5 kroner (Norwegian Postal Service) – Norway

Add to wishlist

Circulating commemorative coins

Commemoration: 350th Anniversary of Norwegian Postal Service

Norway

Context

Material

Diameter: 29.5 mm

Weight: 11.5 g

Thickness: 2.23 mm

Shape: Round

Composition: Copper-nickel

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #14687

Value

Exchange value: 5 NOK

Inflation-adjusted value: 9.97 NOK

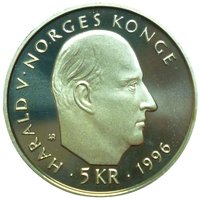

Obverse

Description:

Norwegian lion crowned, facing left with halberd. Inscription left, mintmark and initials right. Value by rear leg. Solid rim ring.

Inscription:

NORGE

⚒

JEJ

5 | KR

⚒

JEJ

5 | KR

Translation:

NORWAY

I AM

5 KRONER

I AM

5 KRONER

Script: Latin

Engraver: Ingrid Austlid Rise

Reverse

Description:

Postman on horseback facing left, blowing a horn. Inscription above; engraver's initials and date below. Solid ring on rim.

Inscription:

POSTEN SKAL FRAM

IAR

1647·1997

IAR

1647·1997

Translation:

The Mail Must Go Through

Year

1647·1997

Year

1647·1997

Script: Latin

Engraver: Ingrid Austlid Rise

Edge

Plain

Mints

| Name | Mark |

|---|---|

| Norwegian Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1997 | — | 12,000 | Proof | |

| 1997 | — | 1,667,073 | ||

| 1997 | — | 12,000 | BU |

Historical background

In 1997, Norway's currency situation was defined by its managed float exchange rate regime for the Norwegian krone (NOK). Following the collapse of the European Exchange Rate Mechanism (ERM) in the early 1990s, Norges Bank, the central bank, had adopted a policy of targeting low and stable inflation rather than a fixed exchange rate. However, it still actively monitored and occasionally intervened in the foreign exchange market to smooth out excessive volatility and maintain general stability for the krone. This approach reflected Norway's status as a major oil and gas exporter, where currency values were heavily influenced by fluctuating global energy prices and capital flows.

The economy was strong in 1997, buoyed by high oil prices and robust mainland (non-oil) economic growth. This strength, combined with relatively high interest rates compared to other European nations, attracted foreign capital and placed upward pressure on the krone. Norges Bank faced the classic "petrocurrency" dilemma: how to manage the inflationary and competitiveness risks of a strong currency without stifling domestic economic activity. The bank's focus was increasingly on its formal inflation target of 2.5%, which had been established in 1996, marking a gradual shift towards the transparency and rules-based monetary policy framework that would become more entrenched in the following years.

Looking ahead, 1997 was a calm before the storm. The Asian Financial Crisis, which began in mid-1997, initially had limited direct impact but would, by 1998, contribute to a sharp fall in global oil prices. This exposed the vulnerability of the krone to external commodity shocks. The pressures from this crisis would culminate in late 1998, forcing Norges Bank to abandon its managed float and allow the krone to depreciate significantly, a stark contrast to the relative stability it had maintained throughout most of 1997.

The economy was strong in 1997, buoyed by high oil prices and robust mainland (non-oil) economic growth. This strength, combined with relatively high interest rates compared to other European nations, attracted foreign capital and placed upward pressure on the krone. Norges Bank faced the classic "petrocurrency" dilemma: how to manage the inflationary and competitiveness risks of a strong currency without stifling domestic economic activity. The bank's focus was increasingly on its formal inflation target of 2.5%, which had been established in 1996, marking a gradual shift towards the transparency and rules-based monetary policy framework that would become more entrenched in the following years.

Looking ahead, 1997 was a calm before the storm. The Asian Financial Crisis, which began in mid-1997, initially had limited direct impact but would, by 1998, contribute to a sharp fall in global oil prices. This exposed the vulnerability of the krone to external commodity shocks. The pressures from this crisis would culminate in late 1998, forcing Norges Bank to abandon its managed float and allow the krone to depreciate significantly, a stark contrast to the relative stability it had maintained throughout most of 1997.

🌱 Common