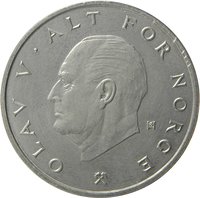

Obverse

Description:

Shield with crowned lion holding a halberd left. Date flanking shield. Solid rim ring.

Inscription:

19 | 84

Script: Latin

Engraver: Øivind Hansen

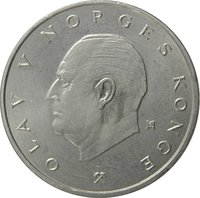

Reverse

Description:

Three-line inscription. Mintmaster initial left, engraver initial right on second line. Mintmark below. Solid rim ring.

Inscription:

50

K ØRE ØH

NORGE

⚒

K ØRE ØH

NORGE

⚒

Translation:

50 Øre

Norway

Pickaxe

Norway

Pickaxe

Script: Latin

Language: Norwegian

Engraver: Øivind Hansen

Edge

Reeded

Categories

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Norwegian Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1974 | — | 8,454,253 | ||

| 1975 | — | 10,088,002 | ||

| 1976 | — | 15,147,324 | ||

| 1977 | — | 19,381,750 | ||

| 1978 | — | 15,270,000 | ||

| 1979 | — | 10,094,000 | ||

| 1980 | — | 6,986,000 | ||

| 1981 | — | 3,302,000 | ||

| 1982 | — | 11,054,000 | ||

| 1983 | — | 15,660,000 | ||

| 1984 | — | 8,514,000 | ||

| 1985 | — | 4,334,000 | ||

| 1986 | — | 4,078,000 | ||

| 1987 | — | 5,082,000 | ||

| 1988 | — | 9,508,000 | ||

| 1989 | — | 5,684,000 | ||

| 1990 | — | 1,626,000 | ||

| 1991 | — | 2,824,000 | ||

| 1992 | — | 6,702,000 | ||

| 1992 | — | 20,000 | Proof | |

| 1993 | — | 7,956,000 | ||

| 1993 | — | 12,000 | Proof | |

| 1994 | — | 7,073,000 | ||

| 1994 | — | 15,000 | Proof | |

| 1995 | — | 14,459 | Proof | |

| 1995 | — | 6,735,000 | ||

| 1996 | — | 4,410,000 | ||

| 1996 | — | 11,551 | Proof |

Historical background

In 1974, Norway's currency situation was defined by its participation in the European "snake in the tunnel" exchange rate mechanism, a collective effort to limit fluctuations between European currencies following the collapse of the Bretton Woods system. Norway, not yet an EEC member, had joined this arrangement in 1972 as an associate member, pegging the Norwegian krone (NOK) to a basket of currencies, effectively shadowing the Deutsche Mark. This policy aimed to provide stability for its vital export-oriented industries, particularly shipping and traditional manufacturing, by reducing exchange rate uncertainty with its major trading partners in Europe.

However, this commitment created significant domestic tension. Norway was experiencing the early effects of its nascent oil wealth, which began flowing from the Ekofisk field in 1971. This new economic reality led to inflationary pressures, a growing current account surplus, and differing economic cycles from its European partners. Maintaining the fixed peg required the Norges Bank to intervene heavily in foreign exchange markets, buying foreign currency to prevent the krone from appreciating too strongly. This conflict—between the needs of a traditional industrial economy seeking stable exchange rates and the emerging oil economy generating immense capital inflows—placed the fixed exchange rate regime under considerable strain.

Ultimately, the pressures proved unsustainable. In December 1974, after repeated interventions and facing divergent monetary policies, Norway was forced to withdraw from the "snake." The krone was revalued by 5% and pegged to a trade-weighted currency basket, marking a pivotal shift. This move acknowledged that Norway's economic destiny was becoming decoupled from continental Europe due to oil, setting the stage for the independent, managed float and oil fund model that would define its future macroeconomic policy.

However, this commitment created significant domestic tension. Norway was experiencing the early effects of its nascent oil wealth, which began flowing from the Ekofisk field in 1971. This new economic reality led to inflationary pressures, a growing current account surplus, and differing economic cycles from its European partners. Maintaining the fixed peg required the Norges Bank to intervene heavily in foreign exchange markets, buying foreign currency to prevent the krone from appreciating too strongly. This conflict—between the needs of a traditional industrial economy seeking stable exchange rates and the emerging oil economy generating immense capital inflows—placed the fixed exchange rate regime under considerable strain.

Ultimately, the pressures proved unsustainable. In December 1974, after repeated interventions and facing divergent monetary policies, Norway was forced to withdraw from the "snake." The krone was revalued by 5% and pegged to a trade-weighted currency basket, marking a pivotal shift. This move acknowledged that Norway's economic destiny was becoming decoupled from continental Europe due to oil, setting the stage for the independent, managed float and oil fund model that would define its future macroeconomic policy.

Series: 1974 Norway circulation coins

🌱 Very Common