5 rupees (United Nations) – Pakistan

Add to wishlist

Circulating commemorative coins

Commemoration: 50th Anniversary of the United Nations

Pakistan

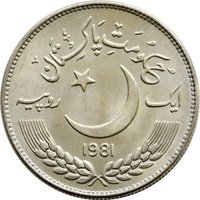

Obverse

Description:

Crescent and star over grain sprigs.

Inscription:

حكومت پاکستان

5

روپيه

1995

5

روپيه

1995

Translation:

Government of Pakistan

5

Rupee

1995

5

Rupee

1995

Language: Urdu

Reverse

Description:

50th anniversary, UN logo

Inscription:

50

Translation:

Of the Emperor Caesar Marcus Aurelius Commodus Antoninus Augustus, Conqueror of the Germans, Conqueror of the Britons, Pius, Felix.

Language: Latin

Edge

Reeded

Categories

| Organization> United Nations |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1995 | — | 500,000 |

Historical background

In 1995, Pakistan's currency situation was characterized by mounting pressure and a stark duality between official and market exchange rates. The Pakistani rupee, officially pegged to a basket of currencies but effectively managed against the US dollar, was held at an artificially strong rate of approximately Rs. 31-32 to the dollar by the government of Prime Minister Benazir Bhutto. This overvalued peg was maintained to control inflation and the cost of imports, including essential oil, but it came at a significant cost to the country's export competitiveness and foreign exchange reserves.

Beneath the surface of this managed stability, a severe economic crisis was brewing. The official rate masked a thriving black market where the rupee traded for as high as Rs. 40-42 per dollar, reflecting a severe shortage of foreign currency. This disparity was fueled by a large current account deficit, dwindling reserves that fell below $1 billion (covering only weeks of imports), and a loss of confidence from international lenders like the IMF. Exports, particularly of key textiles, were stifled by the uncompetitive official rate, while remittances from overseas workers were increasingly channeled through the more lucrative informal hawala system instead of official banking channels.

Consequently, 1995 proved to be the final year of the unsustainable peg. The pressure became untenable, forcing the government to initiate a major devaluation in early 1996. This move, a reluctant shift towards a more market-determined exchange rate, was a precondition for securing critical IMF support. Thus, the currency dynamics of 1995 set the stage for a profound economic adjustment, marking the end of a rigid exchange regime and the beginning of a painful but necessary transition towards greater currency flexibility in the face of a severe balance of payments crisis.

Beneath the surface of this managed stability, a severe economic crisis was brewing. The official rate masked a thriving black market where the rupee traded for as high as Rs. 40-42 per dollar, reflecting a severe shortage of foreign currency. This disparity was fueled by a large current account deficit, dwindling reserves that fell below $1 billion (covering only weeks of imports), and a loss of confidence from international lenders like the IMF. Exports, particularly of key textiles, were stifled by the uncompetitive official rate, while remittances from overseas workers were increasingly channeled through the more lucrative informal hawala system instead of official banking channels.

Consequently, 1995 proved to be the final year of the unsustainable peg. The pressure became untenable, forcing the government to initiate a major devaluation in early 1996. This move, a reluctant shift towards a more market-determined exchange rate, was a precondition for securing critical IMF support. Thus, the currency dynamics of 1995 set the stage for a profound economic adjustment, marking the end of a rigid exchange regime and the beginning of a painful but necessary transition towards greater currency flexibility in the face of a severe balance of payments crisis.

🌱 Fairly Common