2 centésimos – Uruguay

Add to wishlist

Uruguay

Context

Year: 1953

Issuer: Uruguay

Issuing organization: Bank of Oriental Republic of Uruguay

Period:

(since 1825)

Currency:

(1863—1975)

Demonetization: 1 July 1975

Total mintage: 50,000,000

Material

Diameter: 17 mm

Weight: 2.5 g

Thickness: 1 mm

Shape: Round

Composition: Copper-nickel

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #4633

Value

Exchange value: 0.02 UYP

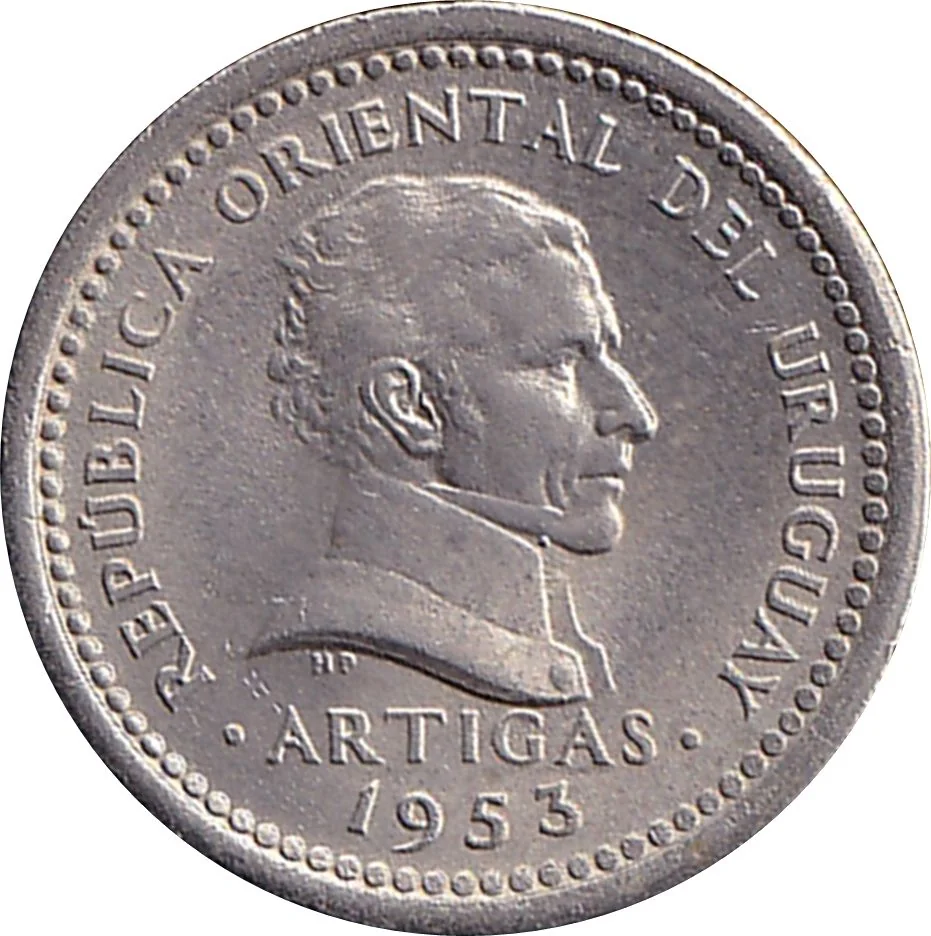

Obverse

Description:

Portrait of José Artigas facing right, encircled by country name and a dotted border. Name below, date at bottom. Engraver's initials under shoulder.

Inscription:

REPÚBLICA ORIENTAL DEL URUGUAY

HP

• ARTIGAS •

1953

HP

• ARTIGAS •

1953

Translation:

Eastern Republic of Uruguay

HP

• ARTIGAS •

1953

HP

• ARTIGAS •

1953

Script: Latin

Language: Spanish

Engraver: Thomas Humphrey Paget

Reverse

Description:

Laurel Wreath Value

Inscription:

2

CENTÉSIMOS

CENTÉSIMOS

Translation:

Two Centésimos

Script: Latin

Language: Spanish

Engraver: Thomas Humphrey Paget

Edge

Plain

Categories

| Symbol> Wreath |

| Person> Military leader |

| Person> Politician |

Mints

| Name | Mark |

|---|---|

| Royal Mint (Tower Hill) | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1953 | — | 50,000,000 | ||

| 1953 | — | — | Proof |

Historical background

By 1953, Uruguay was grappling with the severe economic consequences of the long-standing Batllista model, which had prioritized a generous welfare state and industrial protectionism funded primarily by booming wool and beef exports. The post-Korean War collapse in global commodity prices exposed the structural weaknesses of this system, leading to chronic fiscal deficits, dwindling foreign reserves, and persistent balance of payments crises. The peso, which had been historically stable, came under intense pressure, forcing the government to rely on a complex and unsustainable system of multiple exchange rates and stringent import controls to manage the currency and conserve hard currency.

President Andrés Martínez Trueba, leading a weak collegial executive (the Consejo Nacional de Gobierno), faced this crisis with limited tools. The Central Bank struggled to defend the official parity, leading to a thriving black market for U.S. dollars where the peso traded at a significant discount. This multi-tiered system—different rates for essential imports, non-essentials, and financial transactions—created distortions, encouraged speculation, and hampered economic planning. Inflation began to accelerate, eroding the purchasing power of wages and undermining the social peace that had characterized mid-century Uruguay.

The currency instability of 1953 was a critical symptom of a deeper economic malaise, marking the beginning of the end of Uruguay's "Switzerland of America" prosperity. Efforts to stabilize the peso were largely stopgap, as the government was politically constrained from making the sharp fiscal adjustments needed. This period set the stage for the more severe stagflation and monetary crises that would define the latter half of the 1950s and 1960s, ultimately contributing to social unrest and the political upheavals that followed.

President Andrés Martínez Trueba, leading a weak collegial executive (the Consejo Nacional de Gobierno), faced this crisis with limited tools. The Central Bank struggled to defend the official parity, leading to a thriving black market for U.S. dollars where the peso traded at a significant discount. This multi-tiered system—different rates for essential imports, non-essentials, and financial transactions—created distortions, encouraged speculation, and hampered economic planning. Inflation began to accelerate, eroding the purchasing power of wages and undermining the social peace that had characterized mid-century Uruguay.

The currency instability of 1953 was a critical symptom of a deeper economic malaise, marking the beginning of the end of Uruguay's "Switzerland of America" prosperity. Efforts to stabilize the peso were largely stopgap, as the government was politically constrained from making the sharp fiscal adjustments needed. This period set the stage for the more severe stagflation and monetary crises that would define the latter half of the 1950s and 1960s, ultimately contributing to social unrest and the political upheavals that followed.

Series: 1953 Uruguay circulation coins

🌱 Very Common