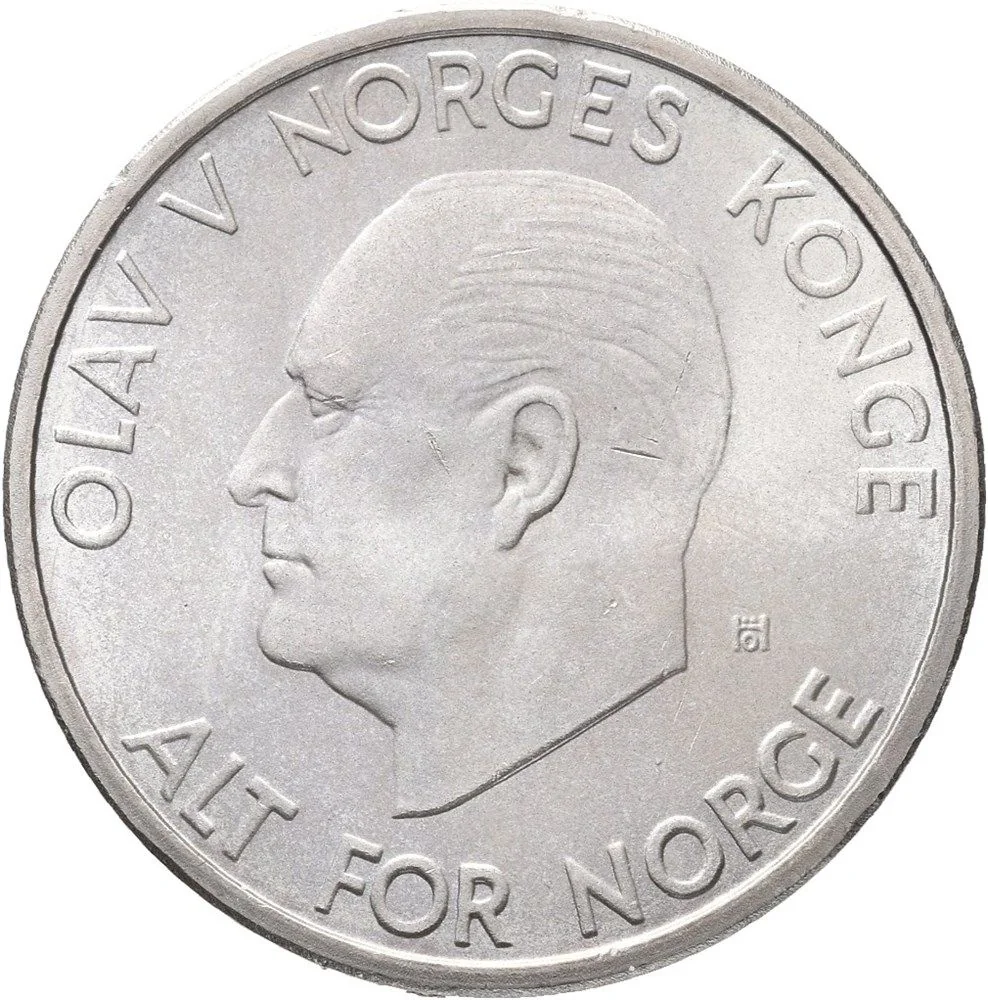

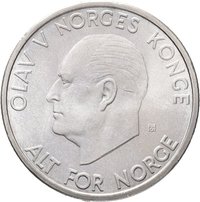

Obverse

Description:

King Olav V bust facing left. Engraver's initials behind bust. Inscription surrounds. Solid rim ring.

Inscription:

OLAV V NORGES KONGE

öH

ALT FOR NORGE

öH

ALT FOR NORGE

Translation:

Olav V Norway's King

By the Grace of God

All for Norway

By the Grace of God

All for Norway

Script: Latin

Engraver: Øivind Hansen

Reverse

Description:

Crowned shield with a lion holding a halberd left. Value and date flank shield. Solid rim ring.

Inscription:

5 | KR

19 | 66

19 | 66

Script: Latin

Engraver: Øivind Hansen

Edge

Plain with wavy line, alternating with crossed hammers mintmark and letter B.

Legend:

B

Mints

| Name | Mark |

|---|---|

| Norwegian Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1963 | — | 7,074,000 | ||

| 1964 | — | 7,346,000 | ||

| 1965 | — | 2,231,200 | ||

| 1966 | — | 2,500,600 | ||

| 1967 | — | 580,600 | ||

| 1968 | — | 1,810,000 | ||

| 1969 | — | 2,393,200 | ||

| 1970 | — | — | Proof | |

| 1970 | — | 193,000 | ||

| 1971 | — | 171,900 | ||

| 1972 | — | 2,267,720 | ||

| 1973 | — | 2,757,880 |

Historical background

In 1963, Norway’s currency was governed by the Bretton Woods system, which pegged the Norwegian krone (NOK) to the US dollar at a fixed but adjustable rate. This arrangement, managed by the central bank (Norges Bank), provided stability for the small, open economy, which was heavily reliant on foreign trade. However, the system also imposed constraints, requiring Norway to maintain sufficient foreign exchange reserves to defend the peg and limiting the use of independent monetary policy to address domestic economic conditions.

Domestically, the year fell within a prolonged period of post-war reconstruction and rapid industrialization, known as the "regulated economy." The government exercised significant control over credit and capital flows to support its policy goals of full employment and industrial development. While the krone's fixed exchange rate facilitated predictable trade and investment, it sometimes conflicted with these domestic priorities, particularly as inflationary pressures began to build. The economy was transitioning, with the foundations of the future oil era not yet discovered, leaving shipping and traditional manufacturing as key export sectors.

Internationally, the Bretton Woods system itself was showing signs of strain, though the major crises of the late 1960s were still ahead. For Norway in 1963, the currency situation was thus one of relative stability under a managed regime, but with underlying tensions between the discipline of a fixed exchange rate and the ambitions of an activist state pursuing full employment and growth. This delicate balance would be challenged in the coming years as global monetary instability grew and, eventually, as Norway’s own economic structure was transformed by North Sea oil.

Domestically, the year fell within a prolonged period of post-war reconstruction and rapid industrialization, known as the "regulated economy." The government exercised significant control over credit and capital flows to support its policy goals of full employment and industrial development. While the krone's fixed exchange rate facilitated predictable trade and investment, it sometimes conflicted with these domestic priorities, particularly as inflationary pressures began to build. The economy was transitioning, with the foundations of the future oil era not yet discovered, leaving shipping and traditional manufacturing as key export sectors.

Internationally, the Bretton Woods system itself was showing signs of strain, though the major crises of the late 1960s were still ahead. For Norway in 1963, the currency situation was thus one of relative stability under a managed regime, but with underlying tensions between the discipline of a fixed exchange rate and the ambitions of an activist state pursuing full employment and growth. This delicate balance would be challenged in the coming years as global monetary instability grew and, eventually, as Norway’s own economic structure was transformed by North Sea oil.

🌱 Very Common