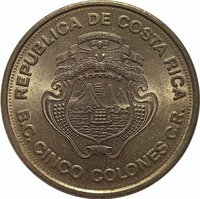

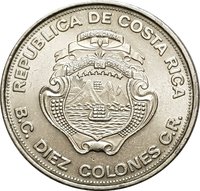

5 colones (Central Bank) – Costa Rica

Add to wishlist

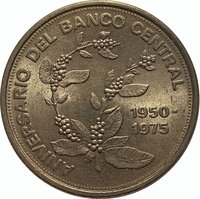

Circulating commemorative coins

Commemoration: 25th Anniversary of the Central Bank

Costa Rica

Context

Year: 1975

Issuer: Costa Rica

Issuing organization: Central Bank of Costa Rica

Period:

(since 1948)

Currency:

(since 1896)

Demonetized: Yes

Total mintage: 2,000,000

Material

References

KM: #

Numista: #3624

Value

Exchange value: 5 CRC

Obverse

Description:

Costa Rica's coat of arms features seven stars for its provinces, three volcanoes for its mountain ranges, two ships for its position between oceans, and a sunrise. The value is encircled by the initials "B.C.C.R." for the central bank.

Inscription:

REPUBLICA DE COSTA RICA

AMERICA CENTRAL

REPUBLICA DE COSTA RICA

B.C. CINCO COLONES C.R.

AMERICA CENTRAL

REPUBLICA DE COSTA RICA

B.C. CINCO COLONES C.R.

Translation:

REPUBLIC OF COSTA RICA

CENTRAL AMERICA

REPUBLIC OF COSTA RICA

B.C. FIVE COLONES C.R.

CENTRAL AMERICA

REPUBLIC OF COSTA RICA

B.C. FIVE COLONES C.R.

Script: Latin

Language: Spanish

Reverse

Edge

Reeded

Categories

| Symbols> Coat of Arms |

| Plants> Flower |

Mints

| Name | Mark |

|---|---|

| VDM Metals / Vereinigte Deutsche Metallwerke | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1975 | — | 2,000,000 |

Historical background

In 1975, Costa Rica's currency situation was characterized by a managed exchange rate regime under the Bretton Woods system, with the colón pegged to the U.S. dollar. The official exchange rate was fixed at 8.57 colones per dollar, a rate that had been maintained since 1974. However, this official peg masked underlying economic pressures. The country was experiencing persistent fiscal deficits, largely financed by central bank credit, which fueled inflation and eroded the colón's real value. This created a growing divergence between the official rate and the currency's true market value, leading to pressures on foreign reserves.

Economically, the period was one of transition and strain. Costa Rica was still benefiting from the high coffee prices of the early 1970s, but this boom was beginning to wane. The first oil shock of 1973 had significantly increased import costs, worsening the trade balance and putting downward pressure on the colón. Furthermore, the expansionary fiscal policies of the administration of President Daniel Oduber, including significant public investment and social spending, contributed to growing macroeconomic imbalances. These factors collectively created a classic scenario for an overvalued currency, which discouraged exports (beyond the booming coffee sector) and encouraged imports, further depleting reserves.

Consequently, 1975 set the stage for the profound currency crisis that would erupt later in the decade. While the fixed exchange rate was officially maintained, the mounting pressures led to the emergence and growth of a parallel black market for U.S. dollars, where the colón traded at a significant discount. This disparity signaled a loss of confidence and foreshadowed the inevitable breakdown of the fixed parity. The unsustainable policies of this period ultimately culminated in a major economic crisis in the early 1980s, necessitating a devaluation, the adoption of a crawling peg system, and structural adjustment programs supported by the International Monetary Fund.

Economically, the period was one of transition and strain. Costa Rica was still benefiting from the high coffee prices of the early 1970s, but this boom was beginning to wane. The first oil shock of 1973 had significantly increased import costs, worsening the trade balance and putting downward pressure on the colón. Furthermore, the expansionary fiscal policies of the administration of President Daniel Oduber, including significant public investment and social spending, contributed to growing macroeconomic imbalances. These factors collectively created a classic scenario for an overvalued currency, which discouraged exports (beyond the booming coffee sector) and encouraged imports, further depleting reserves.

Consequently, 1975 set the stage for the profound currency crisis that would erupt later in the decade. While the fixed exchange rate was officially maintained, the mounting pressures led to the emergence and growth of a parallel black market for U.S. dollars, where the colón traded at a significant discount. This disparity signaled a loss of confidence and foreshadowed the inevitable breakdown of the fixed parity. The unsustainable policies of this period ultimately culminated in a major economic crisis in the early 1980s, necessitating a devaluation, the adoption of a crawling peg system, and structural adjustment programs supported by the International Monetary Fund.

🌱 Common