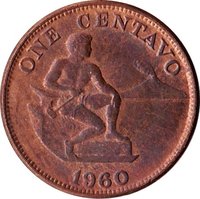

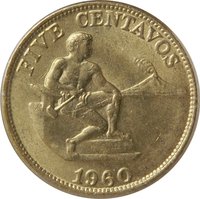

10 centavos – Philippines

Add to wishlist

Philippines

Context

Years: 1958–1966

Issuer: Philippines

Issuing organization: Central Bank of the Philippines

Period:

(since 1946)

Currency:

(1857—1967)

Demonetization: 2 January 1998

Total mintage: 390,000,000

Material

References

KM: #

Numista: #4475

Obverse

Reverse

Description:

Lady Liberty faces left, hammering an anvil with Mayon Volcano behind.

Inscription:

TEN CENTAVOS

1963

1963

Script: Latin

Designer: Melecio Figueroa

Edge

Reeded

Categories

| Symbol> Allegory |

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Royal Mint (Tower Hill) | — |

| United States Mint of Philadelphia | — |

| VDM Metals / Vereinigte Deutsche Metallwerke | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1958 | — | 10,000,000 | ||

| 1960 | — | 70,000,000 | ||

| 1962 | — | 50,000,000 | ||

| 1963 | — | 50,000,000 | ||

| 1964 | — | 100,000,000 | ||

| 1966 | — | 110,000,000 |

Historical background

In 1958, the Philippines operated under a managed currency system with the Philippine peso pegged to the United States dollar at a fixed rate of 2 pesos to 1 dollar. This exchange rate had been established in 1949 following the country's independence from the United States and was maintained through the Central Bank of the Philippines, which was created in 1949 to manage monetary policy. The economy was still heavily reliant on agricultural exports like sugar, coconut, and abaca, and the fixed peg provided stability for foreign trade and investment, which were crucial for post-war reconstruction and development.

However, this stability was under growing strain by the late 1950s. The country faced persistent balance of payments deficits, where the value of imports consistently exceeded export earnings, putting downward pressure on the peso's value. To defend the fixed peg, the government and the Central Bank relied on exchange and import controls, rationing scarce U.S. dollars for priority imports. This created a complex bureaucratic system that led to inefficiencies, occasional shortages of goods, and accusations of favoritism. Furthermore, a black market for dollars emerged where the peso traded at a significant discount, signaling a fundamental imbalance between the official rate and market reality.

The situation in 1958 was, therefore, one of mounting pressure on a system that was becoming increasingly difficult to sustain. While the fixed peg provided a facade of stability, the underlying economic weaknesses—trade imbalances, controlled forex, and a growing black market—were setting the stage for a major monetary crisis. Within a few years, these pressures would force the government to devalue the peso significantly, abandoning the 2:1 peg in the early 1960s and moving towards a more flexible, albeit still managed, exchange rate system to address the country's chronic dollar shortage.

However, this stability was under growing strain by the late 1950s. The country faced persistent balance of payments deficits, where the value of imports consistently exceeded export earnings, putting downward pressure on the peso's value. To defend the fixed peg, the government and the Central Bank relied on exchange and import controls, rationing scarce U.S. dollars for priority imports. This created a complex bureaucratic system that led to inefficiencies, occasional shortages of goods, and accusations of favoritism. Furthermore, a black market for dollars emerged where the peso traded at a significant discount, signaling a fundamental imbalance between the official rate and market reality.

The situation in 1958 was, therefore, one of mounting pressure on a system that was becoming increasingly difficult to sustain. While the fixed peg provided a facade of stability, the underlying economic weaknesses—trade imbalances, controlled forex, and a growing black market—were setting the stage for a major monetary crisis. Within a few years, these pressures would force the government to devalue the peso significantly, abandoning the 2:1 peg in the early 1960s and moving towards a more flexible, albeit still managed, exchange rate system to address the country's chronic dollar shortage.

Series: English Series

🌱 Very Common