10 Rubles – Russian Federation

Russia

Context

Year: 2018

Country: Russia

Issuer: Russian Federation

Period:

(since 1991)

Currency:

(since 1998)

Total mintage: 5,000,000

Material

Diameter: 27 mm

Weight: 7.9 g

Thickness: 2.1 mm

Shape: Round

Standard: Silver quarter ounce

Techniques: Latent image, Milled

Alignment: Medal alignment

flip

References

Value

Exchange value: 10 RUB

Inflation-adjusted value: 18.91 RUB

Obverse

Description:

The central disc features "10 РУБЛЕЙ" with a holographic "10" and "РУБ" inside the zero, and the mint mark below. The ring bears "БАНК РОССИИ" at the top, "2018" at the bottom, and stylized plant twigs extending onto the disc.

Inscription:

БАНК РОССИИ

10

РУБЛЕЙ

ММД

2018

10

РУБЛЕЙ

ММД

2018

Translation:

BANK OF RUSSIA

10

RUBLES

MMD

2018

10

RUBLES

MMD

2018

Script: Cyrillic

Language: Russian

Designer and engraver: Alexander Vasilyevich Baklanov

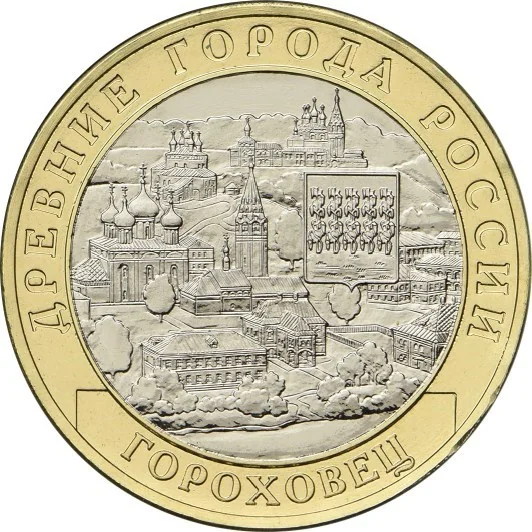

Reverse

Description:

Town panorama with Gorokhovets's coat of arms. Inscription: "ДРЕВНИЕ ГОРОДА РОССИИ" above, "ГОРОХОВЕЦ" below.

Inscription:

ДРЕВНИЕ ГОРОДА РОССИИ

ГОРОХОВЕЦ

ГОРОХОВЕЦ

Translation:

ANCIENT CITIES OF RUSSIA

GOROKHOVETS

GOROKHOVETS

Script: Cyrillic

Language: Russian

Designer and engraver: Fedor Sergeevich Andronov

Edge

300 corrugations and the inscription recurring twice and divided by asterisks

Legend:

ДЕСЯТЬ РУБЛЕЙ * ДЕСЯТЬ РУБЛЕЙ *

Translation:

TEN RUBLES * TEN RUBLES *

Language: Russian

Categories

| Symbols> Coat of Arms |

| Building> Religious building |

| Geography> Town |

Mints

| Name | Mark |

|---|---|

| Moscow Mint | (ММД) |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2018 | ММД | 5,000,000 |

Historical background

In 2018, the Russian ruble faced significant pressure, becoming one of the worst-performing currencies globally that year. The primary drivers were a combination of new U.S. sanctions and falling oil prices. In April, the U.S. imposed severe sanctions on several Russian oligarchs, their companies, and key government officials, causing immediate capital flight and a loss of investor confidence. This financial shock was compounded by a decline in the price of Brent crude, a crucial benchmark for Russia's oil-dependent economy, which fell from over $86 per barrel in October to near $50 by year's end. These twin shocks exposed the Russian economy's ongoing vulnerability to external geopolitical and commodity market forces.

The Central Bank of the Russian Federation (CBR) responded with a strategy focused on controlling inflation and maintaining financial stability, rather than defending a specific exchange rate. It allowed the ruble to float freely, acting as a "shock absorber" for the economy. Throughout the year, the CBR gradually increased its key interest rate, culminating in a hike to 7.75% in December, aimed at curbing inflation risks and making ruble assets more attractive to stem capital outflow. This approach, while leading to a significantly weaker currency, helped preserve foreign exchange reserves and prevented a full-blown financial crisis.

By the close of 2018, the ruble had depreciated by approximately 17% against the U.S. dollar compared to the start of the year. The situation underscored the lasting impact of the sanctions regime first imposed in 2014 and highlighted the structural challenges of an economy heavily reliant on hydrocarbon exports. Despite the volatility, the government's budget, calibrated to lower oil prices, and the CBR's orthodox monetary policy provided a degree of resilience, preventing the kind of panic seen during the 2014-2015 crisis, though at the cost of reduced purchasing power for the Russian population.

The Central Bank of the Russian Federation (CBR) responded with a strategy focused on controlling inflation and maintaining financial stability, rather than defending a specific exchange rate. It allowed the ruble to float freely, acting as a "shock absorber" for the economy. Throughout the year, the CBR gradually increased its key interest rate, culminating in a hike to 7.75% in December, aimed at curbing inflation risks and making ruble assets more attractive to stem capital outflow. This approach, while leading to a significantly weaker currency, helped preserve foreign exchange reserves and prevented a full-blown financial crisis.

By the close of 2018, the ruble had depreciated by approximately 17% against the U.S. dollar compared to the start of the year. The situation underscored the lasting impact of the sanctions regime first imposed in 2014 and highlighted the structural challenges of an economy heavily reliant on hydrocarbon exports. Despite the volatility, the government's budget, calibrated to lower oil prices, and the CBR's orthodox monetary policy provided a degree of resilience, preventing the kind of panic seen during the 2014-2015 crisis, though at the cost of reduced purchasing power for the Russian population.

Series: Ancient Towns of Russia

🌱 Common