1 florin – United Kingdom

Add to wishlist

United Kingdom

Context

Years: 1902–1910

Issuer: United Kingdom

Ruler: Edward VII

Currency:

(1158—1970)

Demonetization: 30 June 1993

Total mintage: 33,727,900

Material

References

KM: #

Numista: #4716

Value

Bullion value: $26.11

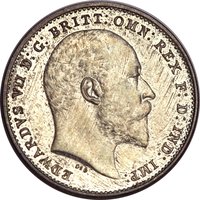

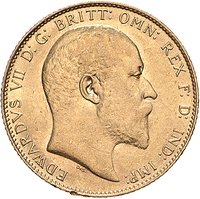

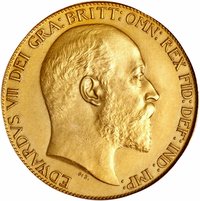

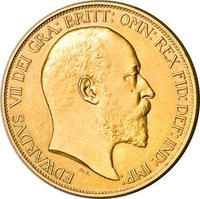

Obverse

Description:

King Edward VII, bareheaded, facing right with surrounding legend.

Inscription:

EDWARDVS VII D:G: BRITT:OMN: REX F:D: IND: IMP:

DES

DES

Translation:

Edward VII by the Grace of God King of all the Britains Defender of the Faith Emperor of India

Script: Latin

Language: Latin

Engraver: George William de Saulles

Reverse

Description:

Britannia standing on a ship's bow, holding a trident and a Union Jack shield, with legend around and date below.

Inscription:

ONE FLORIN TWO SHILLINGS

1906

1906

Script: Latin

Engraver: George William de Saulles

Edge

Reeded

Categories

| Transportation> Watercraft |

| Object> Cold weapons |

| Object> Armour |

| Geography> Sea |

Mints

| Name | Mark |

|---|---|

| Royal Mint (Tower Hill) | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1902 | — | 2,489,500 | ||

| 1902 | — | 15,000 | Proof | |

| 1903 | — | 1,995,200 | ||

| 1904 | — | 2,769,900 | ||

| 1905 | — | 1,187,500 | ||

| 1906 | — | 6,910,100 | ||

| 1907 | — | 5,947,800 | ||

| 1908 | — | 3,280,000 | ||

| 1909 | — | 3,482,200 | ||

| 1910 | — | 5,650,700 |

Historical background

In 1902, the United Kingdom operated under the classical gold standard, a system it had effectively pioneered and which underpinned its global financial dominance. The pound sterling was legally defined as a specific weight of gold (approximately 7.3 grams of fine gold), and Bank of England notes were freely convertible into gold coin upon demand. This "gold sovereign" and its half, the half-sovereign, circulated widely alongside smaller silver and copper token coinage for everyday transactions. The system's rigidity and credibility were seen as the bedrock of London's status as the world's premier financial centre, facilitating vast international trade and investment.

The currency situation was one of remarkable stability in terms of external value, but not without domestic debate. The period was characterised by a relative scarcity of circulating gold coin in daily life, especially following the Bank Charter Act of 1844, which had restricted the issuance of banknotes. Instead, the economy relied heavily on banknotes issued by the Bank of England and, in Scotland and Ireland, by certain commercial banks. There was ongoing political and economic discussion regarding the need for a wider issue of low-denomination Treasury notes to improve everyday liquidity, a debate that would eventually culminate in the 1914 currency reforms following the outbreak of the First World War.

Furthermore, the UK's monetary policy was largely automatic under the gold standard; the Bank of England's primary role was to maintain convertibility. Interest rates were adjusted to protect the nation's gold reserves, influencing domestic credit conditions. While this ensured long-term price stability, it could lead to short-term economic hardship, such as deflationary pressures, to correct trade imbalances. Thus, in 1902, the currency system was both a symbol of immense imperial prestige and a rigid framework that would, within little over a decade, be severely tested by the financial demands of total war.

The currency situation was one of remarkable stability in terms of external value, but not without domestic debate. The period was characterised by a relative scarcity of circulating gold coin in daily life, especially following the Bank Charter Act of 1844, which had restricted the issuance of banknotes. Instead, the economy relied heavily on banknotes issued by the Bank of England and, in Scotland and Ireland, by certain commercial banks. There was ongoing political and economic discussion regarding the need for a wider issue of low-denomination Treasury notes to improve everyday liquidity, a debate that would eventually culminate in the 1914 currency reforms following the outbreak of the First World War.

Furthermore, the UK's monetary policy was largely automatic under the gold standard; the Bank of England's primary role was to maintain convertibility. Interest rates were adjusted to protect the nation's gold reserves, influencing domestic credit conditions. While this ensured long-term price stability, it could lead to short-term economic hardship, such as deflationary pressures, to correct trade imbalances. Thus, in 1902, the currency system was both a symbol of immense imperial prestige and a rigid framework that would, within little over a decade, be severely tested by the financial demands of total war.

🌱 Common