Obverse

Description:

Mexican coat of arms centered, with legend above, flanked by silver details. Value below, mintmark and date at bottom.

Inscription:

ESTADOS UNIDOS MEXICANOS

PESO 27 7/9 G LEY 0.720

CINCO PESOS

Mo 1952

PESO 27 7/9 G LEY 0.720

CINCO PESOS

Mo 1952

Translation:

UNITED MEXICAN STATES

PESO 27 7/9 G FINENESS 0.720

FIVE PESOS

Mo 1952

PESO 27 7/9 G FINENESS 0.720

FIVE PESOS

Mo 1952

Script: Latin

Language: Spanish

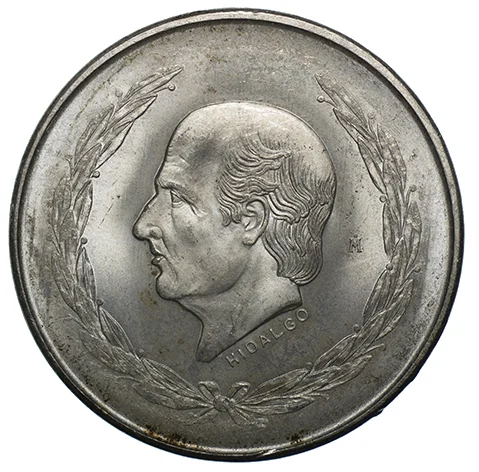

Reverse

Edge

Smooth with inscription

Legend:

COMERCIO AGRICULTURA INDUSTRIA

Translation:

Commerce, Agriculture, Industry

Language: Spanish

Mints

| Name | Mark |

|---|---|

| Mexican Mint | Mo |

Mintings

Historical background

In 1951, Mexico's currency situation was characterized by a period of relative stability under the Bretton Woods system, but with underlying pressures rooted in the country's rapid industrialization drive. The Mexican peso was pegged to the U.S. dollar at a fixed rate of 8.65 pesos per dollar, a parity established in 1949 and maintained through the Central Bank's management of foreign reserves. This stability was a point of pride for the administration of President Miguel Alemán (1946-1952), supporting a climate of confidence for both domestic investment and foreign capital, which was seen as crucial for the development of infrastructure and industry.

However, this fixed exchange rate existed alongside persistent, though moderate, inflation and a growing demand for imports of capital goods and machinery. Mexico's economic strategy, known as "stabilizing development," prioritized industrial growth over strict price stability, leading to a gradual erosion of the peso's purchasing power domestically. While the currency's external value was firmly anchored, its internal value was slowly declining. This created a subtle overvaluation of the peso, which began to discourage agricultural exports and encouraged spending on imports, applying a slow but steady drain on the country's dollar reserves.

Consequently, 1951 represented a calm before a gathering storm. The policies of the Alemán sexenio had fueled growth through substantial public spending and credit expansion, setting the stage for the balance of payments crises that would challenge the next administration. The fixed parity of 8.65, while a symbol of stability at the time, would come under severe pressure in the latter half of the 1950s, leading to the first major devaluation of the peso in decades in 1954. Thus, the currency situation in 1951 was one of managed equilibrium, masking the structural tensions between a fixed exchange rate and an inflationary, import-heavy development model.

However, this fixed exchange rate existed alongside persistent, though moderate, inflation and a growing demand for imports of capital goods and machinery. Mexico's economic strategy, known as "stabilizing development," prioritized industrial growth over strict price stability, leading to a gradual erosion of the peso's purchasing power domestically. While the currency's external value was firmly anchored, its internal value was slowly declining. This created a subtle overvaluation of the peso, which began to discourage agricultural exports and encouraged spending on imports, applying a slow but steady drain on the country's dollar reserves.

Consequently, 1951 represented a calm before a gathering storm. The policies of the Alemán sexenio had fueled growth through substantial public spending and credit expansion, setting the stage for the balance of payments crises that would challenge the next administration. The fixed parity of 8.65, while a symbol of stability at the time, would come under severe pressure in the latter half of the 1950s, leading to the first major devaluation of the peso in decades in 1954. Thus, the currency situation in 1951 was one of managed equilibrium, masking the structural tensions between a fixed exchange rate and an inflationary, import-heavy development model.

🌱 Common