5 kroner (Nansen's return from the Arctic) – Norway

Add to wishlist

Circulating commemorative coins

Commemoration: 100th Anniversary of Return of Nansen from the Arctic

Norway

Context

Material

Diameter: 29.5 mm

Weight: 11.5 g

Thickness: 2.23 mm

Shape: Round

Composition: Copper-nickel

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #14686

Value

Exchange value: 5 NOK

Inflation-adjusted value: 10.10 NOK

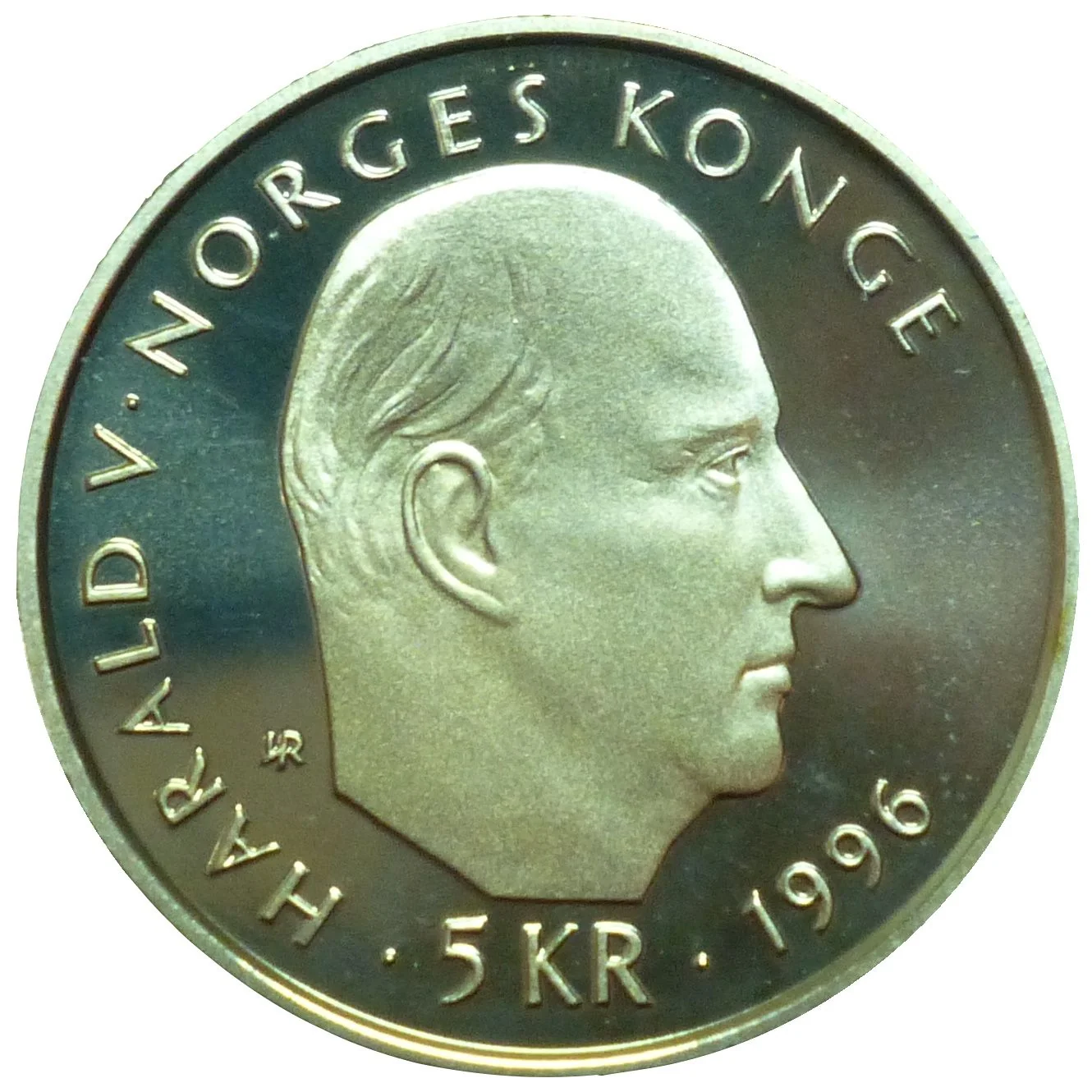

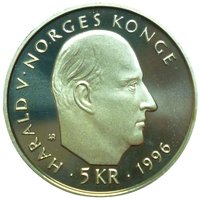

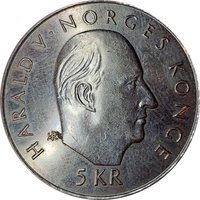

Obverse

Description:

Right-facing bust of King Harald V with engraver's initials behind it, surrounded by an inscription. Value and date below. Solid rim ring.

