5 cents – United States

Add to wishlist

Circulating commemorative coins

Commemoration: Bicentennial of The Lewis and Clark Expedition

Series: Westward Journey

United States

Context

Year: 2005

Issuer: United States

Period:

(since 1776)

Currency:

(since 1785)

Total mintage: 808,544,679

Material

Diameter: 21.21 mm

Weight: 5 g

Thickness: 1.95 mm

Shape: Round

Composition: Copper-nickel

Technique: Milled

Alignment: Coin alignment

flip

References

KM: #

Numista: #49

Value

Exchange value: 0.05 USD = $0.05

Inflation-adjusted value: 0.08 USD

Obverse

Description:

A right-profile portrait of Thomas Jefferson, the 3rd U.S. President, is accompanied by his handwritten "Liberty" and encircled by the motto "IN GOD WE TRUST."

Inscription:

IN GOD WE TRUST

Liberty

S

JF DE 2005

Liberty

S

JF DE 2005

Script: Latin

Engravers: Joe Fitzgerald, Don Everhart

Reverse

Description:

Pacific coast pine forest.

Inscription:

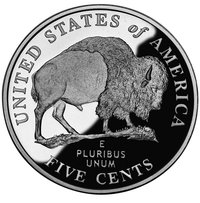

E PLURIBUS UNUM • UNITED STATES OF AMERICA

Ocean

in view!

O! The joy!

JF DW

• LEWIS & CLARK 1805 • FIVE CENTS •

Ocean

in view!

O! The joy!

JF DW

• LEWIS & CLARK 1805 • FIVE CENTS •

Translation:

Out of many, one. United States of America

Ocean

in view!

O! The joy!

JF DW

Lewis & Clark 1805. Five cents.

Ocean

in view!

O! The joy!

JF DW

Lewis & Clark 1805. Five cents.

Script: Latin

Engravers: Joe Fitzgerald, Donna Weaver

Edge

Plain

Mints

| Name | Mark |

|---|---|

| United States Mint of Denver | D |

| United States Mint of Philadelphia | P |

| United States Mint of San Francisco | S |

Historical background

In 2005, the United States currency situation was characterized by a period of relative stability for the U.S. dollar on foreign exchange markets, but underlying concerns about growing macroeconomic imbalances. The dollar had experienced a multi-year decline since 2002, but this depreciation moderated significantly in 2005. The Dollar Index, which measures the dollar against a basket of major currencies, actually rose approximately 13% that year. This strength was largely driven by the Federal Reserve's steady interest rate hikes, which made dollar-denominated assets more attractive to global investors seeking higher returns. This monetary policy tightening was a response to domestic concerns about inflation, fueled by rising energy prices.

However, this surface strength masked significant long-term vulnerabilities. The U.S. was running a massive and growing current account deficit, exceeding 6% of GDP, meaning it was consuming far more from the rest of the world than it exported. This deficit was financed by substantial capital inflows from foreign governments, particularly in Asia. Central banks in China, Japan, and other export-oriented economies actively purchased U.S. Treasury securities to manage their own exchange rates and sustain demand for their goods, creating a symbiotic but precarious financial relationship often termed "Bretton Woods II." Domestically, the housing market boom was nearing its peak, fueled by easy credit, while household savings rates plummeted, adding to the economy's debt-fueled structure.

The prevailing consensus among policymakers, including then-Federal Reserve Chairman Alan Greenspan, was that global financial markets would smoothly adjust these imbalances over time. The dominant view held that the dollar's role as the world's primary reserve currency was secure. Consequently, there was little sense of immediate crisis in 2005, but rather a background hum of warning from economists about the sustainability of U.S. external deficits and the potential for a disorderly dollar correction should foreign investors' appetite for U.S. assets wane. The vulnerabilities accumulating in this period would later be exposed during the 2007-2008 global financial crisis.

However, this surface strength masked significant long-term vulnerabilities. The U.S. was running a massive and growing current account deficit, exceeding 6% of GDP, meaning it was consuming far more from the rest of the world than it exported. This deficit was financed by substantial capital inflows from foreign governments, particularly in Asia. Central banks in China, Japan, and other export-oriented economies actively purchased U.S. Treasury securities to manage their own exchange rates and sustain demand for their goods, creating a symbiotic but precarious financial relationship often termed "Bretton Woods II." Domestically, the housing market boom was nearing its peak, fueled by easy credit, while household savings rates plummeted, adding to the economy's debt-fueled structure.

The prevailing consensus among policymakers, including then-Federal Reserve Chairman Alan Greenspan, was that global financial markets would smoothly adjust these imbalances over time. The dominant view held that the dollar's role as the world's primary reserve currency was secure. Consequently, there was little sense of immediate crisis in 2005, but rather a background hum of warning from economists about the sustainability of U.S. external deficits and the potential for a disorderly dollar correction should foreign investors' appetite for U.S. assets wane. The vulnerabilities accumulating in this period would later be exposed during the 2007-2008 global financial crisis.

🌱 Very Common