5 Cents – United States

United States

Context

Years: 1866–1867

Issuer: United States

Period:

(since 1776)

Currency:

(since 1785)

Total mintage: 16,762,160

Material

References

KM: #Click to copy to clipboard96

Numista: #14852

Value

Exchange value: 0.05 USD = $0.05

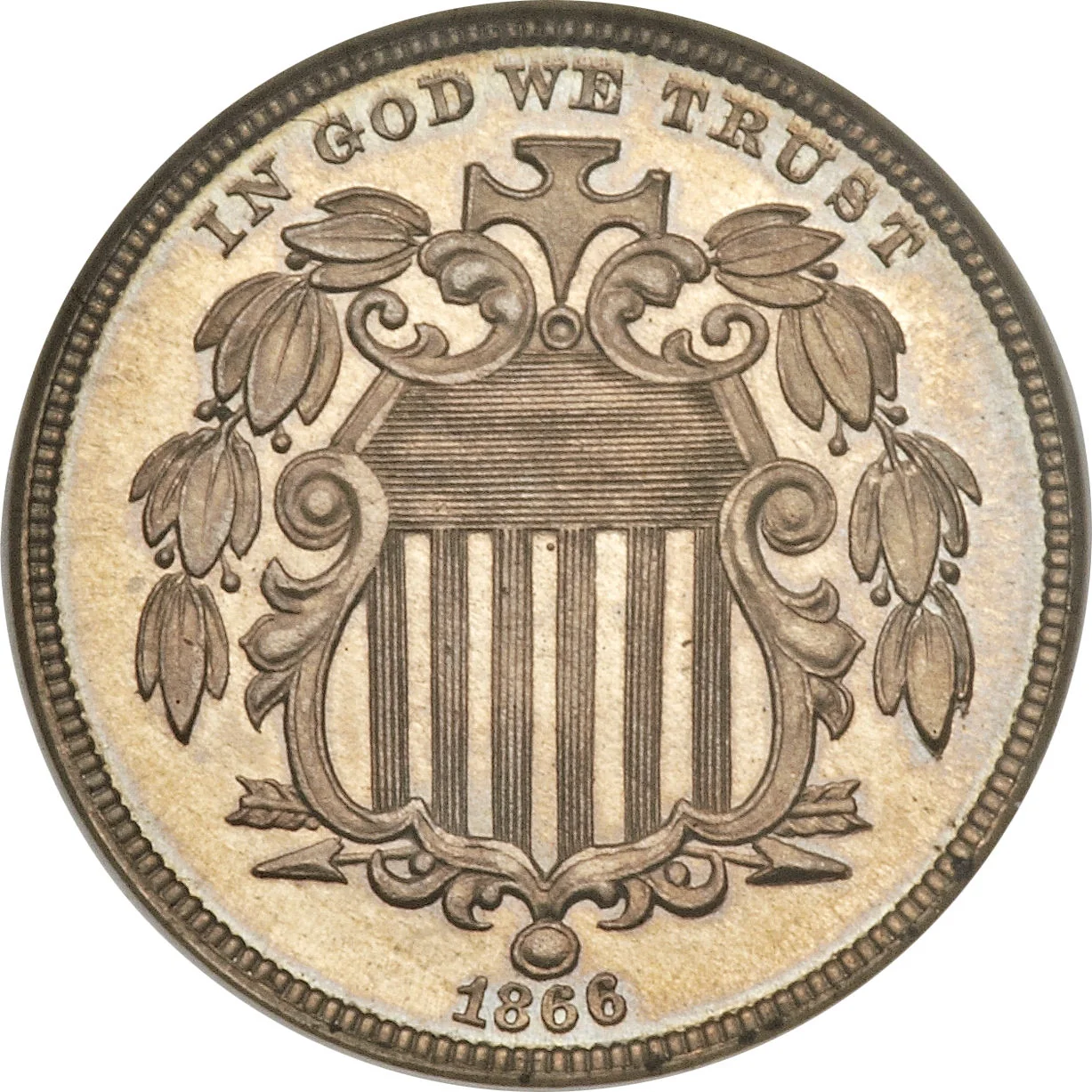

Obverse

Description:

