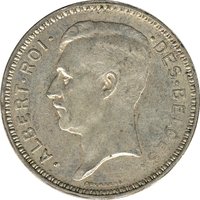

Obverse

Description:

King Albert I facing left, surrounded by French text. Designer name below.

Inscription:

· ALBERT · ROI · · DES · BELGES ·

DEVREESE

DEVREESE

Translation:

Albert, King of the Belgians

Devreese

Devreese

Script: Latin

Language: French

Engraver: Godefroid Devreese

Reverse

Description:

The Belgian coat of arms, featuring the collar of the Order of Leopold with "LR" monograms, divides the value and year. The designer's initials are below.

Inscription:

20 FR.

LR LR LR LR

G.D

1934

LR LR LR LR

G.D

1934

Script: Latin

Engraver: Godefroid Devreese

Categories

| Symbol> Crown |

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Royal Mint of Belgium | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1933 | — | 200,000 | ||

| 1934 | — | — |

Historical background

In 1933, Belgium, like much of the world, was grappling with the severe economic fallout of the Great Depression. The country had initially weathered the storm better than some due to its strong industrial base and colonial resources, but by the early 1930s, it faced plummeting exports, widespread unemployment, and significant deflationary pressures. A critical challenge was the overvaluation of the Belgian franc, which remained pegged to the gold standard at its pre-war parity—a point of national pride but an economic straitjacket. This made Belgian goods expensive on the world market, further crippling industry and deepening the crisis.

The political situation was intensely unstable, with rapid succession of governments, making decisive economic action difficult. However, a consensus was building that the franc's gold parity, defended at great cost since 1926, was unsustainable. Pressure mounted from industrialists and workers alike for a devaluation to restore competitiveness. The breaking point came in March 1935, just two years after the 1933 stalemate, when the newly formed "Government of National Unity" under Prime Minister Paul van Zeeland finally abandoned the gold standard and devalued the franc by 28%.

Thus, the currency situation in 1933 was one of prolonged tension and waiting. It was the final chapter of a costly defense of an overvalued currency, a period marked by economic suffering and political paralysis that set the stage for the decisive devaluation of 1935. This move, though delayed, ultimately allowed Belgium to begin a slow recovery by boosting exports and stimulating its domestic economy.

The political situation was intensely unstable, with rapid succession of governments, making decisive economic action difficult. However, a consensus was building that the franc's gold parity, defended at great cost since 1926, was unsustainable. Pressure mounted from industrialists and workers alike for a devaluation to restore competitiveness. The breaking point came in March 1935, just two years after the 1933 stalemate, when the newly formed "Government of National Unity" under Prime Minister Paul van Zeeland finally abandoned the gold standard and devalued the franc by 28%.

Thus, the currency situation in 1933 was one of prolonged tension and waiting. It was the final chapter of a costly defense of an overvalued currency, a period marked by economic suffering and political paralysis that set the stage for the decisive devaluation of 1935. This move, though delayed, ultimately allowed Belgium to begin a slow recovery by boosting exports and stimulating its domestic economy.

🌱 Common