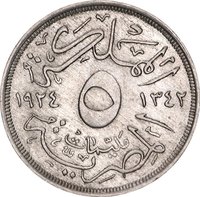

10 milliemes – Egypt

Add to wishlist

Egypt

Context

Year: 1924

Islamic (Hijri) Year:: 1342

Issuer: Egypt

Ruler: Ahmed Fuad I

Currency:

(since 1916)

Demonetized: Yes

Total mintage: 2,000,000

Material

Diameter: 23 mm

Weight: 5.19 g

Thickness: 1.6 mm

Shape: Round

Composition: Copper-nickel

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #10268

Value

Exchange value: 0.010 EGP

Obverse

Reverse

Edge

Plain

Mints

| Name | Mark |

|---|---|

| Royal Mint (Tower Hill) | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1924 | — | 2,000,000 |

Historical background

In 1924, Egypt's currency situation was defined by its continued adherence to the gold standard and its close, albeit evolving, financial ties to Britain. Following its nominal independence in 1922, Egypt remained within the British sphere of influence, and its monetary system reflected this. The Egyptian pound (EE), introduced in 1885, was pegged to gold and maintained a fixed parity with the British pound sterling, which itself was on the gold standard. This link ensured stability for international trade and foreign debt servicing, but it also meant that Egypt's monetary policy was largely dictated by the Bank of England and the economic conditions in London, limiting autonomous financial control.

The system in place was a currency board arrangement, managed by the National Bank of Egypt, which issued banknotes fully backed by gold and sterling securities. This strict convertibility guaranteed the currency's strength and public confidence, making the Egyptian pound one of the most stable currencies in the region. However, this rigidity also meant that the money supply was directly tied to Egypt's balance of payments. A surplus would bring in gold and sterling, allowing for more local currency issuance, while a deficit would contract the money supply, potentially exacerbating economic downturns without the ability for discretionary central banking intervention.

This framework existed amidst a period of growing Egyptian nationalism and economic development. While the stability attracted foreign investment and facilitated the booming cotton exports that were central to the economy, it was increasingly seen by Egyptian intellectuals and political figures as a symbol of lingering colonial control. The debate over monetary sovereignty would simmer throughout the 1920s and 1930s, setting the stage for future calls for a truly independent central bank and a monetary policy tailored to Egypt's domestic needs, rather than the imperatives of the British Empire.

The system in place was a currency board arrangement, managed by the National Bank of Egypt, which issued banknotes fully backed by gold and sterling securities. This strict convertibility guaranteed the currency's strength and public confidence, making the Egyptian pound one of the most stable currencies in the region. However, this rigidity also meant that the money supply was directly tied to Egypt's balance of payments. A surplus would bring in gold and sterling, allowing for more local currency issuance, while a deficit would contract the money supply, potentially exacerbating economic downturns without the ability for discretionary central banking intervention.

This framework existed amidst a period of growing Egyptian nationalism and economic development. While the stability attracted foreign investment and facilitated the booming cotton exports that were central to the economy, it was increasingly seen by Egyptian intellectuals and political figures as a symbol of lingering colonial control. The debate over monetary sovereignty would simmer throughout the 1920s and 1930s, setting the stage for future calls for a truly independent central bank and a monetary policy tailored to Egypt's domestic needs, rather than the imperatives of the British Empire.

Series: 1924 Egypt circulation coins

🌱 Common