50 Dollars – Cook Islands

Context

Material

Diameter: 38.8 mm

Weight: 31.1 g

Silver weight: 28.77 g

Shape: Round

Composition: 92.5% Silver

Standard: Silver ounce

Magnetic: No

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #Click to copy to clipboard202

Numista: #36846

Value

Exchange value: 50 NZD = $29.95

Bullion value: $81.78

Obverse

Description:

Queen Elizabeth II's effigy

Inscription:

ELIZABETH II COOK ISLANDS

RDM

1992

RDM

1992

Translation:

ELIZABETH II COOK ISLANDS

RDM

1992

RDM

1992

Script: Latin

Language: English

Designer: Raphael David Maklouf

Reverse

Description:

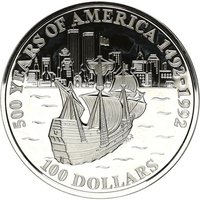

Horse-drawn wagon facing left before a U.S. map.

Inscription:

500 YEARS OF AMERICA

1492-1992

50 DOLLARS

1492-1992

50 DOLLARS

Script: Latin

Edge

Smooth with lettering

Legend:

* THE OREGON TRAIL * THE PIONEER ROUTE TO THE WEST

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1992 | — | 60,000 | Proof |

Historical background

In 1992, the currency situation in the Cook Islands was one of transition and national assertion, following a severe economic crisis. The country, a self-governing state in free association with New Zealand, had traditionally used the New Zealand dollar as its official currency. However, a devastating debt crisis in the mid-1990s, triggered by excessive government borrowing and a collapse in the tourism sector, led to a comprehensive restructuring program brokered with New Zealand and other creditors. This period set the immediate stage for a significant monetary change.

As part of broader efforts to stabilize the economy and assert national identity, the Cook Islands government introduced its own decimal currency, the Cook Islands dollar, in 1992. It was pegged at par with the New Zealand dollar, meaning the two currencies were intended to have equal value and could both circulate legally within the islands. The new currency featured distinct banknotes and coins, including the now-famous triangular $3 coin and notes depicting local culture and history, symbolizing a step towards greater economic self-definition.

However, this move was largely symbolic in terms of monetary policy. The New Zealand dollar remained the de facto anchor and preferred currency for major transactions and foreign trade, with the Cook Islands dollar serving primarily for domestic circulation. The 1992 introduction was therefore less about economic independence from New Zealand and more about national prestige and providing a tangible symbol of sovereignty, while remaining securely within the financial orbit of its larger partner to ensure stability during a fragile recovery period.

As part of broader efforts to stabilize the economy and assert national identity, the Cook Islands government introduced its own decimal currency, the Cook Islands dollar, in 1992. It was pegged at par with the New Zealand dollar, meaning the two currencies were intended to have equal value and could both circulate legally within the islands. The new currency featured distinct banknotes and coins, including the now-famous triangular $3 coin and notes depicting local culture and history, symbolizing a step towards greater economic self-definition.

However, this move was largely symbolic in terms of monetary policy. The New Zealand dollar remained the de facto anchor and preferred currency for major transactions and foreign trade, with the Cook Islands dollar serving primarily for domestic circulation. The 1992 introduction was therefore less about economic independence from New Zealand and more about national prestige and providing a tangible symbol of sovereignty, while remaining securely within the financial orbit of its larger partner to ensure stability during a fragile recovery period.

Series: 500 Years of America

💎 Extremely Rare