Inscription:

HARALD V · NORGES KONGE

IAR

· 5 KR · 1996

IAR

· 5 KR · 1996

Translation:

Harald V, Norway's King

IAR

5 Crowns 1996

IAR

5 Crowns 1996

Script: Latin

Engraver: Ingrid Austlid Rise

Reverse

Description:

The *Fram* locked in ice. Inscription top right. Expedition date and engraver's initials in the ice. Solid ring on rim.

Inscription:

FRAM OVER POLHAVET

1893·1896

IAR

1893·1896

IAR

Translation:

FRAM OVER THE POLAR SEA

1893·1896

YEAR

1893·1896

YEAR

Script: Latin

Engraver: Ingrid Austlid Rise

Edge

Smooth, inscribed with crossed hammers, the mark of the mint master J and waved lines.

Legend:

J

Categories

| Transportation> Watercraft |

Mints

| Name | Mark |

|---|---|

| Norwegian Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1996 | — | 1,291,909 | ||

| 1996 | — | 11,551 | Proof | |

| 1996 | — | 12,000 | BU |

Historical background

In 1996, Norway's currency situation was defined by its managed float exchange rate regime for the Norwegian krone (NOK). Following the collapse of the European Exchange Rate Mechanism (ERM) in 1992, Norges Bank, the central bank, had shifted from a fixed exchange rate policy to one where the krone's value was allowed to fluctuate within an unofficial, unpublished target band against a trade-weighted basket of currencies, though with a heavy emphasis on stability against European currencies, particularly the Deutsche Mark. The primary objective of monetary policy was explicitly to maintain a stable krone, with interest rates being the main tool to counteract undue volatility and speculative pressures.

The year was marked by significant economic strength, driven by rising petroleum revenues from the North Sea oil and gas sector. This created a complex policy dilemma: strong capital inflows and a growing current account surplus naturally put upward pressure on the krone. Norges Bank was therefore actively engaged in "leaning against the wind," using foreign exchange interventions and adjusting interest rates to prevent an excessive appreciation that would harm the competitiveness of Norway's non-oil export industries, such as shipping and manufacturing. Inflation was low and stable, but concerns about domestic overheating and asset price inflation were beginning to emerge.

This period laid the crucial groundwork for the major policy shift that would follow. The challenges of managing the krone amidst volatile capital flows and the "Dutch disease" effects of a resource-rich economy led to an intense domestic debate. By 1996, Norges Bank was increasingly advocating for a new framework that would prioritize an explicit inflation target over exchange rate stability. This culminated in 2001 with the formal adoption of an inflation-targeting regime, making the 1996 environment a pivotal final chapter in Norway's era of exchange rate-focused monetary policy.

The year was marked by significant economic strength, driven by rising petroleum revenues from the North Sea oil and gas sector. This created a complex policy dilemma: strong capital inflows and a growing current account surplus naturally put upward pressure on the krone. Norges Bank was therefore actively engaged in "leaning against the wind," using foreign exchange interventions and adjusting interest rates to prevent an excessive appreciation that would harm the competitiveness of Norway's non-oil export industries, such as shipping and manufacturing. Inflation was low and stable, but concerns about domestic overheating and asset price inflation were beginning to emerge.

This period laid the crucial groundwork for the major policy shift that would follow. The challenges of managing the krone amidst volatile capital flows and the "Dutch disease" effects of a resource-rich economy led to an intense domestic debate. By 1996, Norges Bank was increasingly advocating for a new framework that would prioritize an explicit inflation target over exchange rate stability. This culminated in 2001 with the formal adoption of an inflation-targeting regime, making the 1996 environment a pivotal final chapter in Norway's era of exchange rate-focused monetary policy.

🌱 Common