1 sol – Peru

Add to wishlist

Peru

Material

Diameter: 25.5 mm

Weight: 7.32 g

Shape: Round

Composition: Nickel brass

Magnetic: No

Technique: Milled

Alignment: Coin alignment

flip

References

KM: #

Numista: #47264

Value

Exchange value: 1 PEN

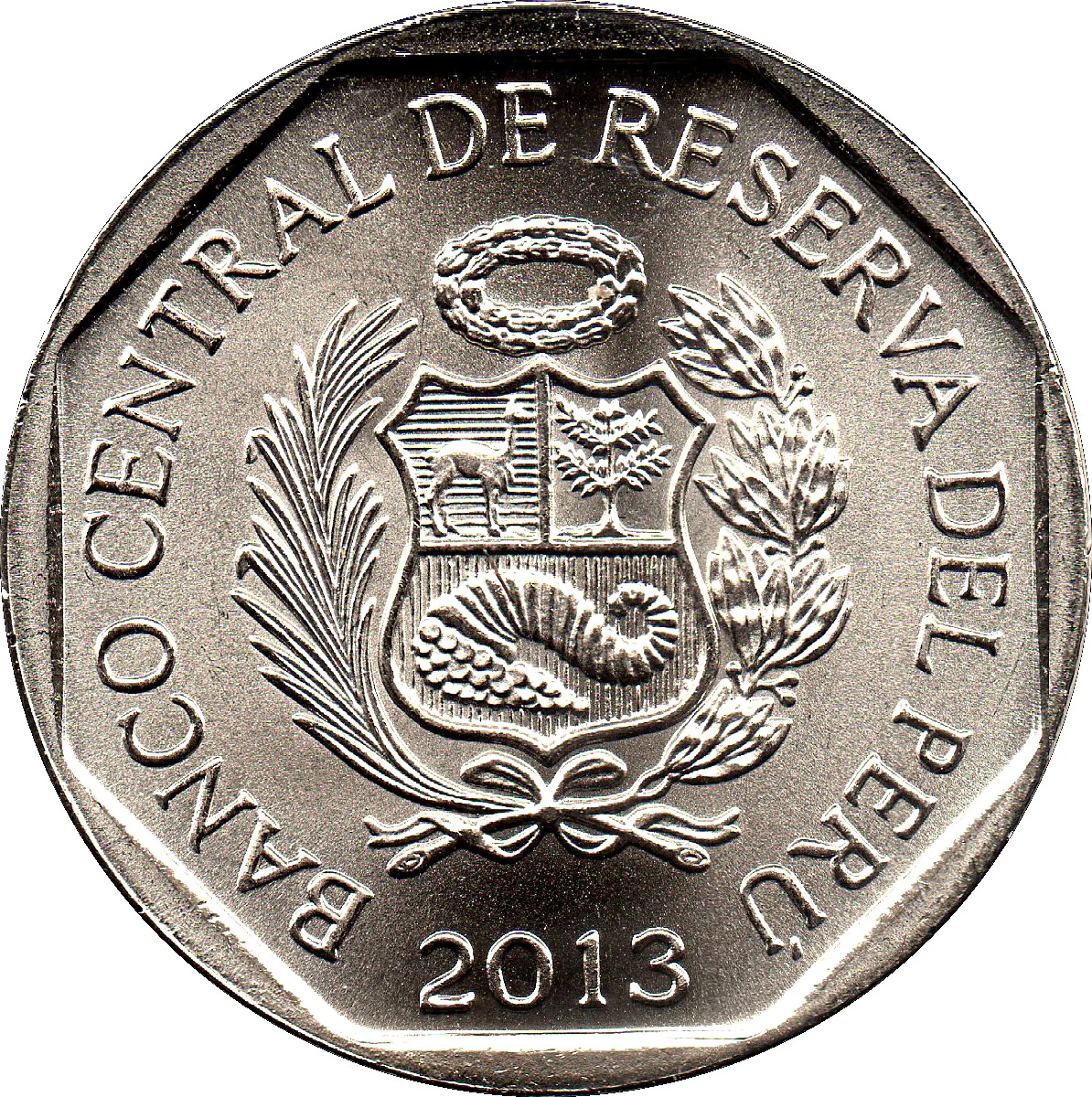

Obverse

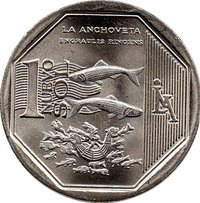

Reverse

Edge

Reeded

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2013 | LIMA | 10,000,000 |

Historical background

In 2013, Peru's currency, the nuevo sol (PEN), demonstrated notable resilience and strength, continuing a multi-year trend of appreciation against the US dollar. This was largely driven by robust foreign direct investment, particularly in the mining sector, and sustained high prices for Peru's key commodity exports like copper, gold, and silver. These capital inflows increased the supply of dollars in the local economy, pushing the sol's value higher. The Central Reserve Bank of Peru (BCRP) actively intervened in the foreign exchange market through pre-announced dollar purchases to moderate the pace of appreciation, aiming to protect the competitiveness of non-traditional exports and maintain financial stability.

The strong sol presented a policy dilemma. While it helped keep inflation low and imported goods affordable, it also raised concerns from exporters and industrial sectors about eroded profitability and "Dutch disease," where a resource boom harms other industries. Domestically, the economy was growing at a healthy clip, but there were emerging signs of a slowdown from the high growth rates of previous years. Inflation remained within the BCRP's target range of 1-3%, allowing the central bank to maintain a relatively accommodative monetary policy to support economic activity.

By the end of 2013, the nuevo sol had appreciated approximately 4.5% against the US dollar for the year, marking one of the strongest performances among emerging market currencies. This strength was a testament to Peru's macroeconomic stability and its appeal to foreign investors, but it also underscored the ongoing challenges of managing a small, open economy heavily dependent on volatile commodity cycles and external capital flows. The BCRP's managed float regime and accumulation of international reserves were key tools in navigating this complex environment.

The strong sol presented a policy dilemma. While it helped keep inflation low and imported goods affordable, it also raised concerns from exporters and industrial sectors about eroded profitability and "Dutch disease," where a resource boom harms other industries. Domestically, the economy was growing at a healthy clip, but there were emerging signs of a slowdown from the high growth rates of previous years. Inflation remained within the BCRP's target range of 1-3%, allowing the central bank to maintain a relatively accommodative monetary policy to support economic activity.

By the end of 2013, the nuevo sol had appreciated approximately 4.5% against the US dollar for the year, marking one of the strongest performances among emerging market currencies. This strength was a testament to Peru's macroeconomic stability and its appeal to foreign investors, but it also underscored the ongoing challenges of managing a small, open economy heavily dependent on volatile commodity cycles and external capital flows. The BCRP's managed float regime and accumulation of international reserves were key tools in navigating this complex environment.

🌱 Common