1 Dollar – New Zealand

New Zealand

Context

Material

Diameter: 40 mm

Weight: 31.1 g

Silver weight: 31.07 g

Shape: Round

Composition: 99.9% Silver

Standard: Silver ounce

Magnetic: No

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #Click to copy to clipboard519

Numista: #395082

Value

Exchange value: 1 NZD = $0.60

Bullion value: $87.17

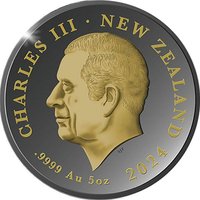

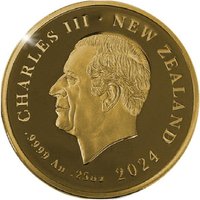

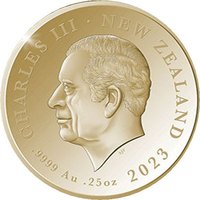

Obverse

Description:

Uncrowned portrait of King Charles III facing left.

Inscription:

CHARLES III NEW ZEALAND

SJF

.999 Ag 1oz 2024

SJF

.999 Ag 1oz 2024

Script: Latin

Designer: Stephen Fuller

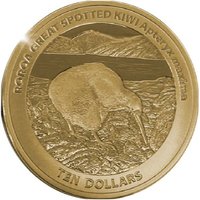

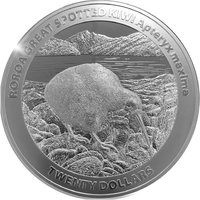

Reverse

Description:

A Roroa kiwi foraging before mountains.

Inscription:

ROROA GREAT SPOTTED KIWI Apteryx maxima

ONE DOLLAR

ONE DOLLAR

Script: Latin

Designer: Stevan Stojanovic

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| B. H. Mayer Kunstprageanstalt | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2024 | — | 5,000 | BU |

Historical background

In 2024, New Zealand's currency situation is characterised by a period of relative stability for the New Zealand Dollar (NZD) following the significant volatility of the preceding years. The NZD has traded within a contained range against major counterparts like the US Dollar (USD), largely influenced by a global "higher for longer" interest rate environment. While the Reserve Bank of New Zealand (RBNZ) has maintained the Official Cash Rate (OCR) at 5.5% to combat persistent domestic inflation, similar hawkish stances by other central banks, particularly the US Federal Reserve, have limited the NZD's traditional yield advantage and prevented a sharp appreciation.

Domestically, the currency faces crosscurrents from a slowing economy. Stubborn core inflation and a tight labour market provide underlying support, preventing a dramatic decline. However, weak consumer confidence, a cooling housing market, and the broader impact of high borrowing costs have tempered growth prospects. This economic softening has led markets to anticipate potential OCR cuts later in 2024 or early 2025, a outlook that weighs on the NZD's strength relative to currencies where rates are expected to remain elevated for longer.

Externally, the NZD remains sensitive to global risk sentiment and key export prices. As a commodity-linked currency, it benefits from sustained demand for New Zealand's dairy and meat exports, though prices have softened from earlier peaks. The primary external headwind is the strength of the USD, bolstered by resilient US economic data. Looking ahead, the NZD's trajectory will hinge on the timing and pace of the RBNZ's policy pivot compared to its global peers, alongside the performance of China's economy—a major trading partner—and broader shifts in geopolitical and financial market risk appetite.

Domestically, the currency faces crosscurrents from a slowing economy. Stubborn core inflation and a tight labour market provide underlying support, preventing a dramatic decline. However, weak consumer confidence, a cooling housing market, and the broader impact of high borrowing costs have tempered growth prospects. This economic softening has led markets to anticipate potential OCR cuts later in 2024 or early 2025, a outlook that weighs on the NZD's strength relative to currencies where rates are expected to remain elevated for longer.

Externally, the NZD remains sensitive to global risk sentiment and key export prices. As a commodity-linked currency, it benefits from sustained demand for New Zealand's dairy and meat exports, though prices have softened from earlier peaks. The primary external headwind is the strength of the USD, bolstered by resilient US economic data. Looking ahead, the NZD's trajectory will hinge on the timing and pace of the RBNZ's policy pivot compared to its global peers, alongside the performance of China's economy—a major trading partner—and broader shifts in geopolitical and financial market risk appetite.

Series: Great Spotted Kiwi 2024

✨ Legendary