50 centimes – Belgium

Add to wishlist

Belgium

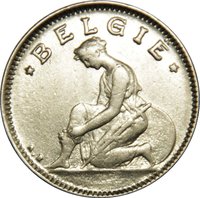

Obverse

Description:

A kneeling woman with Dutch text above and the designer's initials at left.

Inscription:

* BELGIË *

A.B

A.B

Translation:

Belgium

Albert II

Albert II

Script: Latin

Engraver: Armand Bonnetain

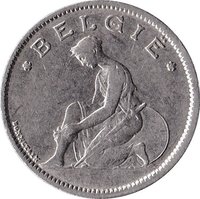

Reverse

Description:

Caduceus splits value: Dutch text above, year below.

Inscription:

❀ GOED VOOR ❀

50 CEN

❀ 1930 ❀

50 CEN

❀ 1930 ❀

Translation:

Good for

50 Cents

1930

50 Cents

1930

Script: Latin

Language: Dutch

Engraver: Armand Bonnetain

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Royal Mint of Belgium | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1923 | — | 15,000,000 | ||

| 1928 | — | 10,000,000 | ||

| 1930 | — | 2,252,000 | ||

| 1932 | — | 2,000,000 | ||

| 1933 | — | 3,139,000 | ||

| 1934 | — | 1,840,000 |

Historical background

In 1923, Belgium was grappling with the severe economic and monetary consequences of the First World War. The German occupation and the war effort had been financed largely through borrowing and the printing of money, leading to a massive expansion of the money supply and a collapse in the value of the Belgian franc. By 1923, hyperinflation, though less extreme than in neighbouring Germany, was a devastating reality, eroding savings, destabilising prices, and causing widespread social hardship. The franc's value on foreign exchanges was a fraction of its pre-war parity, and the government struggled with a heavy burden of internal debt.

The situation was exacerbated by the ongoing international crisis over German reparations, particularly the Franco-Belgian occupation of the Ruhr in January 1923. Belgium, heavily dependent on German coal and reparations payments for reconstruction, joined France in this punitive action to compel compliance. While initially providing some fiscal relief through seized resources, the occupation proved economically costly and further isolated Belgium internationally, contributing to currency volatility. Domestically, political divisions deepened over how to stabilise the economy, with debates centring on whether to return to the gold standard at the pre-war parity or devalue.

Ultimately, 1923 represented a critical juncture of crisis before eventual reform. The persistent inflation and the complex fallout from the Ruhr occupation made it clear that a drastic monetary stabilisation was unavoidable. This set the stage for the decisive actions of Finance Minister Albert-Edouard Janssen, who in 1926 would implement a successful stabilisation plan. This involved a de facto devaluation, the creation of a new gold-backed Belgian franc at a fraction of its old value, and the consolidation of the public debt, finally ending the period of monetary chaos that had characterised the early 1920s.

The situation was exacerbated by the ongoing international crisis over German reparations, particularly the Franco-Belgian occupation of the Ruhr in January 1923. Belgium, heavily dependent on German coal and reparations payments for reconstruction, joined France in this punitive action to compel compliance. While initially providing some fiscal relief through seized resources, the occupation proved economically costly and further isolated Belgium internationally, contributing to currency volatility. Domestically, political divisions deepened over how to stabilise the economy, with debates centring on whether to return to the gold standard at the pre-war parity or devalue.

Ultimately, 1923 represented a critical juncture of crisis before eventual reform. The persistent inflation and the complex fallout from the Ruhr occupation made it clear that a drastic monetary stabilisation was unavoidable. This set the stage for the decisive actions of Finance Minister Albert-Edouard Janssen, who in 1926 would implement a successful stabilisation plan. This involved a de facto devaluation, the creation of a new gold-backed Belgian franc at a fraction of its old value, and the consolidation of the public debt, finally ending the period of monetary chaos that had characterised the early 1920s.

🌱 Very Common