10 Dollars – Australia

Non-circulating coins

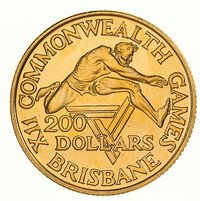

Commemoration: XII Commonwealth Games in Brisbane

Australia

Context

Material

References

KM: #Click to copy to clipboard75

Numista: #43855

Value

Exchange value: 10 AUD = $7.12

Bullion value: $52.59

Inflation-adjusted value: 48.13 AUD

Obverse

Description:

Queen Elizabeth II facing right in the Girls of Great Britain and Ireland Tiara.

Inscription:

ELIZABETH II

AUSTRALIA 1982

AUSTRALIA 1982

Script: Latin

Designer: Arnold Machin

Reverse

Description:

Country outline with Games Logo, encircled by icons of 12 sports, surrounded by an outer legend ring.

Inscription:

XII COMMONWEALTH GAMES BRISBANE

: 10 DOLLARS :

: 10 DOLLARS :

Script: Latin

Designers: Stuart Devlin, Hugh Edwards

Edge

Milled

Categories

| Sport> Commonwealth Games |

| Sport> Athletics |

| Sport> Boxing or wrestling |

| Sport> Cycling |

| Sport> Swimming |

| Sport> Table tennis |

Mints

| Name | Mark |

|---|---|

| Royal Australian Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1982 | — | 125,700 | BU | |

| 1982 | — | 75,094 | Proof |

Historical background

In 1982, Australia's currency situation was defined by a pivotal transition away from a fixed exchange rate regime. Just over a decade earlier, in 1971, the Australian dollar (AUD) had been pegged to the US dollar, but this was abandoned in 1974 in favour of a peg against a trade-weighted basket of currencies. By the early 1980s, this system was under severe strain. High inflation, persistent current account deficits, and volatile capital flows, exacerbated by global oil shocks and a worldwide recession, created intense pressure on the managed peg. The Reserve Bank of Australia was forced to engage in frequent and costly interventions to defend the currency's value, devaluing it several times within the basket peg system.

The year itself was marked by significant turbulence and a major policy shift. In May 1982, the AUD was devalued by 10% as part of a broader incomes and economic policy package. However, the fundamental pressures remained, leading to a more profound change in December 1983. Although this occurred just after the 1982 timeframe, it was the direct culmination of that year's instability: the newly elected Hawke Labor government, with Treasurer Paul Keating, floated the Australian dollar. This decision freed the currency's value to be determined by market forces, a move that was considered radical at the time but ultimately modernised Australia's financial system.

Therefore, the background for 1982 is best understood as the final chapter of a failing fixed exchange rate system. The currency was caught between domestic economic challenges—including wage pressures and high inflation—and a volatile international environment. The frequent devaluations and defensive interventions of that year highlighted the system's unsustainability, setting the stage for the historic float in late 1983, which fundamentally reshaped Australia's economic policy and insulated it better from future external shocks.

The year itself was marked by significant turbulence and a major policy shift. In May 1982, the AUD was devalued by 10% as part of a broader incomes and economic policy package. However, the fundamental pressures remained, leading to a more profound change in December 1983. Although this occurred just after the 1982 timeframe, it was the direct culmination of that year's instability: the newly elected Hawke Labor government, with Treasurer Paul Keating, floated the Australian dollar. This decision freed the currency's value to be determined by market forces, a move that was considered radical at the time but ultimately modernised Australia's financial system.

Therefore, the background for 1982 is best understood as the final chapter of a failing fixed exchange rate system. The currency was caught between domestic economic challenges—including wage pressures and high inflation—and a volatile international environment. The frequent devaluations and defensive interventions of that year highlighted the system's unsustainability, setting the stage for the historic float in late 1983, which fundamentally reshaped Australia's economic policy and insulated it better from future external shocks.

🌟 Limited