100 Dollars – Australia

Australia

Context

Years: 1988–1989

Issuer: Australia

Ruler: Elizabeth II

Currency:

(since 1966)

Total mintage: 140,725

Material

Diameter: 32.1 mm

Weight: 31.14 g

Platinum weight: 31.12 g

Thickness: 2.7 mm

Shape: Round

Composition: 99.95% Platinum

Standard: Silver ounce

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #Click to copy to clipboard111

Numista: #41347

Value

Exchange value: 100 AUD = $71.20

Bullion value: $0.00

Inflation-adjusted value: 299.80 AUD

Obverse

Description:

Queen Elizabeth III facing right in the King George IV State Diadem.

Inscription:

ELIZABETH II

AUSTRALIA

100 DOLLARS

RDM

AUSTRALIA

100 DOLLARS

RDM

Script: Latin

Designer: Raphael David Maklouf

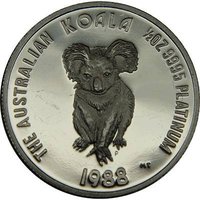

Reverse

Description:

Seated koala facing forward, date beneath.

Inscription:

THE AUSTRALIAN KOALA

1 OZ 9995 PLATINUM

1988 MT

1 OZ 9995 PLATINUM

1988 MT

Script: Latin

Designer: Michael Tracey

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Perth Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1988 | — | 61,682 | BU | |

| 1989 | — | 79,043 | BU |

Historical background

In 1988, Australia's currency situation was characterised by a managed float of the Australian dollar (AUD) operating within a broader context of economic liberalisation and external pressures. Just three years prior, in December 1983, the Hawke-Keating Labor government had deregulated the financial system and floated the dollar, abandoning a fixed exchange rate. By 1988, the currency was therefore valued by market forces of supply and demand, with the Reserve Bank of Australia (RBA) intervening only to smooth out excessive volatility or address disorderly market conditions. This new regime was still being tested, with the dollar's value heavily influenced by commodity prices, particularly for key exports like coal and wool, and shifting interest rate differentials with major trading partners.

The year saw the AUD under significant downward pressure, depreciating notably against the US dollar and other major currencies. This weakness was driven by a widening current account deficit, which ballooned to around 4% of GDP, and a high level of foreign debt accumulated during the 1980s. Market sentiment was concerned about Australia's "twin deficits" (both fiscal and current account), leading to periodic sell-offs of the currency. In response, the RBA maintained a tight monetary policy, with high interest rates throughout 1988 (the cash rate reached 15.5% in early 1989) to curb inflationary pressures from strong domestic demand and to support the currency by attracting foreign capital.

Overall, the currency situation in 1988 reflected a challenging transition for an economy opening itself to global financial markets. The floating dollar acted as a shock absorber, but its depreciation highlighted underlying structural issues and exposed the economy to the discipline of international investors. This environment set the stage for the "recession we had to have" in the early 1990s, as policymakers continued to grapple with balancing external imbalances, inflation, and growth in the new financial landscape they had created.

The year saw the AUD under significant downward pressure, depreciating notably against the US dollar and other major currencies. This weakness was driven by a widening current account deficit, which ballooned to around 4% of GDP, and a high level of foreign debt accumulated during the 1980s. Market sentiment was concerned about Australia's "twin deficits" (both fiscal and current account), leading to periodic sell-offs of the currency. In response, the RBA maintained a tight monetary policy, with high interest rates throughout 1988 (the cash rate reached 15.5% in early 1989) to curb inflationary pressures from strong domestic demand and to support the currency by attracting foreign capital.

Overall, the currency situation in 1988 reflected a challenging transition for an economy opening itself to global financial markets. The floating dollar acted as a shock absorber, but its depreciation highlighted underlying structural issues and exposed the economy to the discipline of international investors. This environment set the stage for the "recession we had to have" in the early 1990s, as policymakers continued to grapple with balancing external imbalances, inflation, and growth in the new financial landscape they had created.

Series: Platinum Issues

💎 Extremely Rare