1 peso – Dominican Republic

Add to wishlist

Dominican Republic

Context

Years: 2008–2018

Issuer: Dominican Republic

Period:

(since 1966)

Currency:

(since 1937)

Total mintage: 195,000,000

Material

Diameter: 25 mm

Weight: 6.4 g

Thickness: 2.1 mm

Shape: Hendecagonal

Magnetic: Yes

Technique: Milled

Alignment: Coin alignment

flip

References

KM: #

Numista: #45819

Value

Exchange value: 1 DOP

Obverse

Reverse

Description:

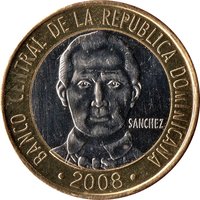

Portrait of Juan Pablo Duarte (1813–1876), a founding father of the Dominican Republic.

Inscription:

PADRE DE LA PATRIA

DUARTE

2008

DUARTE

2008

Script: Latin

Edge

Plain

Mints

| Name | Mark |

|---|---|

| Mint of Poland | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2008 | — | 40,000,000 | ||

| 2014 | — | 30,000,000 | ||

| 2015 | — | 15,000,000 | ||

| 2016 | — | 40,000,000 | ||

| 2017 | — | 20,000,000 | ||

| 2018 | — | 50,000,000 |

Historical background

In 2008, the Dominican Republic faced significant currency pressures stemming from the global financial crisis and domestic economic vulnerabilities. The Dominican peso (DOP), which had been relatively stable for several years under a managed float regime, came under intense downward pressure. Key drivers included a sharp decline in remittances and tourism revenue—two critical sources of foreign exchange—as the recession hit the United States and other major source countries. Furthermore, soaring global prices for oil and food in the first half of the year widened the trade deficit, increasing demand for US dollars to pay for imports and putting additional strain on international reserves.

The Central Bank of the Dominican Republic (BCRD) intervened aggressively to defend the peso, selling dollars from its reserves to slow depreciation. This policy, however, led to a significant depletion of foreign reserves, which fell by approximately 30% during the year. Despite these interventions, the peso depreciated by about 5.5% against the US dollar in the official market over the course of 2008, with greater pressure visible in the parallel market. The situation created a climate of uncertainty for businesses and increased the cost of servicing foreign-denominated debt.

By late 2008, the BCRD shifted its strategy in response to the sustained pressure and falling reserves. It began to allow for greater exchange rate flexibility, easing its direct interventions to conserve reserves. This controlled depreciation was part of a broader adjustment to the external shocks, helping to correct imbalances. The currency situation was a central challenge within the wider 2008-2009 economic slowdown, prompting authorities to later seek a precautionary standby agreement with the International Monetary Fund in 2009 to bolster confidence and provide a buffer for the balance of payments.

The Central Bank of the Dominican Republic (BCRD) intervened aggressively to defend the peso, selling dollars from its reserves to slow depreciation. This policy, however, led to a significant depletion of foreign reserves, which fell by approximately 30% during the year. Despite these interventions, the peso depreciated by about 5.5% against the US dollar in the official market over the course of 2008, with greater pressure visible in the parallel market. The situation created a climate of uncertainty for businesses and increased the cost of servicing foreign-denominated debt.

By late 2008, the BCRD shifted its strategy in response to the sustained pressure and falling reserves. It began to allow for greater exchange rate flexibility, easing its direct interventions to conserve reserves. This controlled depreciation was part of a broader adjustment to the external shocks, helping to correct imbalances. The currency situation was a central challenge within the wider 2008-2009 economic slowdown, prompting authorities to later seek a precautionary standby agreement with the International Monetary Fund in 2009 to bolster confidence and provide a buffer for the balance of payments.

🌱 Very Common