50 francs – Rwanda

Add to wishlist

Rwanda

Context

Material

Diameter: 40 mm

Weight: 31.1 g

Silver Weight:: 31.07 g

Thickness: 3.14 mm

Shape: Round

Composition: 99.9% Silver

Standard: Silver ounce

Magnetic: No

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #45678

Value

Exchange value: 50 RWF

Bullion value: $77.46

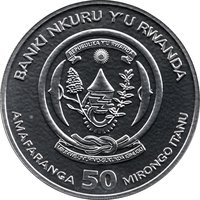

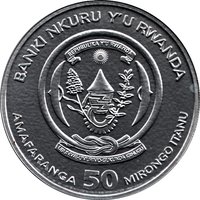

Obverse

Description:

Rwanda's national emblem.

Inscription:

BANKI NKURU Y'U RWANDA

REPUBLIKA Y'U RWANDA

UBUMWI - UMURIMO - GUKUNDA IGIHUGU

AMAFARANGA 50 MIRONGO ITANU

REPUBLIKA Y'U RWANDA

UBUMWI - UMURIMO - GUKUNDA IGIHUGU

AMAFARANGA 50 MIRONGO ITANU

Translation:

BANKI NKURU Y'U RWANDA - National Bank of Rwanda

REPUBLIKA Y'U RWANDA - Republic of Rwanda

UBUMWI - UMURIMO - GUKUNDA IGIHUGU - Unity - Work - Patriotism

AMAFARANGA 50 MIRONGO ITANU - 50 Francs

REPUBLIKA Y'U RWANDA - Republic of Rwanda

UBUMWI - UMURIMO - GUKUNDA IGIHUGU - Unity - Work - Patriotism

AMAFARANGA 50 MIRONGO ITANU - 50 Francs

Script: Latin

Language: Kinyarwanda

Reverse

Description:

Three elephants at left, Africa outline at right.

Inscription:

AFRICAN OUNCE 2009

1oz FINE SILVER 999

1oz FINE SILVER 999

Script: Latin

Edge

Reeded

Categories

| Animal> Elephant |

| Symbols> Coat of Arms |

| Map |

Mints

| Name | Mark |

|---|---|

| B. H. Mayer Kunstprageanstalt | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2009 | — | 5,000 |

Historical background

In 2009, Rwanda's currency situation was characterized by relative stability and cautious optimism, a significant achievement following the devastating genocide and hyperinflation of the mid-1990s. The Rwandan franc (RWF) was managed under a flexible exchange rate regime by the National Bank of Rwanda (BNR), with its value primarily determined by market forces of supply and demand. This period saw low and stable inflation, averaging around 10.3% for the year, which allowed the central bank to gradually reduce its policy rate to stimulate private sector credit and economic growth. The currency's stability was underpinned by sound fiscal management, substantial donor support, and growing exports, particularly from the coffee and tea sectors.

However, the year was not without pressures. Rwanda, as a landlocked and import-dependent nation, remained vulnerable to external shocks. The global financial crisis of 2008-2009 led to a decline in export demand and foreign direct investment, creating some downward pressure on the franc. Furthermore, the country's trade deficit posed a persistent challenge, as the need to import fuel, food, and capital goods consistently created higher demand for foreign currency (especially US dollars) than the supply generated by exports and remittances. The BNR actively monitored this volatility and maintained foreign exchange reserves to smooth out excessive fluctuations without targeting a specific exchange rate.

Overall, the 2009 currency landscape reflected Rwanda's broader economic narrative of post-conflict recovery and disciplined reform. The government's commitment to macroeconomic stability, supported by programs with the International Monetary Fund (IMF), provided a solid anchor for the franc. This environment of monetary stability was crucial for fostering investor confidence and supporting the country's ambitious development goals, as outlined in its Vision 2020 framework, which aimed to transform Rwanda into a middle-income nation.

However, the year was not without pressures. Rwanda, as a landlocked and import-dependent nation, remained vulnerable to external shocks. The global financial crisis of 2008-2009 led to a decline in export demand and foreign direct investment, creating some downward pressure on the franc. Furthermore, the country's trade deficit posed a persistent challenge, as the need to import fuel, food, and capital goods consistently created higher demand for foreign currency (especially US dollars) than the supply generated by exports and remittances. The BNR actively monitored this volatility and maintained foreign exchange reserves to smooth out excessive fluctuations without targeting a specific exchange rate.

Overall, the 2009 currency landscape reflected Rwanda's broader economic narrative of post-conflict recovery and disciplined reform. The government's commitment to macroeconomic stability, supported by programs with the International Monetary Fund (IMF), provided a solid anchor for the franc. This environment of monetary stability was crucial for fostering investor confidence and supporting the country's ambitious development goals, as outlined in its Vision 2020 framework, which aimed to transform Rwanda into a middle-income nation.

Series: African Ounce

💎 Extremely Rare