20 dollars – Canada

Add to wishlist

Canada

Context

Material

References

KM: #

Numista: #366806

Value

Exchange value: 20 CAD

Bullion value: $79.24

Inflation-adjusted value: 21.40 CAD

Obverse

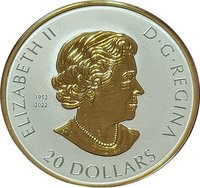

Description:

Queen Elizabeth II at 77, facing right, wearing a necklace and earrings. Below, the dates 1952 and 2022 are separated by four pearls, representing the four effigies on Canadian coins during her reign.

Inscription:

ELIZABETH II

1952

••••

2022

20 DOLLARS 2023

SB

1952

••••

2022

20 DOLLARS 2023

SB

Script: Latin

Engraver: Susan Taylor

Designer: Susanna Blunt

Reverse

Description:

Your coin's reverse features the classic maple leaf design, now struck for the first time with Super Incuse technology for a 1.5mm depth. A modified reverse proof finish highlights the brilliant relief.

Inscription:

CANADA

9999 9999

FINE SILVER 1 OZ ARGENT PUR

9999 9999

FINE SILVER 1 OZ ARGENT PUR

Script: Latin

Designer: Walter Ott

Edge

Serrated

Mints

| Name | Mark |

|---|---|

| Royal Canadian Mint of Ottawa | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2023 | — | 8,000 | Proof |

Historical background

In 2023, Canada's currency situation was defined by a prolonged period of elevated inflation and the Bank of Canada's aggressive monetary policy response. The year began with the Canadian dollar (CAD) under pressure, trading around 73.5 US cents, as markets priced in a potential pause in the U.S. Federal Reserve's rate hikes. However, the dominant narrative was the Bank of Canada's (BoC) ongoing battle to rein in inflation, which had peaked at 8.1% in mid-2022 but remained stubbornly above the 2% target. The central bank implemented a series of interest rate increases, bringing its key policy rate to a 22-year high of 5.0% by July 2023, creating a tight monetary environment.

This high-interest-rate policy had a dual impact on the loonie. On one hand, it provided fundamental support by attracting foreign capital seeking yield, helping the CAD recover to trade in a range of roughly 72 to 76 US cents for much of the year. On the other hand, the strength was capped by broader global factors, including a stronger U.S. dollar driven by robust American economic data and persistent geopolitical uncertainty. Domestically, concerns about slowing economic growth and a cooling housing market, both consequences of the high-rate environment, created headwinds that prevented a more dramatic appreciation.

By the end of 2023, the currency landscape was in a holding pattern. Inflation showed signs of moderating, dropping to 3.1% in November, which led the BoC to hold rates steady in its final meetings of the year. The market's focus shifted from rate hikes to the timing of future rate cuts, with expectations building for 2024. Consequently, the Canadian dollar closed the year relatively flat against the U.S. dollar, reflecting a balance between domestic economic resilience, cautious optimism on inflation, and a wait-and-see approach from the central bank as it navigated the path toward a soft economic landing.

This high-interest-rate policy had a dual impact on the loonie. On one hand, it provided fundamental support by attracting foreign capital seeking yield, helping the CAD recover to trade in a range of roughly 72 to 76 US cents for much of the year. On the other hand, the strength was capped by broader global factors, including a stronger U.S. dollar driven by robust American economic data and persistent geopolitical uncertainty. Domestically, concerns about slowing economic growth and a cooling housing market, both consequences of the high-rate environment, created headwinds that prevented a more dramatic appreciation.

By the end of 2023, the currency landscape was in a holding pattern. Inflation showed signs of moderating, dropping to 3.1% in November, which led the BoC to hold rates steady in its final meetings of the year. The market's focus shifted from rate hikes to the timing of future rate cuts, with expectations building for 2024. Consequently, the Canadian dollar closed the year relatively flat against the U.S. dollar, reflecting a balance between domestic economic resilience, cautious optimism on inflation, and a wait-and-see approach from the central bank as it navigated the path toward a soft economic landing.

Series: Super Incuse SML

💎 Extremely Rare