100 zlotys (Poland Regaining Independence) – Poland

Add to wishlist

Non-circulating coins

Commemoration: 100th Anniversary of Regaining Independence by Poland

Poland

Context

Material

Weight: 217.7 g

Silver Weight:: 217.48 g

Shape: Sculptural

Composition: 99.9% Silver

Magnetic: No

Technique: Milled

Alignment: Medal alignment

flip

References

Y: #

Numista: #144544

Value

Exchange value: 100 PLN

Bullion value: $551.39

Inflation-adjusted value: 153.45 PLN

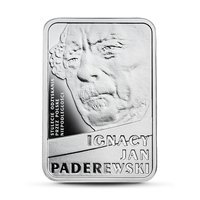

Obverse

Inscription:

RZECZPOSPOLITA POLSKA 2018 •

mw

mw

Translation:

REPUBLIC OF POLAND 2018 •

Script: Latin

Language: Polish

Designer: Urszula Walerzak

Reverse

Inscription:

100

ZŁ

100. ROCZNICA ODZYSKANIA PRZEZ POLSKĘ NIEPODLEGŁOŚCI •

ZŁ

100. ROCZNICA ODZYSKANIA PRZEZ POLSKĘ NIEPODLEGŁOŚCI •

Translation:

100 ZŁ

100th Anniversary of Poland Regaining Independence •

100th Anniversary of Poland Regaining Independence •

Script: Latin

Language: Polish

Designer: Urszula Walerzak

Edge

Lettering

Legend:

JESZCZE POLSKA NIE ZGINĘŁA, KIEDY MY ŻYJEMY

Translation:

Poland has not yet perished, so long as we still live.

Language: Polish

Categories

| Event> Independence |

Mints

| Name | Mark |

|---|---|

| Mint of Poland | (MW) |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2018 | MW | 1,918 | Proof |

Historical background

In 2018, Poland's currency, the złoty (PLN), operated within a context of robust economic growth but heightened regional political uncertainty. The Polish economy was strong, with GDP growth exceeding 5%, low unemployment, and rising wages, which typically supports a currency. However, the złoty faced persistent headwinds primarily from external factors. The most significant was the strengthening of the US dollar globally, which pressured all emerging market currencies, and concerns over the economic policies and rule-of-law disputes between Poland's governing Law and Justice (PiS) party and the European Commission. These tensions raised perceived political risk, occasionally spooking investors.

The National Bank of Poland (NBP) maintained a historically low reference interest rate of 1.5% throughout the year, a policy stance that limited the złoty's appeal to yield-seeking investors. While inflation remained within the bank's target range, the low-rate environment contrasted with the tightening monetary policy in the United States, contributing to the złoty's weakness against the dollar. Throughout 2018, the USD/PLN exchange rate climbed from approximately 3.45 in January to nearly 3.82 by year's end, marking a significant depreciation of over 10% for the złoty against the greenback.

Despite this depreciation, the situation was not seen as a crisis. The weak złoty actually benefited Polish exporters, boosting the competitiveness of the country's substantial manufacturing sector. Furthermore, the currency's movement was broadly in line with its regional peers like the Hungarian forint and Czech koruna, which faced similar pressures. The NBP signaled comfort with the currency's level, viewing it as a natural adjustment to external shocks rather than a fundamental imbalance, and did not intervene directly to strengthen the złoty, prioritizing domestic economic stability instead.

The National Bank of Poland (NBP) maintained a historically low reference interest rate of 1.5% throughout the year, a policy stance that limited the złoty's appeal to yield-seeking investors. While inflation remained within the bank's target range, the low-rate environment contrasted with the tightening monetary policy in the United States, contributing to the złoty's weakness against the dollar. Throughout 2018, the USD/PLN exchange rate climbed from approximately 3.45 in January to nearly 3.82 by year's end, marking a significant depreciation of over 10% for the złoty against the greenback.

Despite this depreciation, the situation was not seen as a crisis. The weak złoty actually benefited Polish exporters, boosting the competitiveness of the country's substantial manufacturing sector. Furthermore, the currency's movement was broadly in line with its regional peers like the Hungarian forint and Czech koruna, which faced similar pressures. The NBP signaled comfort with the currency's level, viewing it as a natural adjustment to external shocks rather than a fundamental imbalance, and did not intervene directly to strengthen the złoty, prioritizing domestic economic stability instead.

✨ Legendary