2½ gulden – Netherlands

Add to wishlist

Netherlands

Context

Year: 1840

Issuer: Netherlands

Ruler: William I

Currency:

(1817—2001)

Demonetized: Yes

Total mintage: 44,376

Material

References

KM: #

Numista: #43773

Value

Exchange value: 2.5 NLG

Bullion value: $59.30

Obverse

Description:

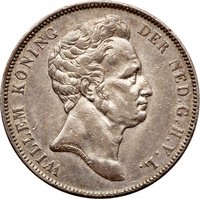

King Willem head, right profile

Inscription:

WILLEM KONING DER NED G. H. V. L.

I. P. SCHOUBERG F.

I. P. SCHOUBERG F.

Translation:

Willem King of the Netherlands Grand Duke of Luxembourg

J. P. Schouberg made this

J. P. Schouberg made this

Script: Latin

Engraver: Johannes Petrus Schouberg

Reverse

Edge

Categories

| Symbol> Crown |

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Royal Dutch Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1840 | — | 44,376 | ||

| 1840 | — | — | Proof |

Historical background

In 1840, the Netherlands operated under a bimetallic monetary system, legally defined by the Money Act of 1816 (Muntwet). This system established both silver and gold as legal tender, with their values fixed in relation to the guilder (or gulden). The primary coin was the silver guilder, but gold coins, such as the ten-guilder piece, were also minted. However, the fixed legal ratio between silver and gold did not always align with fluctuating market prices, leading to practical challenges where one metal would often be undervalued and subsequently exported, causing a shortage.

The period leading up to 1840 was one of financial strain and transition. The costly Belgian Revolution (1830-1839) and the subsequent separation of Belgium had heavily drained the Dutch treasury, leading to significant state debt. Furthermore, the global economic climate was affecting the money supply. A notable phenomenon was the influx of silver from the Dutch East Indies (modern-day Indonesia), which began to increase the silver supply relative to gold, subtly undermining the bimetallic equilibrium. This contributed to a de facto silver standard, where silver became the principal basis for the currency in everyday use.

Consequently, by 1840, the currency system was stable in law but faced underlying pressures. The government maintained the official bimetallic standard, but in practice, the circulation of full-value silver coins was paramount. The financial burdens of the previous decade had also spurred discussions about banking and monetary reform, which would eventually lead to the establishment of the Dutch Bank (De Nederlandsche Bank) as a central bank with exclusive note-issuing rights in 1814, though its full modernizing influence on the currency was still developing. Thus, the situation was one of a formally sound system grappling with the practical realities of post-war finance and shifting bullion markets.

The period leading up to 1840 was one of financial strain and transition. The costly Belgian Revolution (1830-1839) and the subsequent separation of Belgium had heavily drained the Dutch treasury, leading to significant state debt. Furthermore, the global economic climate was affecting the money supply. A notable phenomenon was the influx of silver from the Dutch East Indies (modern-day Indonesia), which began to increase the silver supply relative to gold, subtly undermining the bimetallic equilibrium. This contributed to a de facto silver standard, where silver became the principal basis for the currency in everyday use.

Consequently, by 1840, the currency system was stable in law but faced underlying pressures. The government maintained the official bimetallic standard, but in practice, the circulation of full-value silver coins was paramount. The financial burdens of the previous decade had also spurred discussions about banking and monetary reform, which would eventually lead to the establishment of the Dutch Bank (De Nederlandsche Bank) as a central bank with exclusive note-issuing rights in 1814, though its full modernizing influence on the currency was still developing. Thus, the situation was one of a formally sound system grappling with the practical realities of post-war finance and shifting bullion markets.

⭐ Rare