50 rupees (Khadi & Village Industries Commission) – India

Add to wishlist

Non-circulating coins

Commemoration: 50th Anniversary of Khadi & Village Industries Commission

India

Material

References

KM: #

Numista: #36266

Value

Exchange value: 50 INR

Bullion value: $28.05

Inflation-adjusted value: 170.32 INR

Obverse

Description:

Face Value with Ashoka Pillar

Inscription:

भारत 50 रुपये

India 50 Rupees

India 50 Rupees

Translation:

India 50 Rupees

Language: Hindi

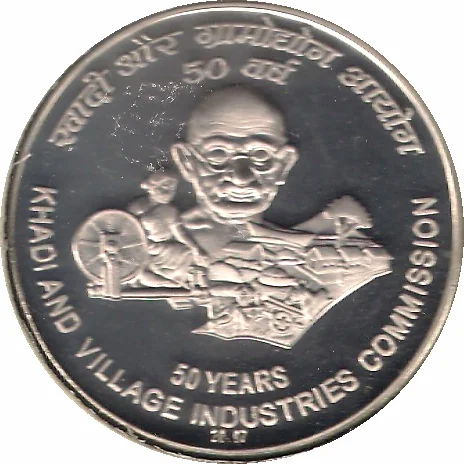

Reverse

Inscription:

खादी और ग्रामोद्योग आयोग, ५० वर्ष

50 Years, Khadi and Village Industries Commission

50 Years, Khadi and Village Industries Commission

Translation:

Khadi and Village Industries Commission, 50 Years

Language: Hindi

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Mumbai / Bombay | ♦ |

| Mumbai / Bombay | M |

Historical background

In 2007, India's currency situation was characterized by robust economic growth and significant pressure on the Indian Rupee (INR) to appreciate. The economy was expanding at a rate of over 9%, attracting substantial foreign capital inflows, both as Foreign Direct Investment (FDI) and portfolio investments in a booming stock market. This surge in dollar inflows created an imbalance, increasing the supply of foreign currency and driving up demand for the rupee. Consequently, the Reserve Bank of India (RBI) faced a complex challenge: an appreciating rupee threatened to make Indian exports less competitive in the global market, a major concern for a key sector like information technology.

To manage this volatility and stem the rupee's rise, the RBI actively intervened in the foreign exchange market by purchasing dollars and building up its foreign exchange reserves, which soared to nearly $300 billion by year's end. This intervention was part of a "managed float" regime. However, these dollar purchases injected large amounts of rupee liquidity into the banking system, risking inflation. To sterilize this effect and control money supply, the RBI simultaneously engaged in Open Market Operations (OMOs), selling government bonds to absorb the excess liquidity. This delicate balancing act defined much of the year's monetary policy.

Despite these interventions, the rupee ended 2007 significantly stronger, appreciating by approximately 12% against the US dollar. This appreciation was a double-edged sword; while it reduced the cost of imports like oil, it squeezed profit margins for exporters. The situation underscored the tensions of a rapidly globalizing economy. Furthermore, the latter part of 2007 brought early shadows of the impending global financial crisis, which would, by 2008, dramatically reverse capital flows and plunge the rupee into a phase of depreciation and volatility, ending a period of sustained strength.

To manage this volatility and stem the rupee's rise, the RBI actively intervened in the foreign exchange market by purchasing dollars and building up its foreign exchange reserves, which soared to nearly $300 billion by year's end. This intervention was part of a "managed float" regime. However, these dollar purchases injected large amounts of rupee liquidity into the banking system, risking inflation. To sterilize this effect and control money supply, the RBI simultaneously engaged in Open Market Operations (OMOs), selling government bonds to absorb the excess liquidity. This delicate balancing act defined much of the year's monetary policy.

Despite these interventions, the rupee ended 2007 significantly stronger, appreciating by approximately 12% against the US dollar. This appreciation was a double-edged sword; while it reduced the cost of imports like oil, it squeezed profit margins for exporters. The situation underscored the tensions of a rapidly globalizing economy. Furthermore, the latter part of 2007 brought early shadows of the impending global financial crisis, which would, by 2008, dramatically reverse capital flows and plunge the rupee into a phase of depreciation and volatility, ending a period of sustained strength.

⭐ Somewhat Rare