100 Drachmai – Greece

Circulating commemorative coins

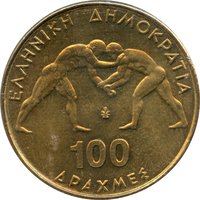

Commemoration: 45th Championship of Greco-Roman Wrestling 1999 in Athens

Greece

Obverse

Description:

Wrestlers face off

Inscription:

ΕΛΛΗΝΙΚΗ ΔΗΜΟΚΡΑΤΙΑ

100

ΔΡΑΧΜΕΣ

100

ΔΡΑΧΜΕΣ

Translation:

HELLENIC REPUBLIC

100

DRACHMAS

100

DRACHMAS

Script: Greek

Language: Greek

Engraver: Geórgios Stamatópoulos

Reverse

Description:

Throwing an opponent.

Inscription:

45Ο ΠΑΓΚΟΣΜΙΟ ΠΡΩΤΑΘΛΗΜΑ

ΑΘΗΝΑ 1999

ΓΣ

ΕΛΛΗΝΟΡΩΜΑΪΚΗΣ ΠΑΛΗΣ

ΑΘΗΝΑ 1999

ΓΣ

ΕΛΛΗΝΟΡΩΜΑΪΚΗΣ ΠΑΛΗΣ

Translation:

45th World Championship

Athens 1999

GS

Greco-Roman Wrestling

Athens 1999

GS

Greco-Roman Wrestling

Script: Greek

Language: Greek

Engraver: Geórgios Stamatópoulos

Edge

Alternating smooth and reeded segments

Categories

| Sport> Boxing or wrestling |

Mints

| Name | Mark |

|---|---|

| National Mint of the Bank of Greece | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1999 | — | — |

Historical background

In 1999, Greece's currency situation was defined by its determined but unfulfilled push to join the newly launched Eurozone. While eleven other European Union members, including economic powerhouses like Germany and France, adopted the euro as their common currency on January 1st, Greece was conspicuously absent. This exclusion was a direct result of its failure to meet the strict convergence criteria (the Maastricht Treaty criteria) for inflation rates, budget deficits, public debt, interest rates, and exchange rate stability. Greece's economy was still grappling with the structural reforms needed to align with the stability-oriented policies of the European Central Bank.

The primary obstacle was Greece's high public debt, which far exceeded the Maastricht limit of 60% of GDP, and its history of fiscal deficits. Throughout the 1990s, successive Greek governments had implemented austerity measures and economic reforms with the singular political goal of euro adoption. However, by 1999, the country's economic data, as reported to the EU, was still not deemed sufficient. Consequently, the Greek drachma remained the national currency, though it was now part of the new Exchange Rate Mechanism II (ERM II), which pegged it to the euro with a central rate. This was a mandatory "waiting room" designed to ensure exchange rate stability before full euro membership.

The year 1999, therefore, was one of intense preparation and renewed commitment for Greece. The government, led by Prime Minister Costas Simitis, redoubled its efforts to tighten fiscal policy, curb inflation, and accelerate privatization. Crucially, a major statistical revision was underway that would, by 2000, retrospectively show Greece had met the deficit criterion in 1999. This controversial data revision paved the way for the European Council to grant Greece membership in June 2000, setting the stage for its formal adoption of the euro on January 1, 2001, with euro banknotes and coins entering circulation a year later.

The primary obstacle was Greece's high public debt, which far exceeded the Maastricht limit of 60% of GDP, and its history of fiscal deficits. Throughout the 1990s, successive Greek governments had implemented austerity measures and economic reforms with the singular political goal of euro adoption. However, by 1999, the country's economic data, as reported to the EU, was still not deemed sufficient. Consequently, the Greek drachma remained the national currency, though it was now part of the new Exchange Rate Mechanism II (ERM II), which pegged it to the euro with a central rate. This was a mandatory "waiting room" designed to ensure exchange rate stability before full euro membership.

The year 1999, therefore, was one of intense preparation and renewed commitment for Greece. The government, led by Prime Minister Costas Simitis, redoubled its efforts to tighten fiscal policy, curb inflation, and accelerate privatization. Crucially, a major statistical revision was underway that would, by 2000, retrospectively show Greece had met the deficit criterion in 1999. This controversial data revision paved the way for the European Council to grant Greece membership in June 2000, setting the stage for its formal adoption of the euro on January 1, 2001, with euro banknotes and coins entering circulation a year later.

🌱 Very Common