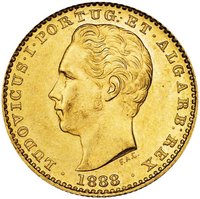

Obverse

Description:

Portrait of Luís I of Portugal.

Inscription:

LUDOVICUS·I·PORTUG: ET·ALGARB: REX

· 1888 ·

· 1888 ·

Translation:

Louis I, King of Portugal and the Algarves

· 1888 ·

· 1888 ·

Script: Latin

Languages: Latin, Portuguese

Engraver: Frederico Augusto de Campos

Reverse

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Imprensa Nacional - Casa da Moeda | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1868 | — | 24,000 | ||

| 1869 | — | 11,000 | ||

| 1870 | — | 500 | ||

| 1871 | — | 500 | ||

| 1872 | — | 1,000 | ||

| 1874 | — | — | Proof | |

| 1874 | — | 5,000 | ||

| 1875 | — | 2,000 | ||

| 1876 | — | 5,000 | ||

| 1876 | — | — | Proof | |

| 1877 | — | 2,250 | ||

| 1878 | — | 21,500 | ||

| 1881 | — | 1,000 | ||

| 1888 | — | 500 |

Historical background

In 1868, Portugal found itself in a precarious monetary situation, characterized by a severe shortage of metallic currency in circulation. The nation was officially on a bimetallic standard (gold and silver), but in practice, the scarcity of gold had led to a de facto silver standard. This scarcity was exacerbated by decades of political instability, fiscal deficits, and heavy foreign borrowing, which drained gold reserves to service debt. The public's consequent hoarding of available gold and silver coins created a chronic shortage of specie, disrupting everyday commerce and highlighting the state's fragile finances.

To address this crisis, the government authorized the increased circulation of paper money issued by the Banco de Portugal, which had held the sole note-issuing privilege since 1846. However, these notes were not fully convertible into specie on demand, leading to a discount against gold and a loss of public confidence. The currency system was fragmented and inefficient, with a mix of older copper coins, scarce silver milréis, and fiduciary paper of uncertain value circulating simultaneously. This period was part of a longer trajectory of monetary instability that would culminate in the 1891 debt default.

The situation in 1868 was therefore one of transition and strain. The state relied on inflationary paper money to finance its obligations, while the public grappled with the practical difficulties of a dysfunctional dual system. This environment set the stage for the more definitive monetary reforms of the subsequent decades, which would eventually attempt to stabilize the Portuguese currency by moving toward a gold standard and consolidating the role of the Banco de Portugal, though not without further crisis and devaluation.

To address this crisis, the government authorized the increased circulation of paper money issued by the Banco de Portugal, which had held the sole note-issuing privilege since 1846. However, these notes were not fully convertible into specie on demand, leading to a discount against gold and a loss of public confidence. The currency system was fragmented and inefficient, with a mix of older copper coins, scarce silver milréis, and fiduciary paper of uncertain value circulating simultaneously. This period was part of a longer trajectory of monetary instability that would culminate in the 1891 debt default.

The situation in 1868 was therefore one of transition and strain. The state relied on inflationary paper money to finance its obligations, while the public grappled with the practical difficulties of a dysfunctional dual system. This environment set the stage for the more definitive monetary reforms of the subsequent decades, which would eventually attempt to stabilize the Portuguese currency by moving toward a gold standard and consolidating the role of the Banco de Portugal, though not without further crisis and devaluation.

💎 Very Rare