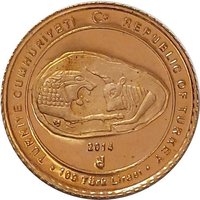

Obverse

Inscription:

TÜRKİYE CUMHURİYETİ

100 TL

2009

100 TL

2009

Translation:

REPUBLIC OF TURKEY

100 TL

2009

100 TL

2009

Script: Latin

Language: Turkish

Engraver: Tekin Gülbasar

Reverse

Description:

Kubaba's portrait and the Kadesh treaty.

Inscription:

ANADOLU MEDENİYETLERİ

KADEŞ ANTLAŞMASI M.Ö. 1269

KUBABA

HİTİTLER

M.Ö. 1600-700

KADEŞ ANTLAŞMASI M.Ö. 1269

KUBABA

HİTİTLER

M.Ö. 1600-700

Translation:

ANATOLIAN CIVILIZATIONS

TREATY OF KADESH 1269 BC

KUBABA

THE HITTITES

1600-700 BC

TREATY OF KADESH 1269 BC

KUBABA

THE HITTITES

1600-700 BC

Script: Latin

Language: Turkish

Engraver: Tekin Gülbasar

Edge

Reeded

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2009 | — | 1,000 | Proof |

Historical background

In 2009, Turkey's currency situation was defined by the severe aftershocks of the global financial crisis, which abruptly ended a period of strong growth and stability. The Turkish Lira (TRY), which had benefited from high foreign investment inflows and a reform-driven positive sentiment in the mid-2000s, came under intense pressure. As global risk appetite vanished, capital fled emerging markets, leading to a sharp depreciation of the Lira. Over the course of 2008-2009, the Lira lost approximately 25% of its value against the US dollar, severely straining corporations with foreign currency debt and raising concerns about financial stability.

The Central Bank of the Republic of Turkey (CBRT) responded with a series of aggressive interest rate cuts, slashing its benchmark rate from 16.75% in late 2008 to a historic low of 6.5% by November 2009. This bold, unorthodox strategy aimed to stimulate domestic demand and cushion the economic contraction, even as the currency weakened. The policy was partly viable because low global inflation and weak domestic demand limited immediate pass-through effects of the weaker Lira into consumer prices. The economy, heavily reliant on external financing, contracted by 4.8% in 2009, but the banking sector, restructured after the 2001 crisis, remained resilient and avoided collapse.

By the end of 2009, the currency situation had stabilized from its crisis lows, with the Lira recovering some ground as global conditions improved and risk appetite tentatively returned. However, the year established a precarious template: heavy reliance on short-term foreign capital inflows for growth and stability, and a central bank increasingly willing to prioritize growth over currency defense. This set the stage for the persistent "twin deficits" (current account and budget) and chronic currency volatility that would define the coming decade, as the deep rate cuts of 2009 marked the beginning of a long period of largely negative real interest rates.

The Central Bank of the Republic of Turkey (CBRT) responded with a series of aggressive interest rate cuts, slashing its benchmark rate from 16.75% in late 2008 to a historic low of 6.5% by November 2009. This bold, unorthodox strategy aimed to stimulate domestic demand and cushion the economic contraction, even as the currency weakened. The policy was partly viable because low global inflation and weak domestic demand limited immediate pass-through effects of the weaker Lira into consumer prices. The economy, heavily reliant on external financing, contracted by 4.8% in 2009, but the banking sector, restructured after the 2001 crisis, remained resilient and avoided collapse.

By the end of 2009, the currency situation had stabilized from its crisis lows, with the Lira recovering some ground as global conditions improved and risk appetite tentatively returned. However, the year established a precarious template: heavy reliance on short-term foreign capital inflows for growth and stability, and a central bank increasingly willing to prioritize growth over currency defense. This set the stage for the persistent "twin deficits" (current account and budget) and chronic currency volatility that would define the coming decade, as the deep rate cuts of 2009 marked the beginning of a long period of largely negative real interest rates.

✨ Legendary