100 rupiah – Indonesia

Add to wishlist

Indonesia

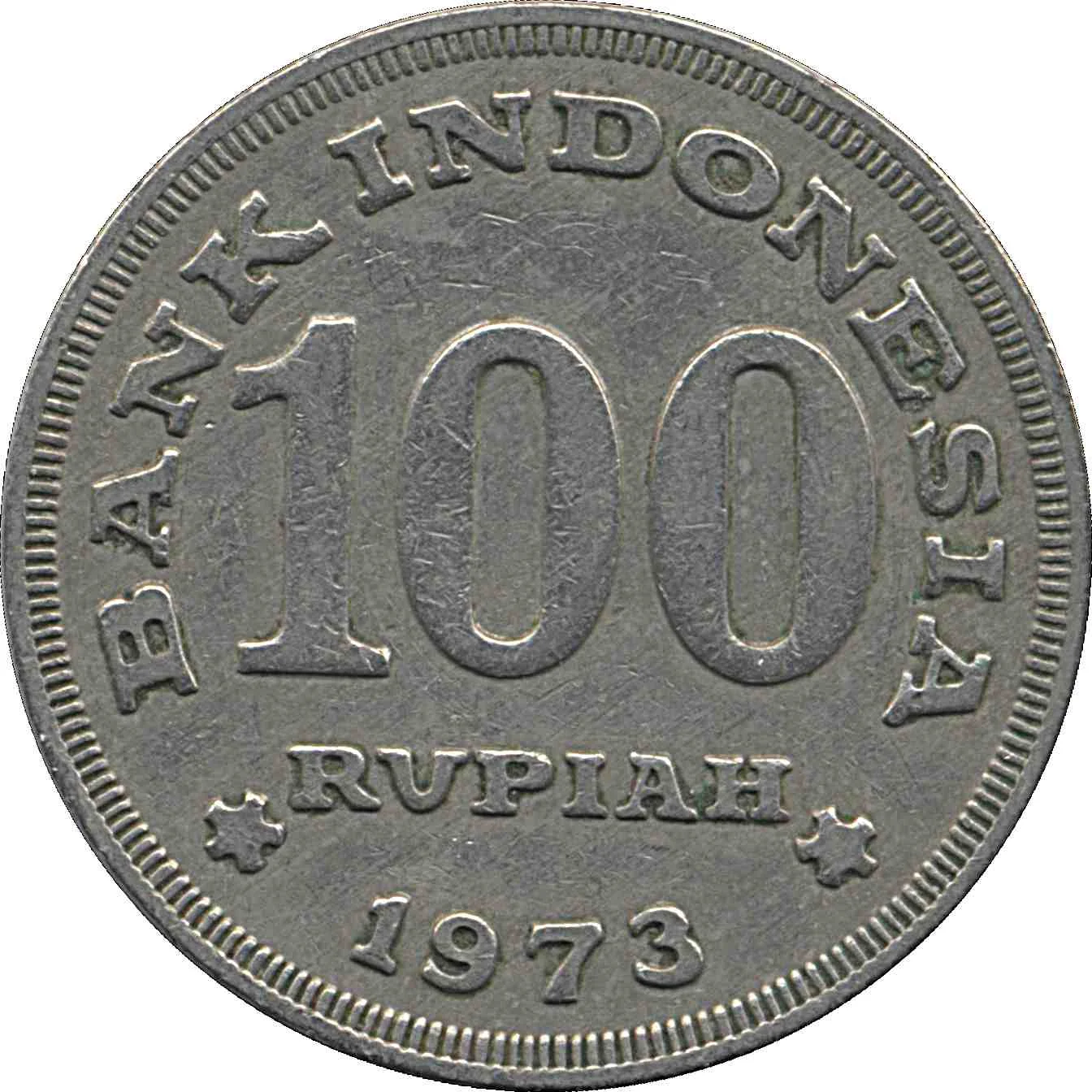

Obverse

Description:

Denomination

Inscription:

BANK INDONESIA

100

RUPIAH

1973

100

RUPIAH

1973

Translation:

BANK INDONESIA

100

RUPIAH

1973

100

RUPIAH

1973

Script: Latin

Languages: Indonesian, English

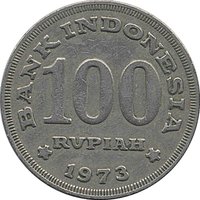

Reverse

Edge

Plain

Legend:

BANK*INDONESIA*

Mints

| Name | Mark |

|---|---|

| Perum Peruri | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1973 | — | 252,868,000 |

Historical background

In 1973, Indonesia's currency situation was characterized by a period of relative stability under the New Order government of President Suharto, but it was a stability built upon significant external support and underlying vulnerabilities. The cornerstone was the rupiah, which had been dramatically revalued and stabilized following the hyperinflation of the mid-1960s. A key policy was the fixed exchange rate regime established in 1971, pegging the rupiah at Rp 415 to the US dollar. This peg was maintained through strict fiscal discipline and critical financial backing from the International Monetary Fund (IMF) and a consortium of Western creditor nations known as the Inter-Governmental Group on Indonesia (IGGI).

This stability, however, was soon tested by global macroeconomic shocks. The year 1973 witnessed the collapse of the Bretton Woods system and the shift to floating major currencies, which put pressure on fixed pegs like Indonesia's. More significantly, the 1973 oil crisis triggered a global surge in petroleum prices. For Indonesia, a net oil exporter, this was a double-edged sword: it promised a massive windfall in export revenues that would soon transform the state budget, but it also immediately fueled domestic inflation and complicated exchange rate management as vast new petrodollars began flowing into the economy.

Consequently, 1973 served as a pivotal transition year. The fixed exchange rate remained officially in place, providing a facade of continuity, but the foundations were shifting. The incoming oil revenues, which would become fully apparent in 1974, began easing the severe foreign exchange constraints of the previous decade and reduced immediate pressure on the rupiah. However, they also set the stage for future challenges, including "Dutch Disease" and increased economic dependence on resource wealth, while the global monetary turbulence hinted at the future difficulties of maintaining a rigid peg in a new era of floating rates.

This stability, however, was soon tested by global macroeconomic shocks. The year 1973 witnessed the collapse of the Bretton Woods system and the shift to floating major currencies, which put pressure on fixed pegs like Indonesia's. More significantly, the 1973 oil crisis triggered a global surge in petroleum prices. For Indonesia, a net oil exporter, this was a double-edged sword: it promised a massive windfall in export revenues that would soon transform the state budget, but it also immediately fueled domestic inflation and complicated exchange rate management as vast new petrodollars began flowing into the economy.

Consequently, 1973 served as a pivotal transition year. The fixed exchange rate remained officially in place, providing a facade of continuity, but the foundations were shifting. The incoming oil revenues, which would become fully apparent in 1974, began easing the severe foreign exchange constraints of the previous decade and reduced immediate pressure on the rupiah. However, they also set the stage for future challenges, including "Dutch Disease" and increased economic dependence on resource wealth, while the global monetary turbulence hinted at the future difficulties of maintaining a rigid peg in a new era of floating rates.

🌱 Very Common