5 córdobas – Nicaragua

Add to wishlist

Nicaragua

Context

Material

Diameter: 27 mm

Weight: 8 g

Thickness: 3 mm

Shape: Round

Composition: Stainless steel

Technique: Milled

Alignment: Coin alignment

flip

References

KM: #

Numista: #371425

Value

Exchange value: 5 NIO

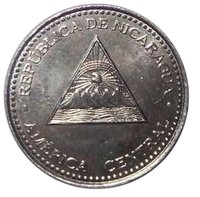

Obverse

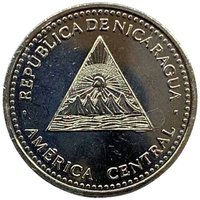

Reverse

Edge

Fine ribbed

Categories

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Mint of Poland | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2022 | — | — | ||

| 2024 | — | — |

Historical background

In 2022, Nicaragua’s currency situation was characterized by a managed dual-system, with the Nicaraguan Córdoba (NIO) circulating alongside the US Dollar. The Central Bank of Nicaragua (BCN) maintained a crawling peg exchange rate regime, where the córdoba was allowed to depreciate gradually against the dollar at a predetermined, controlled pace. This policy aimed to maintain export competitiveness and macroeconomic stability, but it operated within a context of significant political uncertainty and international isolation following the contentious 2021 elections and subsequent sanctions.

Economically, the country faced mounting pressures. Annual inflation accelerated sharply, reaching 11.45% by the end of 2022, driven largely by global increases in food and fuel prices. While the BCN raised its monetary policy interest rate to curb inflation, the stability of the official exchange rate masked underlying strains. A notable parallel market for dollars existed, where the córdoba traded at a discount compared to the official rate, reflecting lower confidence and higher demand for hard currency among businesses and individuals seeking a safe haven.

Despite these challenges, the Ortega government and the BCN presented the currency and financial system as stable, highlighting adequate international reserves and continued debt payments. The official narrative emphasized resilience, but independent analysts pointed to the widening gap between the official and parallel exchange rates, capital flight, and the broader erosion of economic freedom as signs of underlying fragility. The currency situation in 2022 thus reflected a managed stability on the surface, contingent on strict controls, but exposed to deeper structural and political risks that constrained long-term economic prospects.

Economically, the country faced mounting pressures. Annual inflation accelerated sharply, reaching 11.45% by the end of 2022, driven largely by global increases in food and fuel prices. While the BCN raised its monetary policy interest rate to curb inflation, the stability of the official exchange rate masked underlying strains. A notable parallel market for dollars existed, where the córdoba traded at a discount compared to the official rate, reflecting lower confidence and higher demand for hard currency among businesses and individuals seeking a safe haven.

Despite these challenges, the Ortega government and the BCN presented the currency and financial system as stable, highlighting adequate international reserves and continued debt payments. The official narrative emphasized resilience, but independent analysts pointed to the widening gap between the official and parallel exchange rates, capital flight, and the broader erosion of economic freedom as signs of underlying fragility. The currency situation in 2022 thus reflected a managed stability on the surface, contingent on strict controls, but exposed to deeper structural and political risks that constrained long-term economic prospects.

💎 Very Rare