10 dollars – Jamaica

Add to wishlist

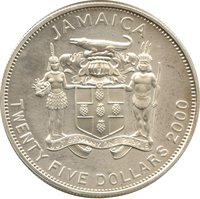

Jamaica

Context

Material

References

KM: #

Numista: #146988

Value

Exchange value: 10 JMD

Bullion value: $66.87

Obverse

Reverse

Edge

Mints

| Name | Mark |

|---|---|

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1999 | — | 500 | Proof |

Historical background

In 1999, Jamaica's currency situation was characterized by a managed floating exchange rate regime under significant pressure. The Jamaican dollar (JMD) had been on a long-term depreciating trend since the financial sector liberalization of the early 1990s, a period marked by a banking crisis that required a costly government bailout. This legacy of high public debt, exceeding 120% of GDP, and consistent current account deficits fueled persistent market anxiety about the currency's value. The Bank of Jamaica (BOJ) actively intervened in the foreign exchange market, using its limited reserves to smooth volatility and prevent a disorderly collapse, but it could not halt the gradual decline.

The core economic drivers of this pressure were stark. Inflation remained high (around 6-8% annually), eroding purchasing power and undermining confidence in the JMD. Simultaneously, interest rates were also high as the BOJ attempted to curb inflation and make holding Jamaican dollars more attractive, but this also stifled economic growth. The country was heavily reliant on imports for food and fuel, creating constant demand for US dollars, while key export sectors like bauxite and tourism, though important, did not earn enough foreign exchange to offset the outflow. This fundamental imbalance kept the currency vulnerable.

Consequently, 1999 ended with the Jamaican dollar continuing its slide, trading at approximately J$42 to US$1, a depreciation from about J$36 at the start of the year. This depreciation increased the local-currency cost of servicing the massive external debt and contributed to imported inflation, creating a challenging cycle for policymakers. The situation underscored the structural weaknesses in the Jamaican economy and set the stage for the continued economic hardships and focus on fiscal consolidation that would define the early 2000s.

The core economic drivers of this pressure were stark. Inflation remained high (around 6-8% annually), eroding purchasing power and undermining confidence in the JMD. Simultaneously, interest rates were also high as the BOJ attempted to curb inflation and make holding Jamaican dollars more attractive, but this also stifled economic growth. The country was heavily reliant on imports for food and fuel, creating constant demand for US dollars, while key export sectors like bauxite and tourism, though important, did not earn enough foreign exchange to offset the outflow. This fundamental imbalance kept the currency vulnerable.

Consequently, 1999 ended with the Jamaican dollar continuing its slide, trading at approximately J$42 to US$1, a depreciation from about J$36 at the start of the year. This depreciation increased the local-currency cost of servicing the massive external debt and contributed to imported inflation, creating a challenging cycle for policymakers. The situation underscored the structural weaknesses in the Jamaican economy and set the stage for the continued economic hardships and focus on fiscal consolidation that would define the early 2000s.

Series: Millennium

✨ Legendary