50 Dollars – Australia

Australia

Context

Material

Diameter: 25.6 mm

Weight: 15.55 g

Gold weight: 15.55 g

Thickness: 2.4 mm

Shape: Round

Composition: 99.99% Gold

Standard: Silver half ounce

Magnetic: No

Technique: Milled

Alignment: Medal alignment

flip

References

Numista: #368174

Value

Exchange value: 50 AUD = $35.60

Bullion value: $2592.40

Inflation-adjusted value: 80.97 AUD

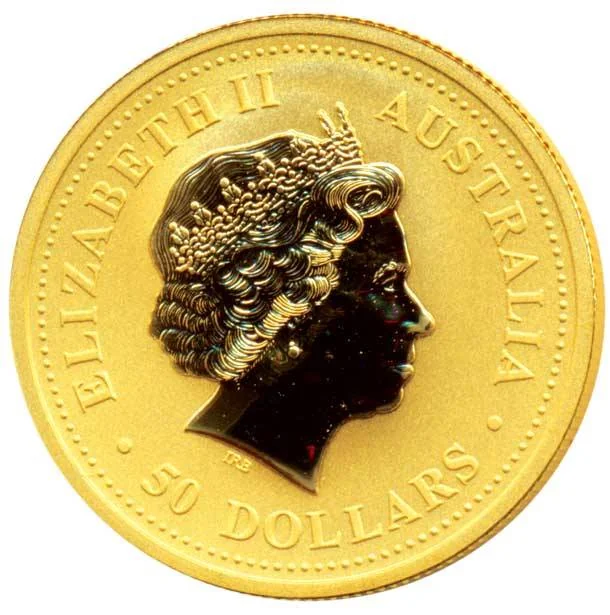

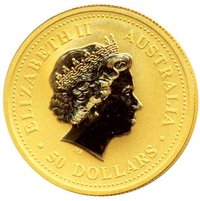

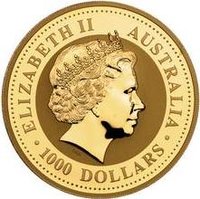

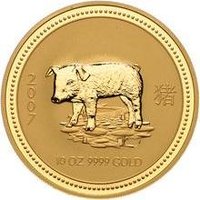

Obverse

Description:

Queen Elizabeth IV, facing right, wearing the Girls of Great Britain and Ireland Tiara.

Inscription:

ELIZABETH II

AUSTRALIA

50 DOLLARS

IRB

AUSTRALIA

50 DOLLARS

IRB

Script: Latin

Designer: Ian Rank-Broadley

Reverse

Description:

Kangaroo facing left.

Inscription:

THE AUSTRALIAN NUGGET

1/2 oz 9999 GOLD

2007

JG

1/2 oz 9999 GOLD

2007

JG

Script: Latin

Designer: Justin Graham

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Perth Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2007 | — | 13,780 | BU |

Historical background

In 2007, Australia's currency landscape was defined by the Australian dollar's remarkable ascent, driven by a powerful confluence of global and domestic factors. The currency, often referred to as the "Aussie," began the year trading around US$0.78 and surged to break the symbolic US$0.90 barrier by year's end, a level not seen since before its float in 1983. This dramatic appreciation was primarily fueled by a sustained global commodities boom, with soaring demand from China and other emerging economies driving up prices for Australia's key exports like iron ore, coal, and liquefied natural gas. This created strong underlying demand for the currency.

Domestically, the economic backdrop reinforced the dollar's strength. The Australian economy was in its 16th consecutive year of expansion, boasting low unemployment and persistent inflationary pressures. Consequently, the Reserve Bank of Australia (RBA) maintained a relatively high-interest-rate environment, with the official cash rate reaching 6.75% in November after two hikes during the year. This rate differential made Australian assets highly attractive to foreign investors seeking yield, further increasing capital inflows and demand for the Aussie dollar.

However, this strength presented a classic "two-speed economy" challenge. While the booming resources sector and related industries benefited, the high currency exerted severe pressure on other parts of the economy. Exporters in manufacturing, tourism, and education faced reduced international competitiveness, and import-competing industries struggled against cheaper foreign goods. As 2007 closed, policymakers and businesses were acutely aware of these divergent pressures, even as the currency's climb reflected robust national income. The global financial crisis, which began to unfold in mid-2007, had not yet significantly impacted Australia's economy or currency, leaving the "Aussie" at a multi-decade high as the year concluded.

Domestically, the economic backdrop reinforced the dollar's strength. The Australian economy was in its 16th consecutive year of expansion, boasting low unemployment and persistent inflationary pressures. Consequently, the Reserve Bank of Australia (RBA) maintained a relatively high-interest-rate environment, with the official cash rate reaching 6.75% in November after two hikes during the year. This rate differential made Australian assets highly attractive to foreign investors seeking yield, further increasing capital inflows and demand for the Aussie dollar.

However, this strength presented a classic "two-speed economy" challenge. While the booming resources sector and related industries benefited, the high currency exerted severe pressure on other parts of the economy. Exporters in manufacturing, tourism, and education faced reduced international competitiveness, and import-competing industries struggled against cheaper foreign goods. As 2007 closed, policymakers and businesses were acutely aware of these divergent pressures, even as the currency's climb reflected robust national income. The global financial crisis, which began to unfold in mid-2007, had not yet significantly impacted Australia's economy or currency, leaving the "Aussie" at a multi-decade high as the year concluded.

Series: Australian Nugget

✨ Legendary