2 dollars – Fiji

Add to wishlist

Non-circulating coins

Series: Dogs

Fiji

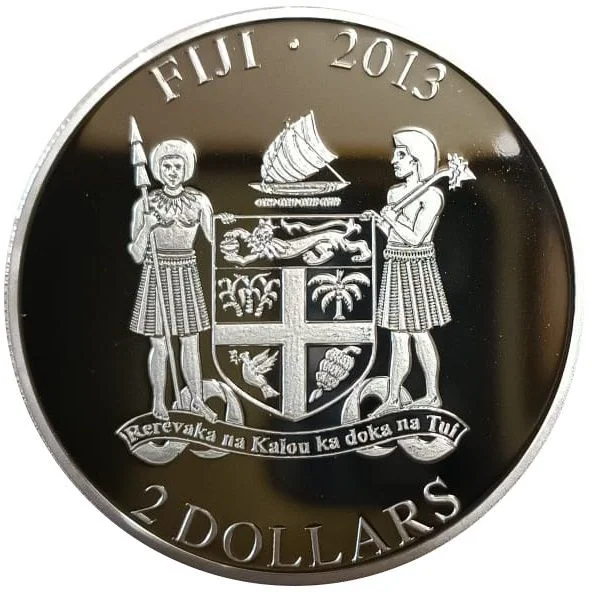

Obverse

Description:

Coat of arms centered, with country, date, and value below.

Inscription:

FIJI 2013

Rerevaka na Kalou ka doka na Tui

2 DOLLARS

Rerevaka na Kalou ka doka na Tui

2 DOLLARS

Translation:

Fear God and honor the King

2 Dollars

2 Dollars

Script: Latin

Designer: Podrojkin Sergey

Reverse

Inscription:

MY LITTLE PUPPY

POMERANIAN

POMERANIAN

Script: Latin

Edge

Reeded

Categories

| Animal> Dog |

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| JVP mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2013 | — | 5,000 | Proof |

Historical background

In 2013, Fiji's currency situation was characterized by a period of relative stability and deliberate management under the Reserve Bank of Fiji (RBF), following a period of significant volatility. The Fijian dollar (FJD) had weathered a major devaluation of 20% in 2009, a move intended to boost export competitiveness and tourism in the wake of the global financial crisis and domestic political upheaval. By 2013, the RBF's policy focus had shifted to maintaining stability, with the dollar operating under a managed float. The central bank actively intervened in the foreign exchange market to curb excessive volatility and maintain adequate foreign reserves, which were crucial for a small, import-dependent island nation.

The key monetary policy objective for the year, as outlined by the RBF, was to keep inflation low and stable. This was largely successful, with inflation averaging around 3% for much of the year, down from higher rates in the preceding years. This stability was supported by a combination of prudent monetary policy, which kept the Overnight Policy Rate (OPR) at a historically low 0.5% to stimulate economic activity, and relatively stable global commodity prices. The low interest rate environment was designed to encourage borrowing and investment as the country continued its post-coup and post-crisis economic recovery.

Underpinning this stability was a healthy level of foreign reserves, which remained comfortably above the RBF's benchmark of four months of import cover throughout 2013. Strong performances in the tourism and remittance sectors provided consistent inflows of foreign currency, bolstering the reserves. Consequently, the Fijian dollar exhibited minimal fluctuation against major trading partner currencies like the Australian and New Zealand dollars, trading within a narrow band. This managed stability provided a predictable economic platform for businesses and supported the government's broader goals of fostering investment and growth.

The key monetary policy objective for the year, as outlined by the RBF, was to keep inflation low and stable. This was largely successful, with inflation averaging around 3% for much of the year, down from higher rates in the preceding years. This stability was supported by a combination of prudent monetary policy, which kept the Overnight Policy Rate (OPR) at a historically low 0.5% to stimulate economic activity, and relatively stable global commodity prices. The low interest rate environment was designed to encourage borrowing and investment as the country continued its post-coup and post-crisis economic recovery.

Underpinning this stability was a healthy level of foreign reserves, which remained comfortably above the RBF's benchmark of four months of import cover throughout 2013. Strong performances in the tourism and remittance sectors provided consistent inflows of foreign currency, bolstering the reserves. Consequently, the Fijian dollar exhibited minimal fluctuation against major trading partner currencies like the Australian and New Zealand dollars, trading within a narrow band. This managed stability provided a predictable economic platform for businesses and supported the government's broader goals of fostering investment and growth.

Series: Dogs

✨ Legendary