Canada's export-oriented sectors, such as manufacturing, forestry, and automotive industries, by making their goods cheaper on the international market. This export advantage was a crucial buffer for the economy. On the other hand, the low dollar contributed to higher costs for imported goods, putting upward pressure on consumer prices and squeezing purchasing power. It also symbolized a broader crisis of confidence in Canadian economic management, as international investors demanded a risk premium to hold Canadian assets.

The federal government's primary response was a decisive shift towards fiscal austerity. Finance Minister Paul Martin's 1995 budget, described as one of the most austere in Canadian history, implemented deep spending cuts to eliminate the federal deficit. This marked a pivotal turn away from the deficits of the previous decades and was aimed directly at restoring fiscal credibility and investor confidence to support the currency. While the loonie remained under pressure through the mid-1990s, these tough measures laid the groundwork for the subsequent period of fiscal surpluses, declining debt-to-GDP ratios, and the currency's eventual recovery later in the decade.

Series: Canadian Aviation

💎 Very Rare