Garland over shield

Inscription:

IN GOD WE TRUST

1866

1866

Script: Latin

Engraver: James Barton Longacre

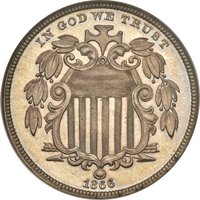

Reverse

Description:

Centered among 13 stars and rays.

Inscription:

UNITED STATES OF AMERICA

5

·CENTS·

5

·CENTS·

Script: Latin

Engraver: James Barton Longacre

Edge

Plain

Categories

| Object> Cold weapons |

Mints

| Name | Mark |

|---|---|

| United States Mint of Philadelphia | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1866 | — | 14,742,500 | ||

| 1866 | — | 600 | Proof | |

| 1867 | — | 2,019,000 | ||

| 1867 | — | 60 | Proof |

Historical background

In 1866, the United States was grappling with the profound monetary consequences of the Civil War, which had ended just a year earlier. The federal government had financed the conflict not only through taxes and bonds but also by issuing over $450 million in "greenbacks"—paper notes declared legal tender but not redeemable in gold or silver. This created a dual-currency system: gold-backed money and a fluctuating paper currency. The greenbacks had depreciated significantly against gold during the war, leading to price inflation and a contentious debate between "hard money" advocates (who wanted a swift return to the gold standard) and "soft money" proponents (who favored retaining or even expanding the paper currency to aid debtors and foster economic growth).

Politically, the battle over currency was crystallizing in Congress. Hard money interests, led by Secretary of the Treasury Hugh McCulloch, were in the ascendant. McCulloch championed a policy of contraction, aiming to gradually retire the greenbacks from circulation to restore the nation's pre-war gold standard and stabilize the dollar. This policy was aligned with commercial and banking interests in the Northeast but was fiercely opposed by farmers, manufacturers, and many in the Midwest and South who feared that reducing the money supply would cause deflation, lower crop prices, and make it harder to pay off war-incurred debts.

The year proved pivotal for the contractionists. In April 1866, Congress passed the Contraction Act, authorizing the Treasury to retire up to $10 million of greenbacks within six months and up to $4 million per month thereafter. This legislative victory for the gold standard set the nation on a path toward the "Resumption" of specie payments, which would ultimately be achieved in 1879. However, the act also intensified regional and class divisions over money, sparking a political backlash that would fuel the Greenback movement of the 1870s. Thus, 1866 stands as a defining moment where the U.S. government decisively, though controversially, chose a path of monetary contraction in the difficult postwar transition.

Politically, the battle over currency was crystallizing in Congress. Hard money interests, led by Secretary of the Treasury Hugh McCulloch, were in the ascendant. McCulloch championed a policy of contraction, aiming to gradually retire the greenbacks from circulation to restore the nation's pre-war gold standard and stabilize the dollar. This policy was aligned with commercial and banking interests in the Northeast but was fiercely opposed by farmers, manufacturers, and many in the Midwest and South who feared that reducing the money supply would cause deflation, lower crop prices, and make it harder to pay off war-incurred debts.

The year proved pivotal for the contractionists. In April 1866, Congress passed the Contraction Act, authorizing the Treasury to retire up to $10 million of greenbacks within six months and up to $4 million per month thereafter. This legislative victory for the gold standard set the nation on a path toward the "Resumption" of specie payments, which would ultimately be achieved in 1879. However, the act also intensified regional and class divisions over money, sparking a political backlash that would fuel the Greenback movement of the 1870s. Thus, 1866 stands as a defining moment where the U.S. government decisively, though controversially, chose a path of monetary contraction in the difficult postwar transition.

🌱 Common