1 Dalasi – The Gambia

Gambia

Context

Material

Diameter: 28 mm

Weight: 8.81 g

Thickness: 1.7 mm

Shape: Heptagonal

Composition: Copper-nickel

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #Click to copy to clipboard59

Numista: #5015

Value

Exchange value: 1 GMD

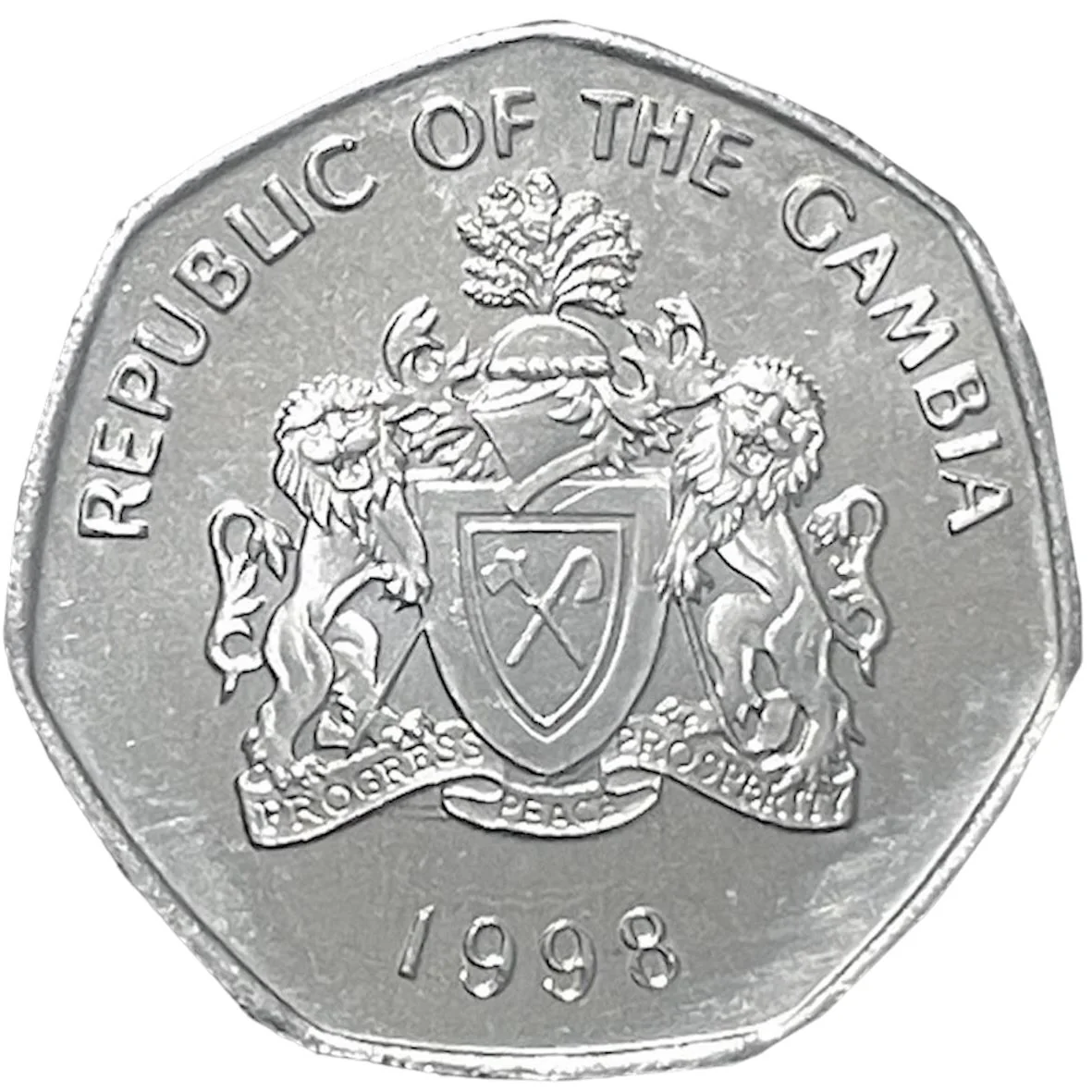

Obverse

Description:

Heraldic emblem

Inscription:

REPUBLIC OF THE GAMBIA

PROGRESS PEACE PROSPERITY

1998

PROGRESS PEACE PROSPERITY

1998

Script: Latin

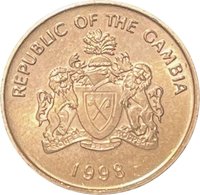

Reverse

Description:

Slender-snouted crocodile, side view.

Inscription:

1

DALASI

دَلَسِ

DALASI

دَلَسِ

Translation:

One Dalasi

Engraver: Michael Rizzello

Edge

Reeded on straight edges, plain on angles

Categories

| Animal> Reptile |

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1998 | — | — |

Historical background

In 1998, The Gambia's currency situation was defined by its continued use of the Gambian dalasi (GMD) within the framework of a managed float, following a significant devaluation earlier in the decade. The country had abandoned the fixed peg to the British pound sterling in 1986 and subsequently joined the International Monetary Fund's (IMF) Structural Adjustment Program. This led to a substantial devaluation of the dalasi in the early 1990s, a process whose effects were still being felt in 1998 as the economy adjusted to new exchange rate realities. The Central Bank of The Gambia managed the currency with the primary goals of controlling inflation and building foreign exchange reserves, but the dalasi remained under persistent pressure.

The economic backdrop in 1998 was challenging, characterized by a heavy reliance on imports, a narrow export base dominated by groundnuts and tourism, and a large fiscal deficit. These structural weaknesses exerted consistent downward pressure on the dalasi's value. Furthermore, the aftermath of the 1994 military coup, which brought President Yahya Jammeh to power, had led to a suspension of international aid. Although some donor relationships were cautiously being rebuilt by 1998, the period of isolation had strained foreign exchange reserves and limited the government's policy options for currency stabilization.

Consequently, businesses and the public in 1998 faced an environment of currency volatility and high inflation, which eroded purchasing power. The parallel (black) market for foreign exchange, particularly for hard currencies like the US dollar and British pound, remained active, often offering rates that highlighted the divergence between official policy and market realities. This situation created uncertainty for trade and investment, as the Gambian economy struggled to achieve macroeconomic stability while navigating the demands of liberalization and the legacy of political upheaval.

The economic backdrop in 1998 was challenging, characterized by a heavy reliance on imports, a narrow export base dominated by groundnuts and tourism, and a large fiscal deficit. These structural weaknesses exerted consistent downward pressure on the dalasi's value. Furthermore, the aftermath of the 1994 military coup, which brought President Yahya Jammeh to power, had led to a suspension of international aid. Although some donor relationships were cautiously being rebuilt by 1998, the period of isolation had strained foreign exchange reserves and limited the government's policy options for currency stabilization.

Consequently, businesses and the public in 1998 faced an environment of currency volatility and high inflation, which eroded purchasing power. The parallel (black) market for foreign exchange, particularly for hard currencies like the US dollar and British pound, remained active, often offering rates that highlighted the divergence between official policy and market realities. This situation created uncertainty for trade and investment, as the Gambian economy struggled to achieve macroeconomic stability while navigating the demands of liberalization and the legacy of political upheaval.

🌱 Very Common