2500 dollars – Canada

Add to wishlist

Non-circulating coins

Series: Robert Bateman

Canada

Context

Material

Diameter: 101.6 mm

Weight: 1006.1 g

Gold Weight:: 1006.00 g

Shape: Round

Composition: 99.99% Gold

Standard: Silver kilo

Magnetic: No

Alignment: Medal alignment

flip

References

KM: #

Numista: #437634

Value

Exchange value: 2500 CAD

Bullion value: $153370.15

Inflation-adjusted value: 2574.60 CAD

Obverse

Description:

The obverse shows Queen Elizabeth II at age 77, facing right, wearing a necklace and earrings. It includes the dates "1952" and "2022," separated by four pearls representing her four Canadian coin effigies.

Inscription:

ELIZABETH II D•G•REGINA

1952 ⁘ 2022

SB

1952 ⁘ 2022

SB

Translation:

Elizabeth II by the Grace of God, Queen

1952 - 2022

SB

1952 - 2022

SB

Script: Latin

Designer: Susanna Blunt

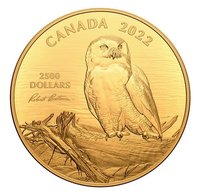

Reverse

Description:

The reverse features Robert Bateman's "Weather Watch – Bison," depicting a bison alertly resting on a grassy bank.

Inscription:

CANADA 2024

2500

DOLLARS

Robert Bateman

2500

DOLLARS

Robert Bateman

Script: Latin

Designer: Robert Bateman

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Royal Canadian Mint of Ottawa | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2024 | — | 70 | Proof |

Historical background

In 2024, Canada's currency situation is defined by a persistent battle with inflation and the resulting high-interest rate environment set by the Bank of Canada. After hitting a multi-decade high in 2022, inflation has cooled but remains stubbornly above the central bank's 2% target, driven by core pressures from services, housing costs, and wage growth. This has forced the Bank of Canada to maintain its benchmark interest rate at a 22-year high of 5% for an extended period, creating a cautious stalemate as it seeks clearer, sustained evidence that inflationary pressures are fully subdued before considering cuts.

The Canadian dollar (CAD) has consequently traded in a relatively narrow range, primarily influenced by the differential between Canadian and U.S. monetary policy. The "loonie" has shown resilience but faces headwinds, often weakening when market expectations pivot toward earlier or deeper rate cuts by the Bank of Canada compared to the U.S. Federal Reserve. Its value is also sensitive to global commodity prices, particularly oil, though this traditional support has been inconsistent amid fluctuating global demand and geopolitical tensions.

Looking forward, the key domestic narrative is the timing and pace of the anticipated easing cycle. Households and businesses are grappling with the high cost of borrowing, which is dampening economic growth and increasing debt servicing burdens. The central bank faces a delicate balancing act: cutting rates too soon could re-ignite inflation, while acting too late could unnecessarily deepen an economic slowdown. The currency's trajectory for the remainder of 2024 will hinge almost entirely on this pivot, alongside external factors like the strength of the U.S. economy and global risk sentiment.

The Canadian dollar (CAD) has consequently traded in a relatively narrow range, primarily influenced by the differential between Canadian and U.S. monetary policy. The "loonie" has shown resilience but faces headwinds, often weakening when market expectations pivot toward earlier or deeper rate cuts by the Bank of Canada compared to the U.S. Federal Reserve. Its value is also sensitive to global commodity prices, particularly oil, though this traditional support has been inconsistent amid fluctuating global demand and geopolitical tensions.

Looking forward, the key domestic narrative is the timing and pace of the anticipated easing cycle. Households and businesses are grappling with the high cost of borrowing, which is dampening economic growth and increasing debt servicing burdens. The central bank faces a delicate balancing act: cutting rates too soon could re-ignite inflation, while acting too late could unnecessarily deepen an economic slowdown. The currency's trajectory for the remainder of 2024 will hinge almost entirely on this pivot, alongside external factors like the strength of the U.S. economy and global risk sentiment.

Series: Robert Bateman

✨ Legendary