25 paisas – Pakistan

Add to wishlist

Pakistan

Context

Years: 1975–1981

Issuer: Pakistan

Period:

(since 1956)

Currency:

(since 1961)

Demonetization: 30 September 2014

Total mintage: 189,232,000

Material

References

KM: #

Numista: #3804

Value

Exchange value: 0.25 PKR

Obverse

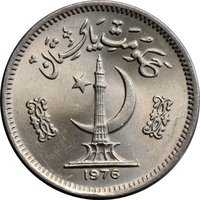

Description:

Urdu script at top, Minar-e-Pakistan with star and crescent in center, date at bottom.

Inscription:

حکومت پاکستان

1976

1976

Translation:

Government of Pakistan

1976

1976

Language: Urdu

Reverse

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Lahore | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1975 | — | — | ||

| 1976 | — | 20,440,000 | ||

| 1977 | — | 22,092,000 | ||

| 1978 | — | 33,544,000 | ||

| 1979 | — | 29,648,000 | ||

| 1980 | — | 49,556,000 | ||

| 1981 | — | 33,952,000 |

Historical background

In 1975, Pakistan's currency situation was characterized by relative stability under a managed exchange rate regime, a legacy of the Bretton Woods system. The Pakistani rupee was pegged to the pound sterling, and through that, indirectly to the U.S. dollar. This fixed parity, established at approximately 9.9 rupees to the dollar, provided predictability for international trade and was maintained by the State Bank of Pakistan through strict capital controls and the management of foreign exchange reserves. The period followed the 1971 war and the loss of East Pakistan, which had caused significant economic disruption, but by the mid-1970s, the economy under Prime Minister Zulfikar Ali Bhutto was showing signs of recovery, supported by remittances from overseas workers and aid flows.

However, underlying pressures were building. The nationalization of major industries, begun in 1972, created inefficiencies and dampened private investment. While remittances were rising, the country's export base remained narrow, reliant on primary goods like cotton. The fixed exchange rate, combined with higher global inflation following the 1973 oil crisis, began to make Pakistani exports less competitive. This led to a growing imbalance, as the cost of vital imports (including oil and machinery) increased, putting gradual pressure on foreign exchange reserves despite the official peg holding firm.

Consequently, 1975 represented a calm before a significant shift. The stability of the rupee was increasingly artificial, sustained by controls rather than fundamental economic strength. The pressures would culminate just a few years later, in 1982, when Pakistan was forced to devalue the rupee and abandon its fixed peg in favor of a managed float—a move that acknowledged the unsustainable nature of the mid-1970s status quo and the need for a more flexible exchange rate to address persistent trade deficits and balance of payments challenges.

However, underlying pressures were building. The nationalization of major industries, begun in 1972, created inefficiencies and dampened private investment. While remittances were rising, the country's export base remained narrow, reliant on primary goods like cotton. The fixed exchange rate, combined with higher global inflation following the 1973 oil crisis, began to make Pakistani exports less competitive. This led to a growing imbalance, as the cost of vital imports (including oil and machinery) increased, putting gradual pressure on foreign exchange reserves despite the official peg holding firm.

Consequently, 1975 represented a calm before a significant shift. The stability of the rupee was increasingly artificial, sustained by controls rather than fundamental economic strength. The pressures would culminate just a few years later, in 1982, when Pakistan was forced to devalue the rupee and abandon its fixed peg in favor of a managed float—a move that acknowledged the unsustainable nature of the mid-1970s status quo and the need for a more flexible exchange rate to address persistent trade deficits and balance of payments challenges.

🌱 Very Common