100 pounds – Egypt

Add to wishlist

Egypt

Context

Year: 1992

Islamic (Hijri) Year:: 1412

Issuer: Egypt

Period:

(since 1971)

Currency:

(since 1916)

Total mintage: 148

Material

References

KM: #

Numista: #395026

Value

Exchange value: 100 EGP

Bullion value: $2350.52

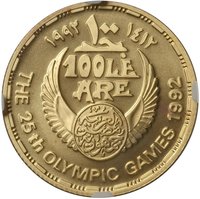

Obverse

Inscription:

١٤١٢ ١٩٩٢

١٠٠جـ

100 LE

ARE

جمهورية مصر العربية

THE 25TH OLYMPIC GAMES 1992

١٠٠جـ

100 LE

ARE

جمهورية مصر العربية

THE 25TH OLYMPIC GAMES 1992

Translation:

One Thousand Four Hundred Twelve 1992

One Hundred Pounds

100 LE

ARE

Arab Republic of Egypt

THE 25TH OLYMPIC GAMES 1992

One Hundred Pounds

100 LE

ARE

Arab Republic of Egypt

THE 25TH OLYMPIC GAMES 1992

Scripts: Arabic (naskh), Latin

Designers: Ibrahim Elhelw, Sabry Salah

Reverse

Description:

Hockey player

Inscription:

الدورة ٢٥ للألعاب الأوليمبية - برشلونة ١٩٩٢

Translation:

The 25th Olympiad - Barcelona 1992

Script: Arabic (kufic)

Language: Arabic

Designers: Ibrahim Elhelw, Sabry Salah

Edge

Reeded

Categories

| Sport> Summer Olympic Games |

| Sport> Hockey |

Mints

| Name | Mark |

|---|---|

| Egyptian Mint Authority | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1992 | — | 49 | ||

| 1992 | — | 99 | Proof |

Historical background

In 1992, Egypt was in the midst of a pivotal economic transition, grappling with the legacy of a tightly controlled, socialist-inspired system. The Egyptian pound (EGP) was officially pegged to the U.S. dollar, but this masked a complex and problematic dual-exchange-rate regime. The government maintained an overvalued official rate for priority imports and debt servicing, while a parallel "black market" rate flourished, reflecting the currency's true, weaker value. This disparity created significant distortions, encouraged corruption, and acted as a major deterrent to foreign investment and efficient trade.

Recognizing these crippling inefficiencies, the Egyptian government, under President Hosni Mubarak and with strong encouragement from the International Monetary Fund (IMF) and World Bank, had embarked on a structural adjustment program. A cornerstone of this reform, initiated in 1991, was the unification of the exchange rate. By early 1992, Egypt had largely succeeded in eliminating the official peg, allowing the pound to be determined by a new, more transparent interbank market. This devaluation was a painful but necessary step to correct the macroeconomic imbalances and unify the currency's value.

The immediate effect in 1992 was a significantly depreciated pound, increasing the cost of imports and contributing to inflation, which placed a burden on the population. However, the reforms were viewed as essential for long-term stability. The unified, market-driven exchange rate aimed to boost Egypt's competitiveness by making exports cheaper, attract crucial foreign capital, and restore international creditor confidence. Thus, 1992 stands as a defining year, marking Egypt's decisive, albeit challenging, shift from a state-controlled to a market-oriented currency system.

Recognizing these crippling inefficiencies, the Egyptian government, under President Hosni Mubarak and with strong encouragement from the International Monetary Fund (IMF) and World Bank, had embarked on a structural adjustment program. A cornerstone of this reform, initiated in 1991, was the unification of the exchange rate. By early 1992, Egypt had largely succeeded in eliminating the official peg, allowing the pound to be determined by a new, more transparent interbank market. This devaluation was a painful but necessary step to correct the macroeconomic imbalances and unify the currency's value.

The immediate effect in 1992 was a significantly depreciated pound, increasing the cost of imports and contributing to inflation, which placed a burden on the population. However, the reforms were viewed as essential for long-term stability. The unified, market-driven exchange rate aimed to boost Egypt's competitiveness by making exports cheaper, attract crucial foreign capital, and restore international creditor confidence. Thus, 1992 stands as a defining year, marking Egypt's decisive, albeit challenging, shift from a state-controlled to a market-oriented currency system.

Series: The 25th Olympic Games

✨ Legendary