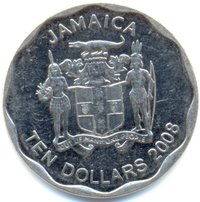

10 Dollars – Jamaica

Jamaica

Context

Material

References

KM: #Click to copy to clipboard190

Numista: #14370

Value

Exchange value: 10 JMD

Obverse

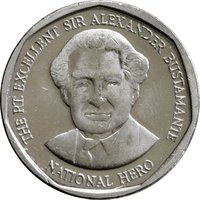

Reverse

Description:

Bust of George William Gordon, frontal.

Inscription:

THE RT. EXCELLENT GEORGE WILLIAM GORDON

NATIONAL HERO

NATIONAL HERO

Script: Latin

Edge

Plain

Categories

| Symbols> Coat of Arms |

| Person> Politician |

Mints

| Name | Mark |

|---|---|

| Royal Dutch Mint | — |

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2008 | — | — | ||

| 2009 | — | — | ||

| 2012 | — | — | ||

| 2015 | — | — | ||

| 2017 | — | — | ||

| 2018 | — | — | ||

| 2022 | — | — | ||

| 2025 | — | — |

Historical background

In 2008, Jamaica's currency situation was characterized by significant pressure and volatility, deeply intertwined with the global financial crisis and long-standing domestic vulnerabilities. The Jamaican dollar (JMD) faced sustained depreciation against the US dollar, a trend exacerbated by the country's chronic twin deficits—large fiscal and current account imbalances. High public debt, which exceeded 120% of GDP, consumed vast resources in debt servicing, leaving the economy highly susceptible to external shocks. As global credit markets seized up and commodity prices fluctuated, the traditional inflows from tourism, remittances, and bauxite/alumina exports weakened, reducing the foreign currency supply just as demand for imports remained inelastic.

The government, led by Prime Minister Bruce Golding, and the Bank of Jamaica (BOJ) intervened in the foreign exchange market in an attempt to stabilize the currency, spending substantial reserves to support the JMD. However, these efforts provided only temporary relief. Market confidence was further strained by the global flight to safety, which saw capital flowing out of emerging markets like Jamaica. By the end of the year, the JMD had depreciated by approximately 10% against the US dollar, with the exchange rate moving from around J$70 to over J$78, intensifying inflationary pressures and increasing the local cost of servicing foreign-denominated debt.

This precarious situation set the stage for Jamaica's eventual recourse to an International Monetary Fund (IMF) standby agreement in early 2010. The 2008 currency crisis underscored the structural weaknesses of the Jamaican economy, highlighting the unsustainable debt burden and its direct impact on exchange rate stability. It became a pivotal moment that reinforced the urgent need for the fiscal consolidation and economic reforms that would define the subsequent decade under an extended IMF program.

The government, led by Prime Minister Bruce Golding, and the Bank of Jamaica (BOJ) intervened in the foreign exchange market in an attempt to stabilize the currency, spending substantial reserves to support the JMD. However, these efforts provided only temporary relief. Market confidence was further strained by the global flight to safety, which saw capital flowing out of emerging markets like Jamaica. By the end of the year, the JMD had depreciated by approximately 10% against the US dollar, with the exchange rate moving from around J$70 to over J$78, intensifying inflationary pressures and increasing the local cost of servicing foreign-denominated debt.

This precarious situation set the stage for Jamaica's eventual recourse to an International Monetary Fund (IMF) standby agreement in early 2010. The 2008 currency crisis underscored the structural weaknesses of the Jamaican economy, highlighting the unsustainable debt burden and its direct impact on exchange rate stability. It became a pivotal moment that reinforced the urgent need for the fiscal consolidation and economic reforms that would define the subsequent decade under an extended IMF program.

🌱 Very Common