10 Bahts (Ministry of Transportation) – Thailand

Circulating commemorative coins

Commemoration: 100th Anniversary of the Ministry of Transportation

Thailand

Context

Year: 2012

Thai Year: 2555

Issuer: Thailand

Ruler: Bhumibol Adulyadej

Currency:

(since 1897)

Demonetized: Yes

Total mintage: 1,000,000

References

Y: #Click to copy to clipboard525

Numista: #41085

Value

Exchange value: 10 THB = $0.32

Obverse

Description:

Portrait of Rama VI encircled by his royal title.

Inscription:

พระบาทสมเด็จพระปรเมนทรมหาวชิราวุธ พระมงกุฏเกล้าเจ้าอยู่หัว

รัชกาลที่ ๖

รัชกาลที่ ๖

Translation:

His Majesty King Vajiravudh, the royal adornment of the head, the King.

The Sixth Reign.

The Sixth Reign.

Language: Thai

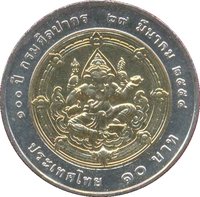

Reverse

Description:

Two soldiers on a tank, with text: "100th Anniversary of the Ministry of Transport, April 1, 2555. 10 Baht, Thailand."

Inscription:

ครบ ๑๐๐ ปี กระทรวงคมนาคม ๑ เมษายน ๒๕๕๕

๑๐ บาท ประเทศไทย

๑๐ บาท ประเทศไทย

Translation:

One Hundredth Anniversary of the Ministry of Transport, 1 April 2012

Ten Baht, Thailand

Ten Baht, Thailand

Language: Thai

Edge

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2012 | — | 1,000,000 |

Historical background

In 2012, Thailand's currency, the baht (THB), was characterized by significant strength and volatility, largely driven by global macroeconomic forces. As a major emerging economy, Thailand attracted substantial foreign capital inflows seeking higher yields, especially as developed nations like the United States and the Eurozone maintained ultra-low interest rates following the 2008 financial crisis. This influx of "hot money" into Thai stocks and bonds placed persistent upward pressure on the baht, raising concerns among exporters about eroded international competitiveness for key sectors like electronics, automobiles, and rice.

The government, led by Prime Minister Yingluck Shinawatra, and the Bank of Thailand (BOT) faced a complex policy dilemma. While a strong baht helped contain inflation and lowered the cost of imports, authorities were wary of its negative impact on the crucial export sector, which accounted for over 60% of GDP. In response, the BOT implemented a series of measures, including interest rate cuts and direct intervention in foreign exchange markets to slow the baht's appreciation. These actions, however, drew criticism and scrutiny from abroad, with the United States briefly placing Thailand on its "Monitoring List" for currency practices in late 2012.

Ultimately, the currency situation reflected Thailand's vulnerability to external financial currents. The strong baht was a symptom of its relative economic success and stability in the region, yet it also highlighted the challenges of managing an open economy during a period of unprecedented global monetary easing. The tensions between supporting growth through exports and maintaining financial stability set the stage for ongoing policy debates regarding capital controls and macroprudential measures in the years that followed.

The government, led by Prime Minister Yingluck Shinawatra, and the Bank of Thailand (BOT) faced a complex policy dilemma. While a strong baht helped contain inflation and lowered the cost of imports, authorities were wary of its negative impact on the crucial export sector, which accounted for over 60% of GDP. In response, the BOT implemented a series of measures, including interest rate cuts and direct intervention in foreign exchange markets to slow the baht's appreciation. These actions, however, drew criticism and scrutiny from abroad, with the United States briefly placing Thailand on its "Monitoring List" for currency practices in late 2012.

Ultimately, the currency situation reflected Thailand's vulnerability to external financial currents. The strong baht was a symptom of its relative economic success and stability in the region, yet it also highlighted the challenges of managing an open economy during a period of unprecedented global monetary easing. The tensions between supporting growth through exports and maintaining financial stability set the stage for ongoing policy debates regarding capital controls and macroprudential measures in the years that followed.

🌱 Fairly Common