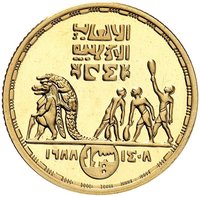

5 Pounds – Egypt

Non-circulating coins

Commemoration: 1988 Summer Olympics, Seoul

Series: 1988 Summer Olympics, Seoul

Egypt

Context

Year: 1988

Islamic (Hijri) Year: 1408

Issuer: Egypt

Period:

(since 1971)

Currency:

(since 1916)

Total mintage: 29,000

Material

References

KM: #Click to copy to clipboard626

Numista: #141411

Value

Exchange value: 5 EGP

Bullion value: $35.82

Obverse

Reverse

Inscription:

الالعاب الاولمبيه

٢٤

١٩٨٨ سيول ١٤٠٨

٢٤

١٩٨٨ سيول ١٤٠٨

Translation:

The Olympic Games

24

1988 Seoul 1408

24

1988 Seoul 1408

Language: Arabic

Edge

Categories

| Sport> Summer Olympic Games |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1988 | — | 24,000 | ||

| 1988 | — | — | Matte | |

| 1988 | — | 5,000 | Proof |

Historical background

In 1988, Egypt's currency situation was characterized by a strained and complex dual-exchange rate system, a legacy of economic pressures from the previous decade. The country maintained an official fixed rate for the Egyptian pound, which was significantly overvalued and used for government transactions and essential imports. Alongside this existed a more influential parallel "black market" rate, which reflected the currency's true market value and was used for most other transactions. This disparity created major distortions, encouraging capital flight, stifling investment, and fostering a widespread culture of currency speculation and rent-seeking.

The root causes lay in the economic policies of the 1970s, which, despite an initial boom, led to large fiscal deficits, heavy external borrowing, and soaring inflation. By the mid-1980s, a collapse in oil prices, a decline in remittances, and falling Suez Canal revenues triggered a severe foreign currency crisis. The government, hesitant to implement drastic reforms, relied on external aid and debt rescheduling while using its scarce hard currency reserves to defend the unsustainable official exchange rate. This policy drained reserves without addressing fundamental imbalances, perpetuating scarcity and a thriving black market.

Consequently, by 1988, the Egyptian economy was in a state of suspended correction. The black market premium was substantial, undermining formal economic planning and creating inefficiencies. The situation highlighted the urgent need for a structural adjustment program, setting the stage for the more decisive reforms that would follow in the early 1990s. These later reforms, negotiated with the IMF and World Bank, would eventually unify the exchange rates and devalue the pound, moving Egypt toward a more market-determined currency system.

The root causes lay in the economic policies of the 1970s, which, despite an initial boom, led to large fiscal deficits, heavy external borrowing, and soaring inflation. By the mid-1980s, a collapse in oil prices, a decline in remittances, and falling Suez Canal revenues triggered a severe foreign currency crisis. The government, hesitant to implement drastic reforms, relied on external aid and debt rescheduling while using its scarce hard currency reserves to defend the unsustainable official exchange rate. This policy drained reserves without addressing fundamental imbalances, perpetuating scarcity and a thriving black market.

Consequently, by 1988, the Egyptian economy was in a state of suspended correction. The black market premium was substantial, undermining formal economic planning and creating inefficiencies. The situation highlighted the urgent need for a structural adjustment program, setting the stage for the more decisive reforms that would follow in the early 1990s. These later reforms, negotiated with the IMF and World Bank, would eventually unify the exchange rates and devalue the pound, moving Egypt toward a more market-determined currency system.

Series: 1988 Summer Olympics, Seoul

✨ Legendary