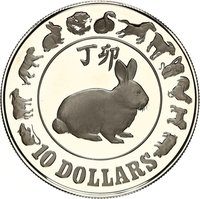

10 Dollars – Singapore

Non-circulating coins

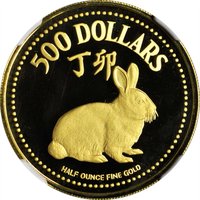

Commemoration: Year of the Rabbit

Singapore

Context

Material

References

KM: #Click to copy to clipboard66

Numista: #38318

Value

Exchange value: 10 SGD = $7.92

Obverse

Reverse

Description:

Rabbit facing right inside circle, with "10 DOLLARS" below and lunar animals around the border.

Inscription:

10 DOLLARS

Edge

Reeded

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1987 | — | 300,000 |

Historical background

In 1987, Singapore's currency situation was characterized by a period of managed stability and strategic evolution under the Monetary Authority of Singapore (MAS). Unlike a typical central bank, the MAS did not (and still does not) use interest rates as its primary tool. Instead, it employed a unique exchange rate-centered monetary policy, managing the Singapore dollar (SGD) against a secret trade-weighted basket of currencies of its major trading partners. This policy, formally adopted in 1981, was designed to control imported inflation and ensure the currency's external value remained aligned with the nation's trade-dependent economy, which was recovering robustly from a mid-1980s recession.

The SGD was, and remains, freely convertible and traded in international markets. By 1987, Singapore had firmly established itself as a burgeoning financial hub, and the currency's strength and stability were cornerstones of this reputation. The MAS's disciplined management ensured low and stable inflation, which was around 1% that year, fostering a conducive environment for both domestic business confidence and foreign investment. This stability was crucial as Singapore's economy was transitioning towards higher value-added sectors in manufacturing and expanding its service industries, particularly financial services.

Therefore, the 1987 currency landscape was one of deliberate and successful technocratic management. The MAS's focus on the exchange rate as its policy lever provided a stable monetary anchor, shielding the economy from volatile global capital flows and commodity price shocks. This stability was a key facilitator for the nation's continued economic restructuring and growth, setting a consistent framework that has underpinned Singapore's monetary philosophy for decades.

The SGD was, and remains, freely convertible and traded in international markets. By 1987, Singapore had firmly established itself as a burgeoning financial hub, and the currency's strength and stability were cornerstones of this reputation. The MAS's disciplined management ensured low and stable inflation, which was around 1% that year, fostering a conducive environment for both domestic business confidence and foreign investment. This stability was crucial as Singapore's economy was transitioning towards higher value-added sectors in manufacturing and expanding its service industries, particularly financial services.

Therefore, the 1987 currency landscape was one of deliberate and successful technocratic management. The MAS's focus on the exchange rate as its policy lever provided a stable monetary anchor, shielding the economy from volatile global capital flows and commodity price shocks. This stability was a key facilitator for the nation's continued economic restructuring and growth, setting a consistent framework that has underpinned Singapore's monetary philosophy for decades.

⭐ Rare