50 Tambala – Malawi

Malawi

Context

Years: 1986–1994

Issuer: Malawi

Period:

(since 1966)

Ruler: Hastings Kamuzu Banda

Currency:

(since 1971)

Material

Diameter: 30 mm

Weight: 11.35 g

Thickness: 2 mm

Shape: Round

Composition: Nickel brass

Magnetic: No

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #Click to copy to clipboard19

Numista: #4776

Value

Exchange value: 0.50 MWK

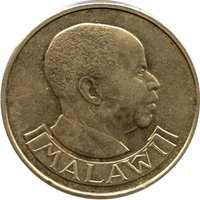

Obverse

Description:

Portrait of Hastings Kamuzu Banda.

Inscription:

MALAWI

Script: Latin

Designer: Paul Vincze

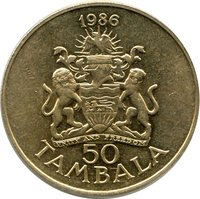

Reverse

Edge

Milled

Categories

| Symbols> Coat of Arms |

| Person> Politician |

Mints

| Name | Mark |

|---|---|

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1986 | — | — | ||

| 1994 | — | — |

Historical background

In 1986, Malawi's currency situation was defined by the persistent overvaluation of the Kwacha, managed under a fixed exchange rate regime pegged to a basket of currencies. This policy, maintained by the government of President-for-Life Dr. Hastings Kamuzu Banda, was a cornerstone of economic management aimed at ensuring stability and keeping the cost of imports—particularly essential goods, inputs for the agricultural estate sector, and luxury items for the elite—artificially low. However, this rigidity created a significant disconnect from economic reality, discouraging exports and leading to chronic foreign exchange shortages.

The overvalued Kwacha fostered a thriving black market for foreign currency, where the exchange rate was significantly higher than the official rate. This parallel market became essential for businesses unable to access sufficient foreign exchange through official channels, but it introduced major distortions and inefficiencies into the economy. Furthermore, the policy placed severe strain on the country's reserves and contributed to a growing debt burden, as the government borrowed to maintain the peg and finance trade imbalances.

International financial institutions, notably the International Monetary Fund (IMF), increasingly pressured the Malawian government to devalue the Kwacha and adopt structural adjustment programs to correct these imbalances. While minor adjustments were made, a major devaluation was resisted until the following year. Thus, 1986 represented the tail end of an unsustainable monetary policy, characterized by mounting internal and external pressures that would force a significant and painful currency correction in 1987.

The overvalued Kwacha fostered a thriving black market for foreign currency, where the exchange rate was significantly higher than the official rate. This parallel market became essential for businesses unable to access sufficient foreign exchange through official channels, but it introduced major distortions and inefficiencies into the economy. Furthermore, the policy placed severe strain on the country's reserves and contributed to a growing debt burden, as the government borrowed to maintain the peg and finance trade imbalances.

International financial institutions, notably the International Monetary Fund (IMF), increasingly pressured the Malawian government to devalue the Kwacha and adopt structural adjustment programs to correct these imbalances. While minor adjustments were made, a major devaluation was resisted until the following year. Thus, 1986 represented the tail end of an unsustainable monetary policy, characterized by mounting internal and external pressures that would force a significant and painful currency correction in 1987.

🌱 Common