50 rupees (Independence) – Pakistan

Add to wishlist

Circulating commemorative coins

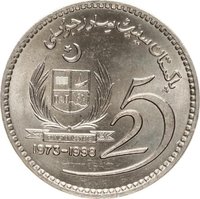

Commemoration: 50 Years of Independence.

Pakistan

Context

Material

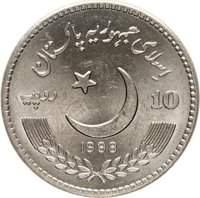

Diameter: 35.25 mm

Weight: 20 g

Thickness: 2.5 mm

Shape: Round

Composition: Copper-nickel

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #9745

Value

Exchange value: 50 PKR

Obverse

Reverse

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Lahore | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1997 | — | — |

Historical background

In 1997, Pakistan's currency situation was characterized by significant pressure and a managed devaluation, set against a backdrop of chronic economic challenges. The Pakistani rupee (PKR), officially pegged to the US dollar but in practice managed through a controlled float, faced sustained downward pressure. This was driven by a widening current account deficit, declining foreign exchange reserves, and a heavy external debt burden. The government, led by Prime Minister Nawaz Sharif, was attempting to implement structural reforms under an IMF program, but political uncertainty and tensions with judicial institutions created an environment of instability that undermined investor confidence.

Economically, the country was grappling with the aftermath of the 1995-96 crisis, where reserves had plummeted. While some stabilization had occurred, key issues persisted. Exports, primarily textiles, were struggling to compete, while imports remained high, leading to a persistent trade gap. Furthermore, the nuclear sanctions imposed after the 1998 tests were looming on the horizon, creating anticipatory market anxiety. The State Bank of Pakistan was actively intervening in the currency market to smooth the rupee's decline, but this was depleting already modest reserves, creating a precarious balance between defending the currency and maintaining liquidity.

Consequently, the rupee experienced a steady depreciation throughout the year. The official exchange rate, which was around PKR 40 to the US dollar at the start of 1997, weakened to approximately PKR 44 by year's end. This controlled devaluation was a deliberate, though difficult, policy choice aimed at boosting export competitiveness and aligning the official rate closer to the higher black-market rate. However, it also increased the cost of servicing foreign debt and contributed to inflationary pressures, setting the stage for the more severe currency crisis that would unfold in 1998 following the nuclear tests and the subsequent freezing of foreign currency accounts.

Economically, the country was grappling with the aftermath of the 1995-96 crisis, where reserves had plummeted. While some stabilization had occurred, key issues persisted. Exports, primarily textiles, were struggling to compete, while imports remained high, leading to a persistent trade gap. Furthermore, the nuclear sanctions imposed after the 1998 tests were looming on the horizon, creating anticipatory market anxiety. The State Bank of Pakistan was actively intervening in the currency market to smooth the rupee's decline, but this was depleting already modest reserves, creating a precarious balance between defending the currency and maintaining liquidity.

Consequently, the rupee experienced a steady depreciation throughout the year. The official exchange rate, which was around PKR 40 to the US dollar at the start of 1997, weakened to approximately PKR 44 by year's end. This controlled devaluation was a deliberate, though difficult, policy choice aimed at boosting export competitiveness and aligning the official rate closer to the higher black-market rate. However, it also increased the cost of servicing foreign debt and contributed to inflationary pressures, setting the stage for the more severe currency crisis that would unfold in 1998 following the nuclear tests and the subsequent freezing of foreign currency accounts.

🌱 Fairly Common